Energy Security and Policy to Remain Key Risks to Markets

2023 to Only Be the End of the Beginning of Commodity Market Rebalancing

NEW YORK, LONDON (December 12, 2022) – Analysts at S&P Global Commodity Insights, the leading independent provider of information, data, analysis, benchmark prices and workflow solutions for the commodities, energy and energy transition markets, today released the latest 2023 energy outlook.

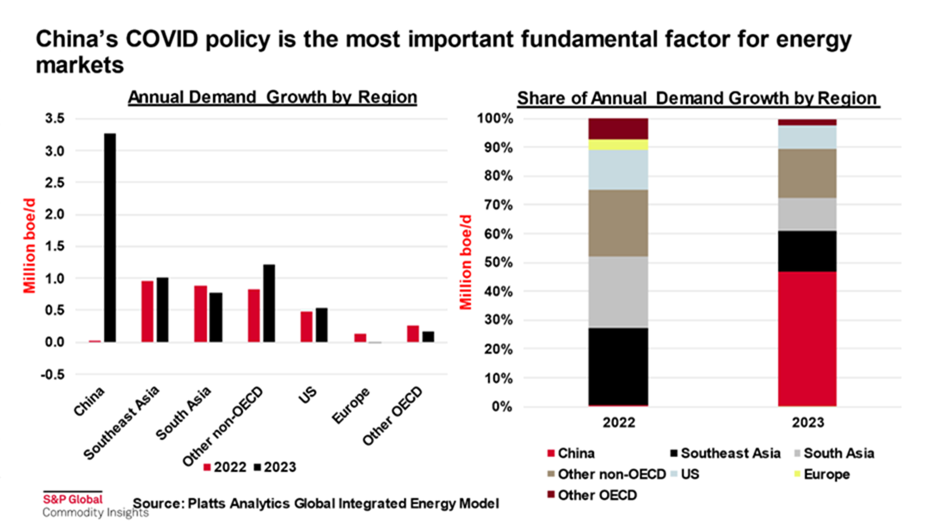

"China's COVID policy is the most important fundamental factor for global demand in commodities and energy in 2023," according to Dan Klein, Head of Energy Pathways, S&P Global Commodity Insights, "as its demand softness due to lockdowns in 2022 was a key safety valve for oil, gas, and coal markets, while Europe scrambled to replace Russian energy. With another year of vaccinations and growing frustrations with lockdowns domestically in China, restrictions will likely ease somewhat in 2023 and imports of fossil fuels can be expected to increase again."

The S&P Global Commodity Insights Energy Outlook 2023 presumes China's total energy demand will increase by 3.3 million barrels of oil equivalent per day, up from virtually no growth in 2022. This will represent 47% of global energy demand growth next year. While China's imports will likely return to growth a growth pathway, India has been a strong demand performer over the past year, with imports of oil and coal notably higher year-on-year, as it has absorbed significant volumes or Russian supply that would have gone to Europe.

OVERVIEW

The incredible rollercoaster ride that energy markets have been on since the onset of the COVID-19 pandemic in 2019/2020 has been extended, with unprecedented uncertainty on global energy supply developing over the past year in the wake of the Russian invasion of Ukraine, amid a backdrop of a weaker macroeconomy and high inflation.In 2023, S&P Global Commodity Insights expects that markets will be on an extended pathway of recalibration as supply and demand fundamentals adjust to elevated prices and supply uncertainty. Barring a significantly deeper recession than expected, it will take several years of stronger supply growth than demand growth for inventory cushions to return to comfortable levels, particularly if Russian energy export reductions are more severe than anticipated. For oil, while global supply will increase, it will grow slower in 2023 at around 1.7 million barrels per day (b/d) than the 4.5 million b/d growth in 2022, due to greater losses from Russia and limited upside from OPEC. While there has been a growing narrative that the US shale revolution is over, we expect 0.7 million b/d of oil supply growth from US shale alone, with additional growth in crude production coming from Norway, Brazil, Canada, and Guyana.

For natural gas, global supply growth, particularly liquefied natural gas (LNG), will be limited in 2023 despite extremely high prices, due to a lack of new liquefaction facilities coming online. This will require LNG markets to balance again on demand destruction rather than supply growth. This dynamic will be particularly apparent in Europe, where there will be even less Russian gas supply in 2023 than in 2022, requiring considerable demand destruction.

In general, commodity prices are expected to ease over 2023, as fundamentals pull toward recalibration. Natural gas, coal, and crude oil prices are all expected to be lower in 2023 than 2022 on average. However, while the "platinum age" of refining will ultimately come to an end, 2023 should still be golden for refiners, with refined products prices maintaining lofty levels. Electricity prices are also poised to deflate, with another tranche of renewables becoming operational and European policymakers looking to weaken the link between natural gas and power prices. Once again, demand for all fossil fuels will increase in 2023, which points to a global CO2 emissions rise despite continued attention paid to climate and the energy transition. The environment created by prevailing geopolitical uncertainty, weaker macroeconomic growth, and high inflation will keep the energy security versus energy transition debate front and center. While there have been commodity crises driven by supply disruptions in the past, the world is dealing with the first truly global energy crisis across all fuels. The market will adjust with fuel substitution and altered trade flows, requiring a holistic global perspective across the breadth of the energy market.

TOP TEN KEY THEMES TO THE 2023 ENERGY OUTLOOK: S&P GLOBAL COMMODITY INSIGHTS:

- China's COVID policy is the most important fundamental factor for energy markets. China's COVID-related restrictions which led to underperforming energy demand growth, and weaker Chinese energy imports was a key safety valve for oil, gas, and coal markets in 2022. Were it not for this demand weakness, prices of all commodities would have undoubtedly been higher, as energy supply not absorbed by China shifted to other areas, highlighted by LNG supply shifting to Europe. While China's imports of crude oil (-0.2 million b/d, -2.0%), LNG (-58 million cubic meters (cu m) -19.7%), and thermal coal (-45 million metric tons (mt), -17.2%) are all on track to contract in 2022, we expect them all to return to growth in 2023. Rising unrest and public protests over COVID policies support this view. If China's energy demand and imports are strong in 2023, commodity prices will be well supported, but another year of subdued demand from China would be a significantly bearish development for virtually all commodity prices.

- India will have its say as well. With China somewhat on the sidelines in 2022, India's energy demand proved to be one of the greatest areas of strength. While India's LNG imports will decline year-on-year over 2022, its oil demand will increase by just shy of 0.3 million barrels per day (b/d), with only the United States growing by a larger amount. India's imports of thermal coal increased by most of any country in the world in 2022 by far (+15 million mt). India has proved to be a key source of demand for Russian energy that would have ordinarily gone to Europe in 2022, and this dynamic becomes even more important as European sanctions on oil tighten, although there are significant questions if India will be willing or able to absorb even more Russian supply.

- The recalibration of energy markets will outlast 2023. Global energy markets have been battered with a pandemic, an uneven recovery, swings in OPEC policy and record uncertainty around energy supply in response to the Russian invasion of Ukraine. Even before 2022 began, global inventories were strained due to a stronger recovery in demand than supply from COVID, with several markets requiring demand destruction to balance. Even if commodity supply/demand balances loosen more than expected in the coming year, almost all markets will require another year or more of recalibration before inventories, balances, and prices return to a more sustainable equilibrium. Even in agricultural commodities, where new planting seasons usually offer new beginnings, several planting seasons will be required to recover from the Ukraine/Russia losses.

- The reports of US shale's demise are greatly exaggerated. There is a growing narrative in the market that "the shale revolution is dead". While growth in shale has and will continue to be more controlled than in recent years, US shale production, including natural gas liquids (NGLs), is on track to increase by more than 1.0 million b/d in 2022 and another 1.4 million b/d in 2023, representing one of the largest components of global supply growth in both years. Shale oil price breakevens (less than $50 per barrel) remain on the low end of the global supply curve, and ~90% of the 180 billion barrels of technically-recoverable oil is yet to be developed. After a sluggish start to the year, US natural gas production has increased by 3 billion cubic feet per day (Bcf/d) in 2022, and another 3 Bcf/d of growth is expected in 2023.

- The "Platinum Age" of refining will ultimately come to an end, but 2023 should still be golden for refiners. Refining margins in 2022 were the strongest ever on a sustained basis, driven particularly by middle distillate strength. This requires a new moniker for describing this period, and we have dubbed it the "platinum age". While some refining cracks will weaken over 2023 due to slower demand growth and new refinery startups, diesel cracks are expected to stay much stronger than historical averages in 2023. And gasoline cracks are expected to strengthen sharply for the second quarter. Furthermore, there is also upside to margins due to low middle distillate inventories and the potential for larger reductions of Russian diesel exports than currently assumed. Overall, refining margins are expected to remain strong for 2023. The capacity driven, cyclical petrochemicals downturn will last at least through 2023, depending on the pace of capacity rationalization. There will be nowhere to hide in the global petrochemicals market during 2023, noted Robert Stier, Sr Lead, Global Petrochemicals, S&P Global Commodity Insights; All value chains (olefins, aromatics, and polymers) will continue to be under severe margin pressure.

- European gas and power markets may be even tighter in 2023. European consumers and policymakers achieved a herculean feat in 2022 by building up natural gas storage to near capacity ahead of winter, with an armada of LNG vessels still waiting to unload supply via the Continent's expanded regasification capacity. Despite this exemplary performance, the encore in 2023 may be more challenging as Europe will have to deal with a full year's worth of virtually no Russian gas, and only a small increase in global LNG supply. European gas will need to balance on demand destruction rather than growth in available supply. Additionally, European buyers should not count on a recurrence of weak Asian LNG and mild temperatures in late-autumn/early-winter to facilitate storage builds. With natural gas prices expected to remain elevated, structural reform of Europe's electricity markets to weaken the link between gas and power prices is high on the agenda for 2023, although there will be significant challenges to achieving such measures.

- Energy security/affordability and energy transition decisions to become even more difficult and complex. 2022 was marked by difficult choices in response to the Russian invasion of Ukraine. Some nations loosened restrictions on the operation of coal-fired power plants, while others extended the lives of coal and nuclear power plants that were planned to retire. However, demand destruction from high prices across a variety of sectors and continued renewables generation growth limited emissions. With several economies expected to be in a recession in 2023 and fiscal budgets stretched, policymakers will be looking to keep energy prices low, perhaps sacrificing progress on the energy transition. While high fossil fuel prices may accelerate some consumers' plans to switch to an electric vehicle or install rooftop solar, the drain of household wealth from high inflation will limit consumers' ability to lay out the higher upfront capital for these green technologies even if they are less expensive that fossil fuels over the lifetime of the asset.

- The importance of international climate agreements and the annual COPs for driving energy transition will be tested. Amidst concerns around energy security, economic growth, and geopolitical tensions, COP27 in Egypt featured a general lack of increased ambition on reducing emissions. While COP27 did lead to a global agreement featuring historic language on loss and damage, establishing a fund for the costs of climate change for the most vulnerable emerging and developing economies, relatively little was agreed to address the emissions driving climate change. To be sure, progress on the energy transition has been made over the past year through domestic industrial policies, bilateral agreements, and ties among smaller groups of stakeholders – efforts such as the Five-Year Plan in China, Fit for 55 in the EU, the Inflation Reduction Act in the U.S., and Just Energy Transition Partnerships. More targeted forums such as the G20 – led by India in this coming year - are increasingly providing platforms for impactful decisions.

- The drivers of energy supply shift more toward policy over economics, increasing volatility. The importance of policy on energy supply was on full display in 2022, headlined by the policy responses to the Russian invasion, the swinging probabilities of an Iran nuclear deal, recent loosening of some sanctions on Venezuela, and OPEC's production quota policies. A clear example of how important supply policy will be in 2023 is how effective the price cap on Russian supply will be. While forecasting markets based on the economics of supply and demand can be difficult, predicting what policymakers will do is next to impossible. Even energy producers situated in countries with limited or more predictable governmental policies will be affected by policies, such ESG pressures from shareholders, net zero commitments, and carbon border adjustment mechanisms.

- Inefficiencies in global trade will continue to support freight rates and delivered prices. The emergence of new trading patterns in response to the Russian invasion of Ukraine has led to greater inefficiencies in the shipping sector. Specifically, Europe's source diversification for oil, and the need to send Russian oil to Asia has led to increased ton-mile demand and consequently clean and dirty tanker freight rates. Additionally, the efforts to supply Europe with enough gas for the winter created a notable increase in the use of floating storage of LNG tankers. These conditions are expected to persist and perhaps intensify in 2023, which should keep freight rates elevated, and keep delivered prices supported.

EUROPE AND NATURAL GAS

"European suppliers achieved a herculean feat in 2022 by building up natural gas storage to near capacity ahead of winter," said Michael Stoppard, Global Gas Strategy Lead and Special Advisor, S&P Global Commodity Insights. "Round Two' in 2023 may be more challenging as Europe will have to deal for the first time with a full year's worth of minimal Russian pipeline gas, and only a small increase in global LNG supply. European gas will need to balance on reduced demand rather than growth in available supply. Additionally, in a global gas system without any slack, European buyers cannot count on a recurrence of weak Asian LNG and mild temperatures."

Media Contacts

Global/EMEA: Paul Sandell, + 44 (0)7816 180039, paul.sandell@spglobal.com

Americas: Kathleen Tanzy, +1 917-331-4607, kathleen.tanzy@spglobal.com

Asia: Melissa Tan, +65-6597-6241, melissa.tan@spglobal.com

About S&P Global Commodity Insights

At S&P Global Commodity Insights, our complete view of global energy and commodities markets enables our customers to make decisions with conviction and create long-term, sustainable value.

We’re a trusted connector that brings together thought leaders, market participants, governments, and regulators and we create solutions that lead to progress. Vital to navigating commodity markets, our coverage includes oil and gas, power, chemicals, metals, agriculture, shipping and energy transition. Platts® products and services, including the most significant benchmark price assessments in the physical commodity markets, are offered through S&P Global Commodity Insights.

S&P Global Commodity Insights is a division of S&P Global (NYSE: SPGI). S&P Global is the world’s foremost provider of credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity and automotive markets. With every one of our offerings, we help many of the world’s leading organizations navigate the economic landscape so they can plan for tomorrow, today. For more information visit https://www.spglobal.com/commodityinsights