Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Aug 10, 2020

Daily Global Market Summary - 10 August 2020

European equity markets closed higher across the region, while most major APAC and US markets were also higher on the day. European benchmark government bonds closed modestly higher, while US bonds were lower on the day. iTraxx and CDX high yield credit indices both closed wider and IG was close to flat, while oil, soybean, and gold futures closed modestly higher. On a positive note, data indicates that the pace of new COVID-19 infections and hospitalizations in the US appears to be slowing.

Americas

- Most US equity markets closed higher, except for Nasdaq -0.4%; Russell 2000 +1.0%, DJIA +1.3%, and S&P 500 +0.3%. Quarter-to-date, the Russell 2000 small cap index (+9.9% QTD) jumped ahead of the Nasdaq (QTD +9.0%) today.

- 10yr US govt bonds closed +2bps/0.58% yield.

- Gold closed +0.6%/$2,039 per ounce and was as high as $2,060 per ounce at 9:30am EST.

- CDX-NAIG closed +1bp/66bps and CDX-NAHY +4bps/391bps. CDX-NAHY

closed at its widest point of the day:

- The NY Fed published research today entitled 'Implications of

the COVID-19 Disruption for Corporate Leverage', which assesses the

preliminary impact of COVID-19 disruptions on the cash flow and

leverage of public U.S. corporations using public filings through

Q1 2020. In the report, the NY Fed uses the interest coverage ratio

(ICR) as their primary measure of corporate leverage. ICR is

calculated by dividing a company's EBITDA by its interest expense

in the same period. If a company's cash flow is less than its

interest expense, it may default on its debt if it is not able to

borrow additional money to cover those interest expenses. They

define a firm to be at risk of becoming delinquent and its debt

being at risk of default (debt-at-risk) whenever its ICR is less

than 1. Since the ICR does not account for cash flow needs related

to capital expenditures or working capital, even firms with an ICR

permanently above but close to 1 may be at risk of becoming

delinquent. The report highlights that "first quarter of 2020

includes only one month of pandemic-related disruptions (March), so

second-quarter earnings [and ICRs] are likely to be worse."

(Federal Reserve Bank of New York)

- For the first time in a month, fewer than 50,000 Americans are known to be hospitalized with COVID-19, according to data compiled by the COVID Tracking Project through Sunday. In Arizona, one of several states to have suffered a brutal July, the coronavirus hospitalization figures have dropped by about half. In Florida, they're down about a third from their peak last month, partly due to an easing of pressure on the Miami area. And in New York, where the pandemic hit hardest in its first onslaught, Governor Andrew Cuomo said Monday that the numbers fell to their lowest of the pandemic -- 535 hospitalized and 127 in the ICU statewide. (Bloomberg)

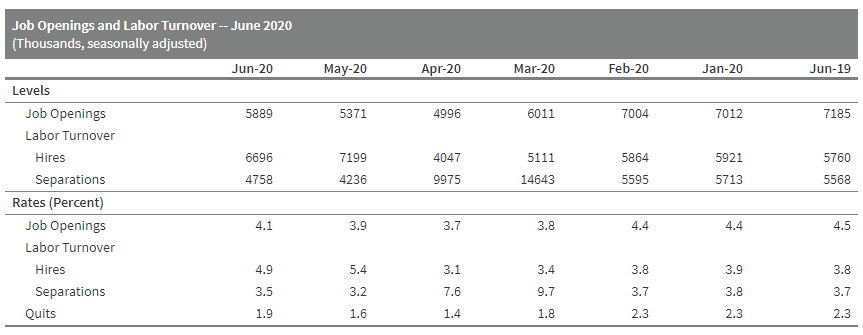

- The June JOLTS report illustrates the continued recovery in the

US labor market from the gradual resumption of economic activity

across the country. (IHS Markit Economist Akshat Goel)

- The number of hires decreased to 6.7 million in June after hitting an all-time high of 7.2 million in May. The number of job openings increased to 5.9 million in June.

- Job separations increased to 4.8 million in June after falling for two straight months; this is still less than half the all-time high of 10.0 million reached in April.

- The layoffs and discharges rate remained at 1.4% in June; the two-year pre-pandemic average of the rate was 1.2%.

- The quits rate, a valuable indicator of the general health of the labor market, continued to recover and rose to 1.9%; it is still well below its two-year pre-pandemic average of 2.3%.

- Over the 12 months ending in June, there was a net employment loss of 8.9 million.

- There were 3.0 workers competing for every job opening in June. In the two years prior to the pandemic, the number of job openings exceeded the number of unemployed in every report.

- The next few JOLTS reports will help to clarify the impact of

the resurgence in COVID-19 cases on the recovery on the labor

market.

- As of August 6, 79.3% of US households made a full or partial rent payment for the month of August, according to a survey conducted by the National Multifamily Housing Council, a residential developer trade group. That was down 1.9% from the same period a year earlier. Even though the headline numbers were generally solid, property executives noted that the proportion of renters who used credit cards to make their payments was increasing, one sign of growing financial strain. (FT)

- Crude oil closed +1.7%/$41.94 per barrel.

- Electric utilities are doing their part to increase the adoption of electric vehicles (EV) by providing incentives to charge at a lower rate during non-peak hours. To date, most utility initiatives have focused on make-ready public charging investments even though more than 80% of charging occurs at home. Xcel Energy's (Xcel) recently approved EV Home Service program is an innovative exception. By enrolling, EV owners can lower the cost of charging at home through time-of-use (TOU) electricity prices and home-charging equipment leases. Xcel will also use the home-charging equipment as the electricity meter (i.e., a submetering scheme). The cost of owning an EV will be lower under the EV Home Service program, making EVs more competitive with internal combustion engines (ICEs). (IHS Markit EnergyView Gas, Power, Renewables' Samir Nangia and Rachel Beaver)

- The US Environmental Protection Agency is preparing to adopt new rules that would rescind regulations for methane-gas emissions, including ending requirements that oil-and-gas producers have systems and procedures to detect methane leaks in their systems, senior administration officials said. The rule changes will apply to wells drilled since 2016 and going forward, and remove the largest pipelines, storage sites and other parts of the transmission system from EPA oversight of smog and greenhouse-gas emissions. (WSJ)

- Soybean futures gained across the board Monday with the nearby August contract up 6 1/4 cents to settle at $8.76 1/2. Futures where supported by US export and domestic demand. USDA announced private exporters reported sales of 111,000 tons of soybeans for delivery to unknown destinations and 588,000 tones for delivery to China, both for 2020/21. A portion of the sales to China were triggered by sales to a single destination during the reporting week being at 200,000 tons or more. Sales are required to be reported if they are for 100,000 tons or more to a single destination in a single day. That continued to provide support for futures despite trade concerns about US-China trade tensions. Futures also were supported Monday supported by strong weekly inspections of 635,665 tons for the week ended August 6. Some positioning ahead of USDA's Wednesday reports also factored into prices. Gains may have been tempered somewhat by favorable weather in much of the US Midwest and some rains forecast for areas that had begun to get dry. Funds bought a net 8,500 soybean and 2,500 soymeal contracts and were net even on soyoil, traders said. (IHS Markit Food and Agricultural Commodities' Wes Petkau)

- Jamaica's government is enjoying a rebound in popularity as a

tourist destination as a result of its COVID-19-virus-related

response and is likely to take advantage by calling an early

election before the economic situation deteriorates further in

2021. (IHS Markit Economists Ellie Vorhaben and Veronica Burford)

- Jamaica's Ministry of Tourism reported that 28,656 tourists arrived in Jamaica from 15 June, when the country reopened its tourism sector, to 20 July, a significant reduction compared with the 250,584 visitors that arrived in July 2019.

- IHS Markit forecasts that Jamaica's economy will contract by 7.2% in 2020, as both services and export activities are constrained by the impact of the COVID-19-virus spread. Jamaica's high dependency on tourism, which accounts for 34% of GDP, makes it particularly vulnerable to recession and travel restrictions in key countries such as the United States, Canada, and Europe. The goods-producing sectors are also at risk because of weaknesses in trade and manufacturing, which have driven down prices of key goods exports, including bauxite and alumina.

- The longer the ongoing tourism underperformance lasts, the more likely it is that the government will lose voters' support. Jamaica's tourism associations have estimated that the sector is unlikely to fully recover until 2023, with only 15% of businesses having reopened as of mid-July and with hotels currently reaching occupancy rates of 10-35%.

- The government is likely to call for an early election, taking advantage of its current approval ratings.

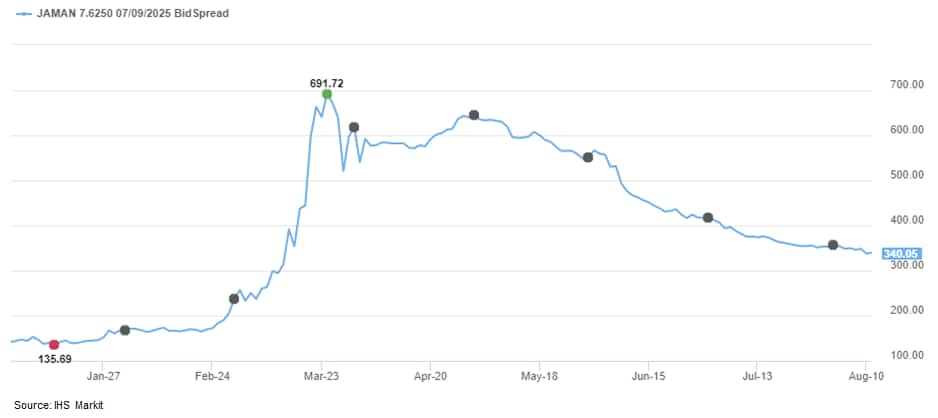

- The below graph shows the 2020 YTD spreads for the Government

of Jamaica's 7.625% 7/2025 bond, which has tightened over 350bps

from the widest level of UST +692bps on 24 March to UST +340bps as

of today's close:

Europe/Middle East/ Africa

- Most European equity markets closed higher today; Spain +1.5%, Italy +0.7%, France +0.4%, UK +0.2%, and Germany +0.1%.

- 10yr European govt bonds closed higher across the region; Spain/France/Germany -2bps and UK/Italy -1bp.

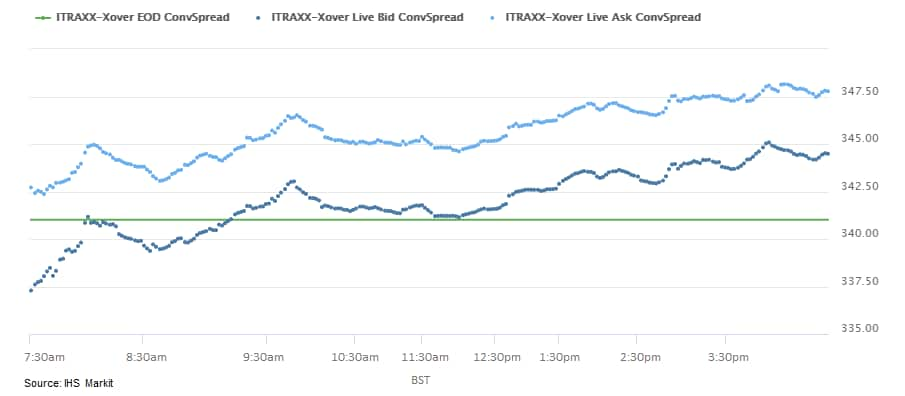

- iTraxx-Europe closed flat/54bps and iTraxx-Xover +6bps/347bps.

Similar to CDX-NAHY, iTraxx-Xover closed near its widest point of

the day.

- Brent crude closed +1.3%/$44.99 per barrel.

- Figures released by the National Institute of Statistics and

Economic Studies (Institut national de la statistique et des études

économiques: INSEE) show industrial production growing by 12.7%

month on month (m/m) in June. (IHS Markit Economist Diego Iscaro)

- Production had increased by 19.9% m/m in May and declined by 17.1% m/m and 20.6% m/m in March and April, respectively.

- Indeed, despite the latest increase, industrial production remained 11.7% below its level in June 2019 and 11.0% below its pre-pandemic level in February this year. Industrial production fell by 17.1% quarter on quarter (q/q) during the second quarter.

- Manufacture of transport equipment rose sharply during the previous two months (by 52.7% m/m in May and 39.5% m/m in June) but remained 13.7% below February's level (-35% for production of cars). Production of machinery and equipment also continued to recover in June (+14.6% m/m) but was still 13% below February's level.

- 'Flash' figures also released by the INSEE show private payroll employment declining by 119,400 q/q during the second quarter. This means that employment is now estimated to have fallen by 617,000 since the start of 2020, standing at its lowest level since the first quarter of 2017.

- The Bank of France on 10 August (today) released its monthly business conditions survey, where it estimates that activity was 7% below "normal" in July. This represents a modest improvement compared with -9% in June. At the height of the pandemic in March, activity was estimated to have been 32% below "normal".

- While activity in the recreation, hospitality, and advertising sectors remain well below "normal", activity in the construction sector is improving and now sits close to its pre-pandemic levels.

- State Secretariat for Economic Affairs (SECO) data reveal that

Swiss seasonally adjusted unemployment has increased by just 1,489

people or 1.0% m/m to 155,007 in July. (IHS Markit Economist Timo

Klein)

- This follows 153,518 in June, revised down by about 1,700. These numbers compare to the previous cycle's peak near 150,000 in mid-2016 and an interim low point of around 104,000 in the third quarter of 2019.

- The seasonally adjusted unemployment rate, which had hovered at 17-year lows of 2.3% in 2019, has remained steady at 3.3%. Upward momentum thus has slowed earlier than expected, enabled by the concurrence of eased administrative restrictions and still very high usage of the short-time work instrument.

- On balance, it now appears unlikely that the cyclical high of 4.1% seen in 2009 due to the global financial market crisis (GFC) will be revisited. Note this is measured against a fixed labor force figure used as denominator, which is currently at 4,636,100 (2015-17 average, used for rates since January 2017).

- Among other labor market indicators, seasonally adjusted job vacancies have bottomed out. They increased by 3.4% m/m to 29,670 in July, with June's level additionally being revised up modestly. The year-on-year decline has therefore been curtailed anew from -14% to -8%.

- As expected, the number of short-time workers - lagging by two months and unadjusted for seasonal variations - has come down from April's record-breaking peak of 1,077,000 to 891,000 in May (-17.3%).

- Nevertheless, this is still 223 times the mere 4,000 registered in February. The number of lost working hours even declined from April's 90.2 to 57.9 million in May (-35.8%), a level that is still 12 times larger than the maximum reached during the GFC in 2009. This reflects that the COVID-19 pandemic heavily impacted the service sector too this time, unlike the situation in 2008-09.

- Trustonic, a UK-based mobile cyber-security company announced that Megatronix, an automotive service provider has chosen its security platform to secure its SmartMega OS plus, an operating system that provides connected services to smart vehicles, according to company sources. Hycan 007, the first vehicle produced by GAC NIO New Energy Automotive Technology that integrates SmartMega OS plus, is currently on sale across China. In February 2019, Volkswagen (VW) and Trustonic announced that they were working together to allow customers to use smartphones to access their vehicles, as well as to securely share the digital car keys to grant access to others. Trustonic's Trusted Execution Environment (TEE), a hardware-based security enclave of the main processor, protects sensitive data by storing, processing and protecting it in an isolated, trusted environment, while Megatronix's SmartMega OS plus provides real-time cloud-based features that help in connectivity of vehicles to the external environment, while protecting communications from the Telematic Control Unit (TCU) to the connected cloud. (IHS Markit Automotive Mobility's Tarun Thakur)

Asia-Pacific

- APAC equity markets closed higher except for Hong Kong -0.6%; Australia +1.8%, South Korea +1.5%, China +0.8%, and India +0.4%.

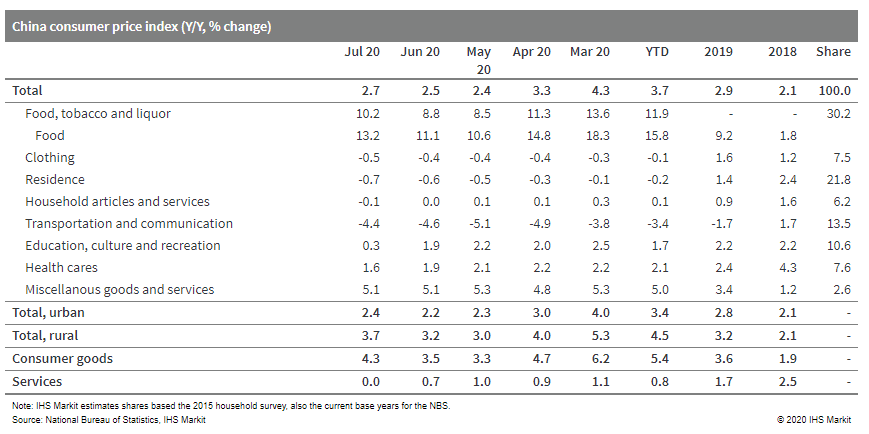

- Mainland China's consumer price index (CPI) registered at 2.7%

year on year in July, up by 0.2 percentage points from June,

according to the data released by the National Bureau of

Statistics. Month-on-month CPI also turned positive, after staying

in deflation territory for four consecutive months. (IHS Markit

Economist Lei Yi)

- By component, food price inflation remains the key factor driving up the headline CPI, as resuming catering businesses increasing their demand for pork and fresh vegetables while the flood disaster and relating transport distortions leading to supply shortages. Price inflation of non-food components remains weak, with only transportation slightly narrowing its price deflation. Core CPI excluding food and crude oil continued to edge down to 0.5% year on year, compared with 0.9% year on year in June.

- Producer price index (PPI) deflation narrowed to 2.4% year on year in July from 3.0% year on year in June, reflecting pickup in domestic and external demand. M/m PPI inflation stayed the same as June's reading of 0.4% gain; and 21 out of 40 surveyed industrial sectors reported m/m price increase, down by 1 from June.

- The rebound in global commodity prices continued to support the recovery, though the impact diminishes from upstream to downstream sectors. Prices in oil-related sectors continued to pick up month on month, led by petroleum and natural gas exploration and fuel processing. Prices in ferrous metals and non-ferrous metals smelting and pressing also kept recording month-on-month gains, though month-on-month inflation edges down for ferrous metals and up for non-ferrous metals. The output price of consumer goods manufacturing has continued rising as food manufacturing PPI sustained its upward momentum, and price deflation of durable consumer goods narrows thanks to the re-inflation in auto industry.

- Cumulatively, CPI rose by 3.7% year on year through July,

slightly down from the 3.8% year on year in the first half of 2020;

PPI deflated by 2.0% y/y through July, up from 1.9% year on year in

the first half.

- Great Wall recorded a 29.8% year-on-year (y/y) increase in

sales to 78,339 units during July. The strong rebound helped the

automaker to further narrow the gap in its year-to-date (YTD) sales

with last year's volumes. (IHS Markit AutoIntelligence's Abby Chun

Tu)

- Combined volumes in the YTD totaled 473,436 units, down 14.5% y/y.

- Total deliveries of the Haval brand increased by 10.8% y/y to 47,517 units in July, while sales of the premium WEY brand fell by 2.1 y/y to 7,091 units.

- Sales of the automaker's Wingle and P-series pick-ups totaled 20,661 units last month, up 155.9% y/y.

- Sales of the Ora electric vehicle (EV) brand, including the R1 and iQ models, totaled 3,064 units last month, compared with 2,071 units in last July.

- Great Wall's export volumes totaled 6,300 units in July. In the YTD, export volumes are reported at 26,836 units.

- Japan is said to have agreed that the timeline to eliminate import tariffs for vehicles and automotive components into the UK will be by 2026, reports the Nikkei. According to the Japanese newspaper, this has been reached as the two countries work towards a trade agreement in principle by the end of the month. This has been despite pressure from the Japanese negotiators to eliminate them sooner. The UK and Japan are undertaking trade negotiations as the UK is now on course to the leave the EU by the end of 2020. A deal between the UK and Japan would be an important step for the former, but is still subject to further negotiations according to the most recent reports, with agriculture being one area of contention. An agreement of this type with regards to auto tariffs will maintain the same steps towards tariff elimination as that agreed between Japan and the EU. (IHS Markit AutoIntelligence's Ian Fletcher)

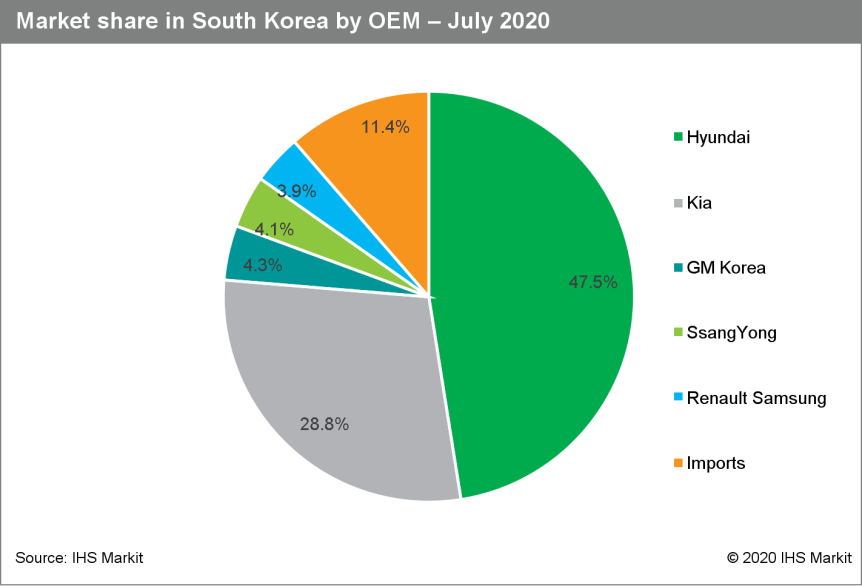

- New vehicle sales in South Korea, including passenger vehicle

imports, grew by 8.2% year on year (y/y) during July to 163,094

units, up from 150,588 units in July 2019, according to reports by

Yonhap News Agency and the Korea Automobile Importers and

Distributors Association (KAIDA), as compiled by IHS Markit. (IHS

Markit AutoIntelligence's Jamal Amir)

- The South Korean new vehicle market grew for the fifth consecutive month during July. The strong growth last month can be attributed to the solid performance by Hyundai and growth recorded by GM Korea, thanks to strong demand for newly launched models, attractive sales promotions by automakers, consumption tax relief on passenger vehicles, and a low base of comparison.

- In the year to date (YTD), total vehicle sales in the country stood at 1.08 million units, up by 6.8% y/y.

- Hyundai and Kia maintained their lead of the South Korean vehicle market in July with a combined share of 76.3%.

- Hyundai posted a 28.4% y/y increase in its monthly sales to 77,381 units, while its affiliate Kia recorded a marginal decrease of 0.1% y/y to 47,050 units.

- Hyundai said that the Grandeur (Azera) sedan led its domestic sales last month with 14,381 units. The strong performance of its premium Genesis brand, with the all-new G80 sedan and the GV80 sport utility vehicle (SUV), also helped to maintain robust sales momentum in South Korea.

- Kia said that its recently launched models, such as the next-generation K5 (Optima) sedan released in December 2019 and the Sorento SUV launched in March, contributed to the consistency in demand in the domestic market last month.

- General Motors (GM) Korea's sales grew by 3.5% y/y to 6,988 units in July.

- SsangYong's sales declined by 23.0% y/y to 6,702 units, while

Renault Samsung reported sales of 6,301 units during the month,

down by 24.2% y/y.

- New vehicle sales in Australia declined by 12.8% year on year

(y/y) during July to 72,505 units, according to data from the

Federal Chamber of Automotive Industries (FCAI). (IHS Markit

AutoIntelligence's Nitin Budhiraja)

- The sport utility vehicle (SUV) segment posted a sales decline of 3.5%% y/y to 36,560 units, while passenger car sales fell steeply to 18,149 units, down by 28.5% y/y.

- Sales of light commercial vehicles (LCVs) totaled 1,812 units, down by 10.8% y/y. During the month, Toyota was the best-selling brand with 15,508-unit sales. In second place was Mazda with 7,806 units, followed by Mitsubishi with 4,684 units, Hyundai with 4,634 units, and Kia with 4,625 units.

- The top-selling vehicle was the Toyota RAV4 with sales of 4,309 units, followed by the Ford Ranger (3,104 units) and the Toyota HiLux (2,947 units).

- The extended Stage 4 Restrictions which have now been invoked in Australia's second largest market, Victoria, will no doubt further challenge the industry during the coming months." On a year-to-date (YTD) basis, sales were down by 19.2% y/y to 514,920 units.

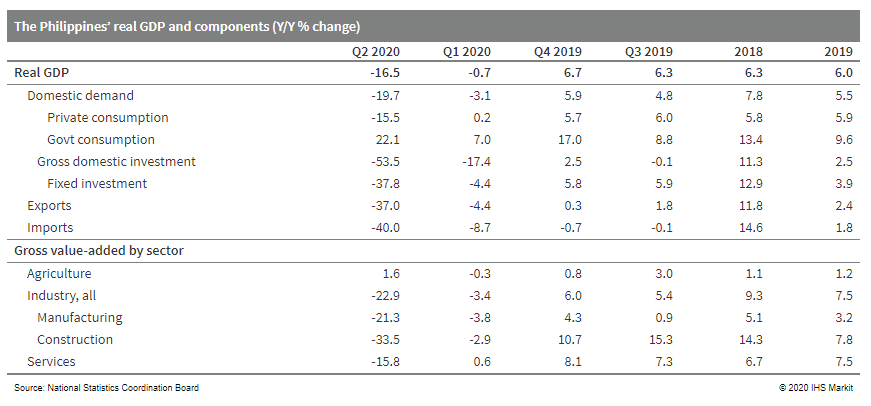

- The Philippines' real GDP plunged 16.5% year on year (y/y) in

the second quarter, marking the worst slump in history, even deeper

than the contractions posted during the 1998 Asian financial

crisis. In seasonally adjusted terms, the economy contracted at a

fresh record speed of 15.2% from the previous quarter, accelerating

sharply from a 5.7% drop posted in the first quarter. (IHS Markit

Economist Ling-Wei Chung)

- Double-digit percentage y/y contractions were seen across the board, except for government spending. In particular, domestic demand - once a key driver of growth - collapsed during the second quarter, dragging down real GDP by a dire 21.5 percentage points. The drag from domestic demand widened sharply from a 3.5-percentage-point subtraction in the first quarter.

- This was offset somewhat by a positive contribution from net exports as imports contracted at a quicker pace than exports. A global slump in demand and supply-chain disruptions, as well as travel restrictions across the world, meant total exports plunged, but the collapse in domestic demand led to a worse contraction in imports than exports and resulted in a 4.9-percentage-point contribution to second-quarter GDP from net exports.

- The government's strict COVID-19-virus-containment measures - so-called "enhanced community quarantine" measures - were imposed initially in March and were extended through May, before being eased gradually from the beginning of June. With around 75% of economic activities shut down, the impact of the strict measures was dire.

- Household consumption, accounting for around 70% of real GDP, tumbled 15.5% y/y during the second quarter, as consumption-related activities came to a standstill. The rate of contraction was the worst in history, which was led by a 60.5% y/y plunge in transport spending, a 66.4% y/y slump in spending on restaurants and hotels, and a 57.2% y/y drop in spending on recreation and culture.

- Coupled with the double-digit percentage falls in spending on furnishings, education, and other household items, these more than offset a 2.4% y/y increase in spending on food and non-alcoholic beverages.

- Concurrently, with virus-containment measures severely disrupting business activities and dampening sentiment, gross investment spending plunged 53.5% y/y, representing the largest contraction since the first quarter of 1985. Within that, fixed investment tumbled 37.8% y/y in the second quarter, driven by a 62.1% y/y plunge in business spending on durable equipment.

- In addition, another drag on fixed investment came from a 32.9% y/y drop in total construction investment as household-related construction investment tumbled 75% y/y and construction spending of financial and non-financial corporations contracted 27% y/y.

- Virus-containment measures also stalled the all-important infrastructure projects, with public construction investment falling 0.9% y/y in the second quarter, after shrinking 0.6% y/y in the first quarter. Coupled with a plunge in inventories, gross investment subtracted 13.9 percentage points from second-quarter GDP.

- Government consumption surged 22.1% y/y in the second quarter, as the government ramped up spending to combat the spread of the COVID-19 virus and bail out households and businesses hit badly by the pandemic. It was the fastest expansion in government consumption since the first quarter of 2012.

- On the external front, the slump in overseas demand and disruptions to global supply chains led to a 31.1% y/y drop in exports of goods, as shipments of office equipment, machinery and transport equipment, and electronic data processing plunged by more than 40% y/y during the second quarter.

- In addition, with tourism-related activities coming to a

standstill amid global travel restrictions, exports of services

tumbled 43.4% y/y during the second quarter. Together, exports of

goods and services contracted 37% y/y, marking the worst slump on

record.

- IHS Markit has downgraded Sri Lanka's medium-term risk rating

to 65 on IHS Markit's numerical scale (CCC on the generic scale)

from 60 (B-), and returned the medium-term outlook to Stable. IHS

Markit also downgraded Sri Lanka's short-term risk rating to 35

(BBB) from 30 (BBB+), and affirmed the short-term outlook as

Negative. These changes come from a worsening outlook for the

country's liquidity position and its continually rising debt

burdens. (IHS Markit Sovereign Risk's Andrew Vogel)

- Sri Lanka's external liquidity gap is at serious risk, given the expectations of poor foreign-exchange earnings due to the large drop in tourism revenues caused by the COVID-19 virus pandemic. Additionally, the need to service debts in foreign currencies will place additional stress upon this metric. The country's enactment and extension of capital controls in April and July respectively have demonstrated foreign-exchange reserves to be an area of concern, and overall act as a warning sign towards Sri Lanka's weakening liquidity position.

- The country's external debt has been rising substantially for many years to cover recurrent fiscal and current-account deficits, and includes non-concessional borrowing and commercial short-term loans. Alongside these increasing liabilities comes increasing risk to Sri Lanka's ability to service its debts, especially given the uncertain outlook for future foreign-exchange inflows and the risk of substantial depreciation of the exchange rate.

- Similarly, the current-account balance for Sri Lanka is skewed heavily to the downside as the COVID-19 virus pandemic restricts global demand and international travel, seriously damaging Sri Lanka's export position - particularly tourism services exports. In the short term, import restrictions and muted oil prices should keep the import bill in check, and both the Extended Fund Facility agreement with the International Monetary Fund and the renewal of concessions under the European Union's Generalized System of Preferences Plus scheme should provide some relief, but macroeconomic imbalances remain.

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-10-august-2020.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-10-august-2020.html&text=Daily+Global+Market+Summary+-+10+August+2020+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-10-august-2020.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - 10 August 2020 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-10-august-2020.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+10+August+2020+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-10-august-2020.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}