Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Both Producing and Non-Producing States Benefit Both oil and gas producing and non-producing states are reaping the benefits of the unconventional oil and gas revolution. Some states benefit through direct upstream exploration and production activities, while other states benefit through the vast supply chain supporting unconventional oil and gas development, or both. States also benefit from the interstate trade that occurs as the unconventional oil and gas income effect flows through the economy.

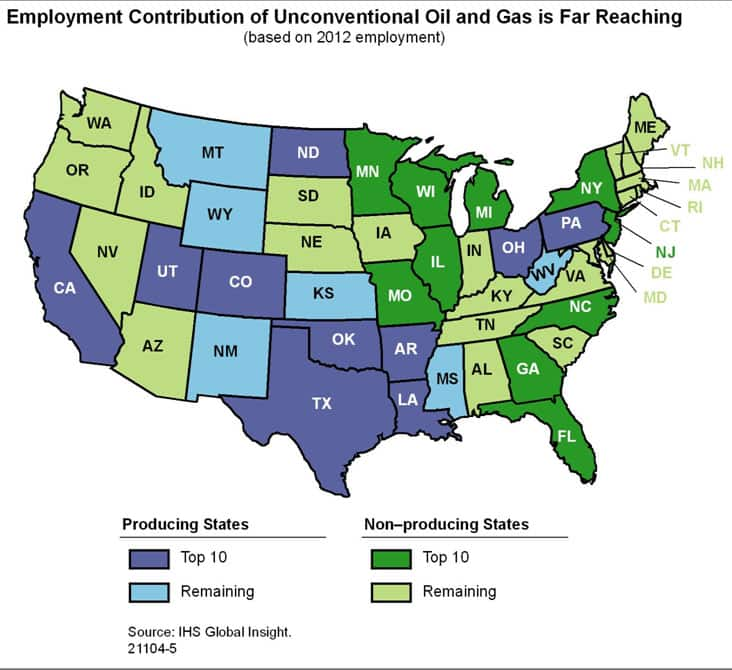

Generating over 1.2 million jobs, state-level impacts are clear among producing states - those states that contain one of 20 identified unconventional oil and gas producing plays or have an emerging oil or natural gas play that is expected to have sizeable oil and/or natural gas production at some point during the 2012 through 2035 forecast period. Texas and Oklahoma, two states with long histories of oil and gas production and a combined total of over 650,000 jobs in 2012, are home to many firms whose expertise and technology are helping lead this new era of oil and gas development. In fact, four out of every five jobs are associated with producing states.

However, these traditional energy states are not the only ones benefitting in the producing states category as the energy outlook is shifting away from traditional energy states. States such as Pennsylvania, North Dakota and Ohio, with a combined 180,000 jobs linked to unconventional oil and gas activity, have entered the unconventional arena and are expected to remain in the top 10 producing states in terms of employment, value added and government revenue through at least the end of the decade. Other leading states include North Dakota - now the second largest oil producer behind Texas, Pennsylvania - home to Marcellus play, and Ohio which is on the brink of significant unconventional developments. These developments have the potential to fundamentally shift the traditional energy supply models in the US which have infrastructure, refinery capacity, and supply chains centered on the legacy producing states. The emergence of these "new" energy producing states is changing this legacy geographic model for energy supply and poses both opportunities and challenges in the coming years.

States classified as non-producing - defined as (1) those whose geographic boundaries do not contain any of the 20 largest unconventional oil and natural gas producing plays nor contain any part of an emerging oil or natural gas play in the 2012 to 2035 forecast horizon; or (2) those with plays that are currently producing oil and/or natural gas, but nevertheless are classified as non-producing states because current production is relatively small and the prospect for future unconventional production is unknown are also reaping benefits of the unconventional oil and gas revolution. Even though these states lack major oil and gas resources, they nonetheless host firms that sell goods and services that are critical to the lengthy supply chain supporting unconventional oil and gas development. In fact, one out of every five jobs attributed to the unconventional oil and gas activity is associated with a non-producing state. Examples of central players in the US unconventional oil and gas supply chain are fabricated metal manufacturing in Illinois, software and information technology in Massachusetts, and financial services and insurance in Connecticut. Additionally, despite the moratorium, New York, which furnishes non-capital goods such as financial and professional services to the unconventional oil and gas industry, is the top state in terms of its employment, value-added and government revenue contributions in 2012.

Increased Local, State, and Federal Government Revenue Based on IHS analysis, the cumulative government revenues from unconventional oil and natural gas activity is expected to exceed $2.5 trillion from 2012 through 2035. Among the producing states, the 10 that provide the most tax revenues will contribute about 75% of that total, or nearly $1.9 trillion. Roughly 18% of all tax revenues will be generated from activities in all of non-producing states.

Expanding revenues related to unconventional oil and gas activity in producing states such as North Dakota and Pennsylvania are, among other uses, being allocated to address community impacts in public safety, public education and to underwrite critical infrastructure requirements, such as the roads and water treatment that will support future oil and gas developments.

While my most recent posts have focused on the upstream employment and economic contributions generated by this unconventional activity, my next entry I will address the findings from the final report which will examine the mid-stream, down-stream, and industrial manufacturing implications for the US stemming from this unconventional revolution.

Posted 27 February 2013

This article was published by S&P Global Commodity Insights and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fcommodityinsights%2fen%2fci%2fresearch-analysis%2fihs-ceraweek-2013-preview-the-unconventional-energy-revolution-fueling-economic-growth-a-state-look.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fcommodityinsights%2fen%2fci%2fresearch-analysis%2fihs-ceraweek-2013-preview-the-unconventional-energy-revolution-fueling-economic-growth-a-state-look.html&text=CERAWeek+by+S%26P+Global+2013+Preview%3a+The+unconventional+energy+revolution+fueling+economic+growth+%e2%80%93+A+state+look","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fcommodityinsights%2fen%2fci%2fresearch-analysis%2fihs-ceraweek-2013-preview-the-unconventional-energy-revolution-fueling-economic-growth-a-state-look.html","enabled":true},{"name":"email","url":"?subject=CERAWeek by S&P Global 2013 Preview: The unconventional energy revolution fueling economic growth – A state look&body=http%3a%2f%2fstage.www.spglobal.com%2fcommodityinsights%2fen%2fci%2fresearch-analysis%2fihs-ceraweek-2013-preview-the-unconventional-energy-revolution-fueling-economic-growth-a-state-look.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=CERAWeek+by+S%26P+Global+2013+Preview%3a+The+unconventional+energy+revolution+fueling+economic+growth+%e2%80%93+A+state+look http%3a%2f%2fstage.www.spglobal.com%2fcommodityinsights%2fen%2fci%2fresearch-analysis%2fihs-ceraweek-2013-preview-the-unconventional-energy-revolution-fueling-economic-growth-a-state-look.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}