Natural gas as part of utilities’ low-carbon strategy

While US power generation expansion is largely focused on clean energy technologies like solar, wind and batteries, S&P Global Commodity Insights research has identified a growing trend in the United States to define a reliability-centered role for new natural gas-fired power generation. Commodity Insights' review of recent utility integrated resource planning (IRP) filings reveals a consistent pattern:

- For most new construction, a focus on clean energy resources like solar, wind, storage batteries and energy efficiency

- A schedule for the phased-in retirement of existing fossil-fired generation, particularly coal

- A provision for the development of some new natural gas-fired generation, mostly to maintain grid reliability beyond what can be accomplished with clean energy resources

This new natural gas generation is typically a small proportion of the total new build and is justified in the context of enabling the associated clean energy development and the retirement of coal plants, thereby making the new gas generation an essential part of a utility's decarbonization strategy. These plans remain contentious, with environmental advocates and others often raising objections about the necessity of any new gas generation. These plans are, however, consistent with Commodity Insights' observation that the need for such dispatchable long-duration resources is becoming a global trend. Our see the tactic of including a relatively small amount of new gas-fired generation as part of a broader clean energy and coal retirement strategy which has been developing for several years, for example with the Tennessee Valley Authority's 2019 IRP and Duke Energy Indiana LLC's 2021 IRP. This trend is accelerating as evidenced in a review of 2023 IRPs from Georgia Power, Salt River Project, Dominion Energy South Carolina, Tucson Electric and Unisource Energy Services.

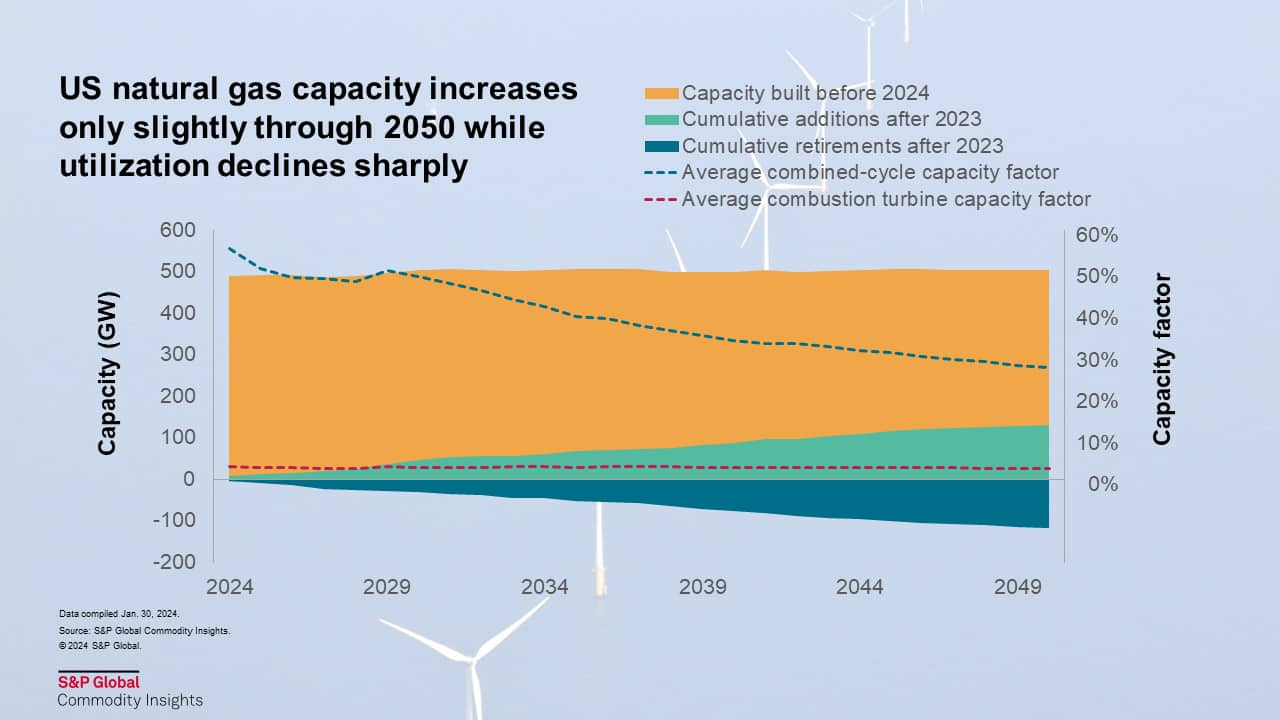

Natural gas power plant development is at a 25-year low according to a recent US Energy Information Agency report. The above utility strategies represent a potential reversal in this trend, and are consistent with Commodity Insights' long-term US power market view, which anticipates a sustained but evolving role for natural gas. Our most recent outlook calls for the size of the US gas power fleet to remain relatively stable through 2050, growing slightly from about 487 GW today to 503 GW in 2050 (see accompanying Figure). Notably, the 2050 US power fleet will consist largely of assets already in operation, with new construction through 2050 slightly exceeding expected retirements.

Natural gas fleet operations are expected to significantly change as the role of natural gas-fired generation realizes a diminished emphasis on providing energy and more focus is put on grid reliability. The operational change is focused primarily on combined-cycle technology, declining from a fleet annual average capacity factor of 56% in 2024 to about 27% in 2050. The average capacity factor for combustion turbines remains relatively constant at about 3% through 2050.

Trends to watch for. The evolving role for gas capacity as envisioned in Commodity Insights' Planning Case is not without risk, and we recommend that power market participants monitor two major signposts:

- The ability of natural gas developers to overcome environmental headwinds. While utility IRPs are one indicator of natural gas development momentum, more support will be needed to offset the environmental pressure to wean the US power industry off gas as soon as possible.

- The physical and financial condition of the existing gas assets in the Northeast and western US. The avoidance of new natural gas construction in these regions hinges on the presumed continued operation of existing (and aging) natural gas assets to provide grid stability and some energy. This will require the regions to provide asset owners with adequate compensation for unit maintenance and periodic capital injections. As these assets are located in regions with the greatest amount of resistance to natural gas-fired power generation, these assets are exposed to some level of financial risk, and if they are forced to retire, regional grid management will be much more difficult.

To find out more information and learn the value of our global gas markets coverage, please click here.

This article was published by S&P Global Commodity Insights and not by S&P Global Ratings, which is a separately managed division of S&P Global.