Disruption of backfill plans for NWS LNG and Pluto LNG

<span/>Prior to the coronavirus (COVID-19) pandemic and oil price crash issues, the story of the future supply of feedstock gas into some of Western <span/>Australia's LNG plants was looking pretty firm. There was Barossa to backfill Darwin LNG, Browse to backfill North West Shelf (NWS) LNG and Scarborough to both backfill Pluto LNG train 1 and also underpin the development of Pluto LNG train 2.

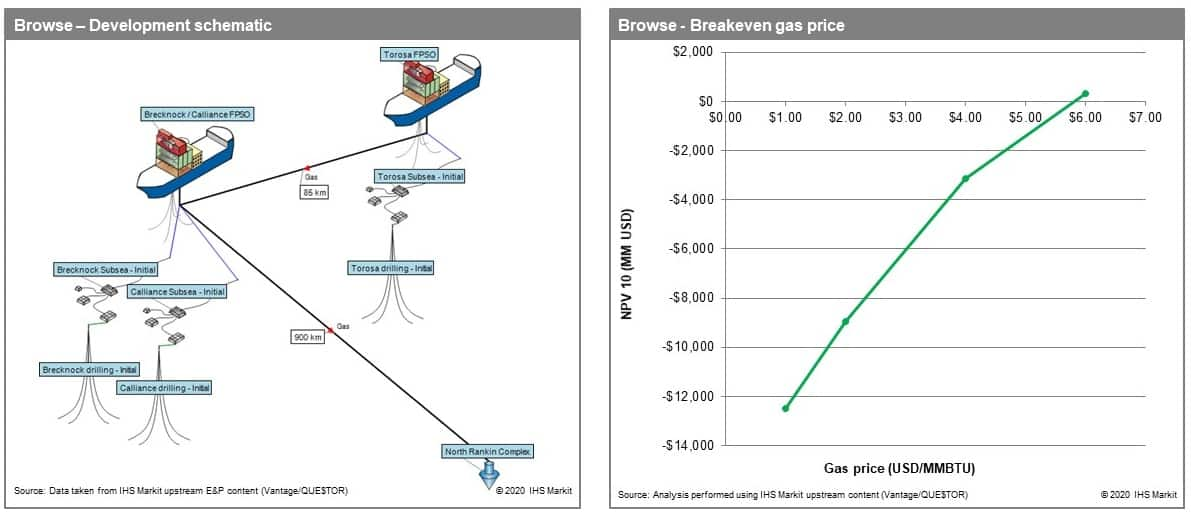

However, the ground is starting to move beneath our feet and what we thought we knew is being challenged. Woodside has admitted that their plans may need to change, with Browse economics struggling to stack up in the current price environment and emissions pressures only likely to increase the costs. Based on the current development plans, we see the upstream breakeven gas price for Browse sitting in the region of USD 5-6/MMBTU.

Image 1: Browse development and estimated economics

Assuming that the ultimate LNG product would be sold at a (currently generous) 12.5% slope to Brent, with a USD 2/MMBTU tolling fee (which is around the discussed value) to go through NWS LNG and USD 0.6/MMBTU to get the LNG to the end market, then a Brent price of USD 60-70/bbl would be required to support the project economics.

If not Browse, then what?

We aren't saying that Browse won't happen and that it won't still be an important part of the future supply story but, if we play devil's advocate and assume that Browse won't be the first cab off the rank, then this does ask the question: what will be next? There are a number of options that could be looked at, we have chosen to discuss the following four:

- Scarborough: could be prioritised as backfill for NWS LNG, with Pluto train 2 delayed/cancelled.

- Clio-Acme: previously talked up as a backfill option for NWS LNG.

- Onshore Perth basin: deeper play is providing new gas volumes.

- Exploration: the 15 Tcf Ironbark prospect is planned to be spudded in October 2020.

Each of these options is discussed in more detail below. It should be noted that this is far from a comprehensive list and there are many other discovered resources and prospects that could be developed to provide backfill.

Scarborough

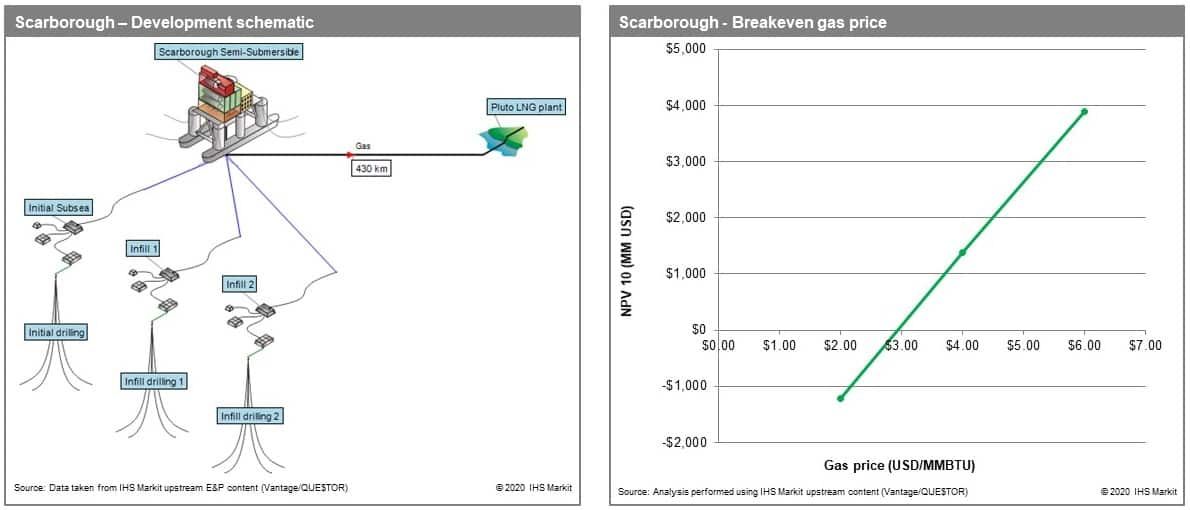

The Scarborough field is located approximately 375km west-northwest of the Burrup Peninsula. Most of the Scarborough gas field sits in WA-01-R retention lease, with some in the WA-62-R retention lease and the participating interest in the Scarborough field is Woodside (73.5% + operator) and BHP (26.5%).

Woodside's current development plan is based on the gas supporting the development of a new second train at the Pluto LNG plant, with some of the production also supporting any decline in feedstock for train 1 and also, potentially, being sent through the interconnector to NWS LNG.

If Pluto Train 2 was put on hold or cancelled, then Scarborough gas could be diverted to NWS LNG. This would require little change in the upstream development plan for the field, with our calculated breakeven gas price being significantly lower than Browse.

Image 2: Scarborough development and estimated

economics

It should be noted that the discussed tolling fee for Pluto Train 2 is around the USD 3/MMBTU mark and, if the gas was to be routed through NWS LNG then further investment in the NWS LNG plant may be required to handle the Scarborough gas that is very lean, which would need to be recovered through a higher toll than the discussed USD 2/MMBTU for Browse through NWS LNG.

Additionally, Woodside have publicly stated that they would like to farm-down their interest in both the upstream asset and the Pluto Train 2 development to ease their capital burden. With uncertainty around the final destination of the gas, it will be a challenge to value the assets, and any deal will therefore be unlikely until this is resolved.

Clio-Acme

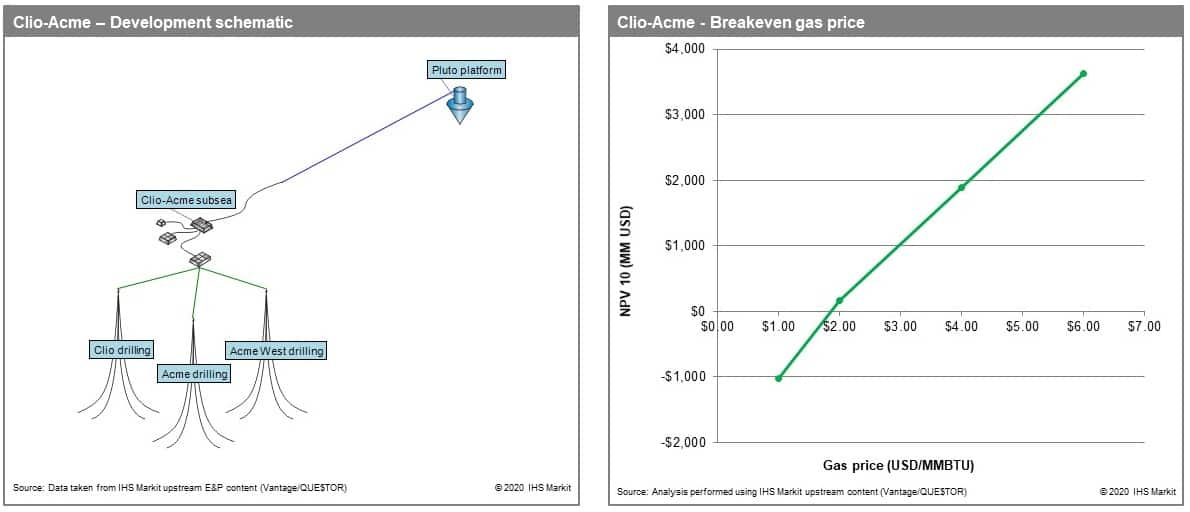

The Clio-Acme gas fields are located in WA-42-R retention lease that is held by Chevron (100% + operator). The fields sit in waters ranging from 875-960m deep. We do not have any information on the CO2 content but there is a small amount of associated condensate.

As recently as November 2018, positive news had been put out on Clio-Acme, with the NWS Joint Venture signing preliminary agreements with Chevron in respect to the potential processing of Clio-Acme gas through the NWS LNG facilities. The outlined development plan had been relatively simple, with subsea wells being tied-back to the Pluto platform, with the gas getting from Pluto LNG plant to the NWS LNG plant through the planned interconnector.

When we look at the economics of this development then it stacks up well. However, a 50km subsea tie-back may be a technical challenge, with a semi-submersible or FPSO then required. This would push up the breakeven price. We have assumed raw gas CO2 content of about 2%.

Image 3:Clio-Acme development and estimated

economics

The discussions for processing Clio-Acme gas through the NWS LNG were reported to have broken down last year and, with Chevron announcing its intention to sell its stake in NWS LNG, it seems unlikely that their molecules will be prioritised as feedstock. The future of Clio-Acme may lie as a backfill option for the Chevron operated Wheatstone LNG plant although we do not expect a window until the early 2030's. The window at Chevron's Gorgon LNG plant would be even further away.

Onshore Perth basin:

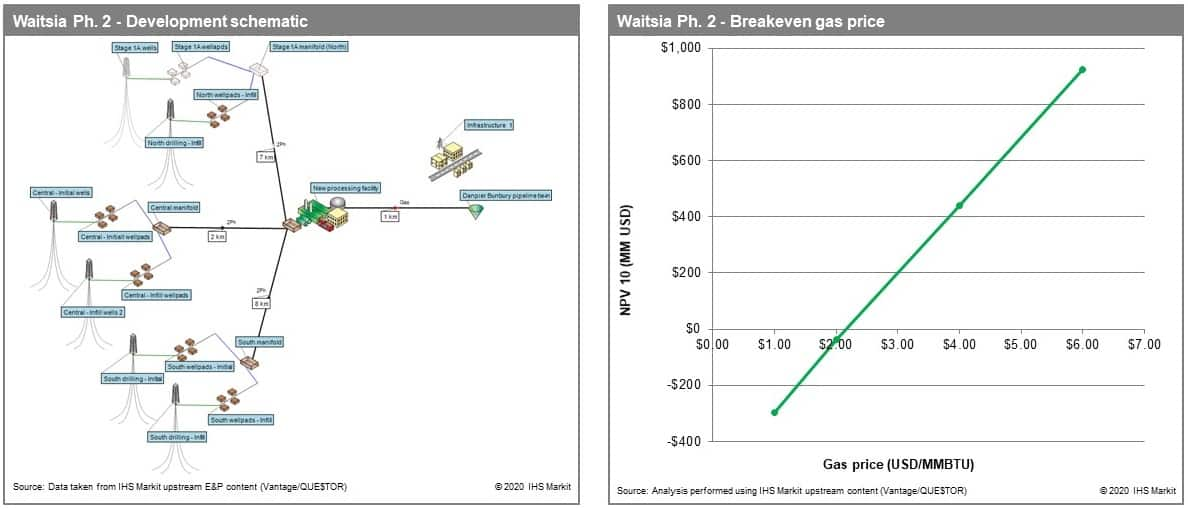

The onshore Perth basin has seen a recent renaissance with a deeper play that was started with the Waitsia field and has been followed up with West Erregulla and Beharra Springs Deep and a number of other prospects being similarly considered. These fields sit about 300km North of Perth and about 1000km south of the Burrup peninsula and the LNG plants. The gas is generally dry with CO2 content in the range of 5-10%.

The monetisation story for these discoveries has been around them providing a lower cost source of gas to the domestic market. There has been some talk about diverting the gas to the LNG plants but the distance from the fields to the plants would make this unlikely. Another option would be for LNG exporters to meet Western Australia's domestic gas reservation policy through gas swaps, with these onshore discoveries replacing gas supply from fields currently dedicated to the LNG plants.

The development plan has typically been phased, with small initial developments based on gas sales agreements. Larger phases are then planned that will involve the drilling of a limited number of new wells and the expansion of new processing facilities or the installation of new facilities. The sales gas can easily be tied into the Dampier Bunbury Natural Gas Pipeline (DBNGP) and it would benefit from lower transportation costs to Perth when compared to the domestic gas plants at the LNG facilities.

Image 4:Waitsia Phase 2 development and estimated

economics

If the focus turns to keeping the LNG plants full before new supply sources come onstream, then a window could be opening sooner than expected. A lot may depend on how the domestic market obligations are handled, particularly given that the NWS LNG plant's domestic obligation ended in 2020.

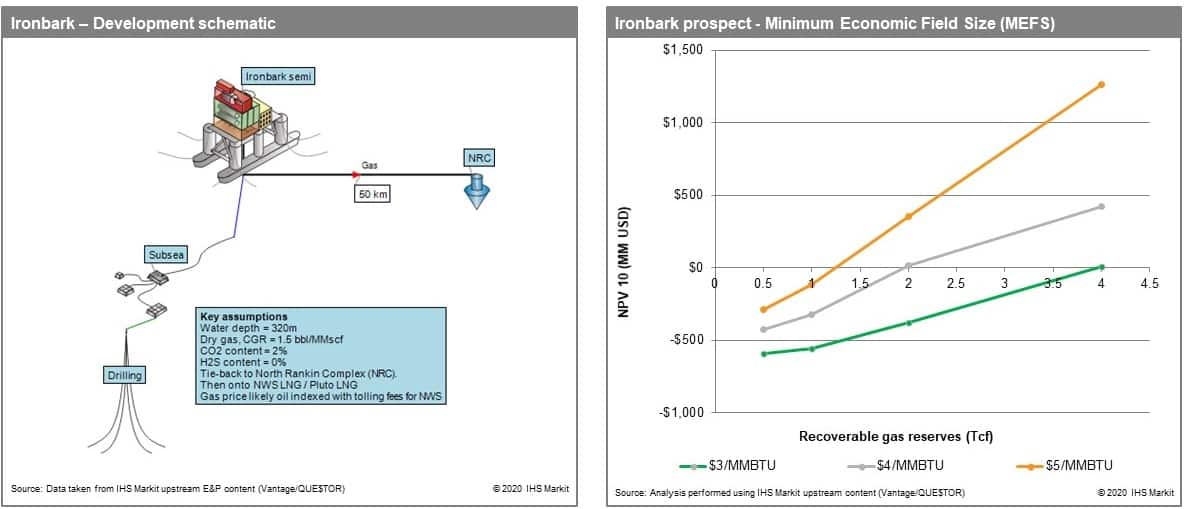

Exploration: Ironbark

The Ironbark prospect is located about 50km outboard from the North Rankin Complex, with the majority of the prospect sitting across the WA-355-P and WA-409-P exploration permits. These are both operated by BP with Beach, Cue and NZOG having participating interests in both permits.

The prospect has been reported to have a pre-drill recoverable gas resource estimate of 15 Tcf, which should certainly result in positive economics. When we run some analysis looking at the minimum economic field size for the prospect, it looks encouraging. A development based on a subsea tie-back to one of the existing platforms (i.e. North Rankin, Pluto or Wheatstone) may be possible, or a new pipeline to shore may be required. For now, our model assumes dry gas with a moderate CO2 content of 2% with a development plan based on a semi-submersible being installed on the field and an export pipeline to the North Rankin Complex.

Image 5: Potential Ironbark development and estimated

economics

As with a lot of other prospects and discoveries on the North West Shelf, the challenge in monetising the molecules will be in finding a route to market. In the above chart, the Minimum Economic Field Size (MEFS) for a USD 4/MMBTU gas price is about 2Tcf and for a USD 3/MMBTU gas price is about 4Tcf.

However, with the potential window opening at NWS LNG, the prospect has progressed and, in mid-July NOPSEMA approved the Environmental Plan (EP) for the Ironbark 1 exploration well and it is understood that the plan is to spud the well in October 2020, dependent on the rig's prior commitments.

Looking for new answers to old questions

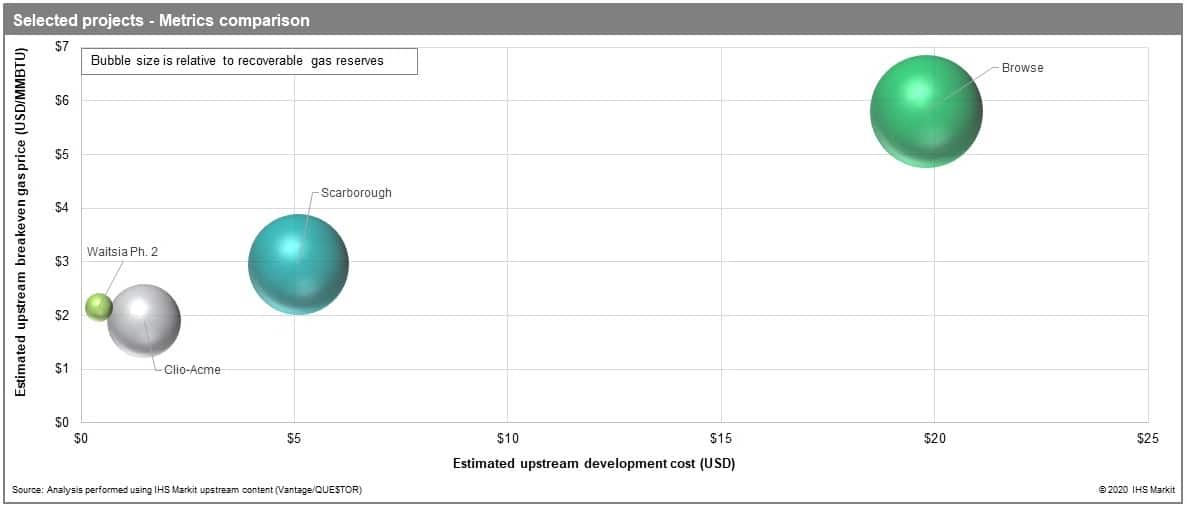

The balls are very much all in the air again and there are many layers of complication to work through before we will see where they all fall. The most likely scenario, if prices do not recover, would be that Browse gets indefinitely delayed and Scarborough will be brought in to backfill NWS LNG, with Pluto Train 2 cancelled. However, there is no lack of alternative potential gas that could serve as backfill.

Image 6: Comparative upstream metrics

However, with the JV dynamics as they are, we could see mismatched objectives that see disagreements over the best path forward resulting in no new projects being prioritised and the NWS LNG plant being under-utilised, in which case no-one wins.

Adding to the mix is the proposed sale of Chevron's NWS LNG stake. Putting a value on this is going to be very challenging given the lack of clarity on both when and where backfill gas will come from and what the associated tolling fee will be.

These are not the kind of risks and uncertainties that would attract an infrastructure investor. Therefore, the most likely destination is one of the existing JV partners. Woodside appear to be everyone's current favourites, and for good reason. A larger stake would help them push the case for their molecules, and on a tolling basis that works for them. However, if BP are confident about Ironbark then this could see them take a keen interest in the sales process to prevent Ironbark becoming another stranded gas discovery on the North West Shelf. The remaining partners seem less likely but CNOOC, who currently have a stake in the upstream licences but not any of the infrastructure, could be keen. However, there are significant doubts around the Australian government's willingness to let them own a stake in such a key piece of infrastructure.

Let the games begin!

Robert Chambers is a Director in the Upstream asset valuation team at IHS Markit.

Posted 06 August 2020

This article was published by S&P Global Commodity Insights and not by S&P Global Ratings, which is a separately managed division of S&P Global.