Concurrent maintenance activities and outages on the supply side tightened the LNG market during the month of June. This caused a massive rally in the Platts JKM price for spot deliveries into Northeast Asia. Now we have to ask whether this trend is expected to continue, or if supply will come back in the coming months leading up to the winter.

Welcome to The Snapshot, a series examining the forces shaping and driving global commodities markets today.

Let's focus on the counter seasonality of supply and demand within the LNG market, as we've seen a bit of a break from recent years on how both supply and demand are behaving. This is being reflected in prices as the Platts JKM was assessed as high as $11.45 during the month of June, which represents the highest outright prices since this past winter, and a far cry from the low of around $7 we saw just a few months prior. The big question that everyone is asking is what is driving this tight market, and more importantly, will it continue? Well, the answer is a combination of what's happening in both supply and demand.

One of the largest drivers of the recent price rally was on the supply side. When we take a look at total aggregate supply compared to previous years, we can see that overall, supply has been higher in 2018 compared to last year. However, recently, concurrent outages and maintenances across several different production regions created a counter-seasonal decline in supply of LNG. In total, supply during June fell more than 70 Mcm/d below where supply averaged during the first quarter.

We observed production losses compared to recent averages across many different facilities over the past month or so, which included Nigeria, the United States, Russia, Qatar, Indonesia, Malaysia and Australia. Furthermore, this occurred right as demand started ramping up for the heart of the cooling season in the Northern Hemisphere combined with the main heating season in the Southern hemisphere. In fact, during the past four years the month of June is traditionally a time when supply starts to pick back up after shoulder season maintenances. This year we saw the opposite occur and it's important to note that supply actually fell below where it was a year ago two separate times already this year.

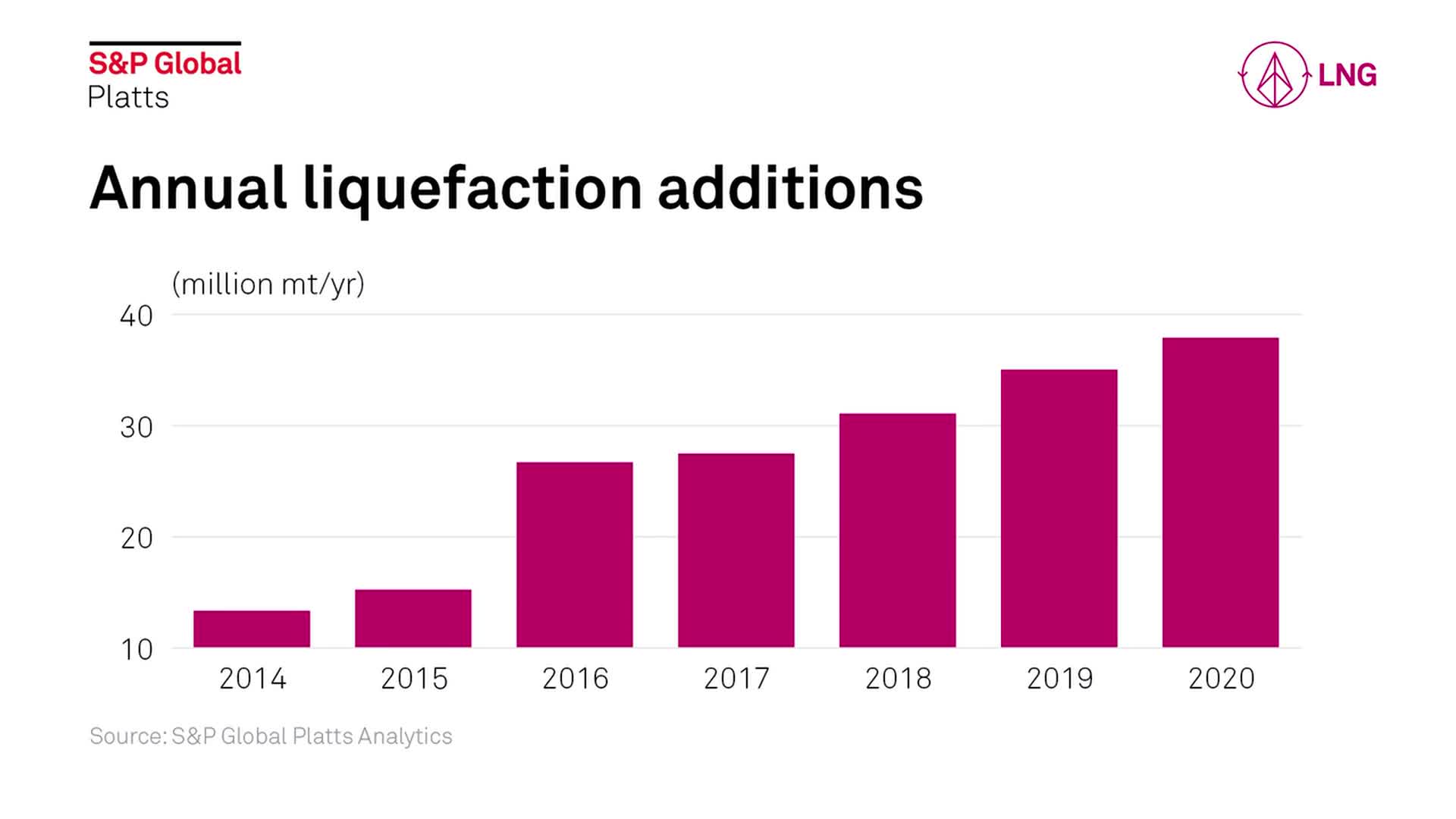

So now the question becomes whether or not the current market conditions are expected to continue. Well, on the supply side, we're already starting to see production come back to levels before the recent decline. We still have a ways to go to get back to Q1 levels, but overall supply is starting to look relatively healthy again. This should limit the upside to prices as demand starts to taper off into the second shoulder season and we forecast prices to fall before heading into the winter. We are also expecting new supply to come online this year, but most is centered during the second half of the year, and only about a quarter of the expected growth in liquefaction capacity is already online.

However, it's important that we not forget about demand, which has maintained a very strong pace this year, especially from China. This should not be ignored, and the balance of supply and demand will likely hinge on whether Asian buying remains strong. We will be following this story closely as we analyze the markets and fundamentals around the globe.

Until next time on Snapshot, we'll be keeping an eye on the markets.