Water disposal stands out in the growing US onshore upstream water lifecycle market

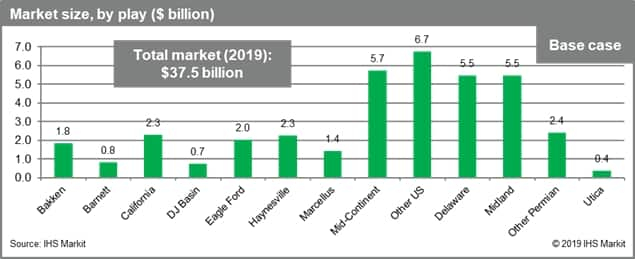

IHS Markit estimates the US oilfield water management to be valued at around $37 billion in 2019, representing a 12% year-on-year (y/y) market growth from 2018; this is mainly driven by water disposal and water logistics. The Permian Basin continues to produce and demand the largest volume of oilfield water among all US onshore regions, with water spending in the region estimated at $13.3 billion in 2019.

Figure 1: Market size, by play ($ billion)

Within the value chain of the water management market, water logistics continues to be the largest segment. Indeed, logistics are expected to make up 60% of spending in 2019 with water hauling services the main driver in that category.

Right behind water logistics is water disposal. As hydrocarbon production continues to increase, mainly due to Permian Basin activities, produced water is projected to follow the same trend. As a result, the water disposal market should continue growing at a 6% compound average growth rate (CAGR) through 2024. However, this growth could be limited if the disposal challenges in the Permian Basin are not addressed by both operators and third-party companies.

Permian water disposal volumes contribute to more than 30% of the total disposed volumes in the onshore US, and in fact they have increased more than 40% between 2010 and 2019. In addition, disposal volumes in West Texas are expected to reach the highest level recorded in the last five years during 2019.

The industry has responded by increasing the recycle/reuse of produced water in fracking operations. Nevertheless, water recycling is not a "silver bullet" since the industry produces five times more water than needed to meet frack water demand.

Looking ahead, the development of the water midstream sector will be key to the development of the market overall. The signs of consolidation in a highly fragmented market could be the first clear step the industry is taking to face the challenges associated with the water lifecycle. Consolidation continues to be a strong industry trend within the water management service sector to reduce costs generally. The active M&A market at the beginning of 2019 involved third-party companies acquiring pipeline and localized water assets to reduce the use of water haulers and to centralize the disposal process. IHS Markit estimates this trend will continue towards the end of the year.

Learn more about our coverage of onshore materials, including proppant and pumping.

IHS Markit's Onshore Services & Materials' recent WaterIQ report for the first half of 2019 monitors and forecasts US oilfield water management market size and volumetrics along the different segments of the value chain. The report is available in its entirety on Connect™ for Onshore Services & Materials clients.

Paola Perez Pena is a Principal Research Analyst, Senior Associate at IHS Markit.

Posted 17 June 2019

This article was published by S&P Global Commodity Insights and not by S&P Global Ratings, which is a separately managed division of S&P Global.