Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Aug 11, 2020

Daily Global Market Summary - 11 August 2020

European equity markets closed higher on the day, while China was the only major APAC market to end the day lower. US equity markets, except for tech, were higher for most of the day until suddenly selling off shortly after 3:00pm to end the session lower due to waning hopes that a US stimulus bill will be passed in the near term. Precious metals closed sharply lower, with gold and silver reporting the largest daily percentage declines since mid-March. iTraxx closed tighter across IG and high yield, while CDX closed modestly wider. Government bonds closed lower across Europe and the US, with US bonds recovering to a small extent during the late-day flight to quality.

Americas

- The US stock market tumbled into the red in the last hour of trading on Tuesday after the Republican leader in the Senate Mitch McConnell said there had been no talks on a new economic stimulus package since Friday, denting hopes for an imminent deal. (FT)

- US equity markets declined sharply at approximately 3:10pm EST on Senator McConnell's statement to end lower across the major indices, despite most being higher on the day up until that point; Nasdaq -1.7%, S&P 500 -0.8%, and Russell 2000 -0.6%.

- 10yr US govt bonds closed +6bps/0.64% yield and was +8bps at its lowest point of the day at 2:57pm EST. 30yr bonds closed +8bps/1.34% yield.

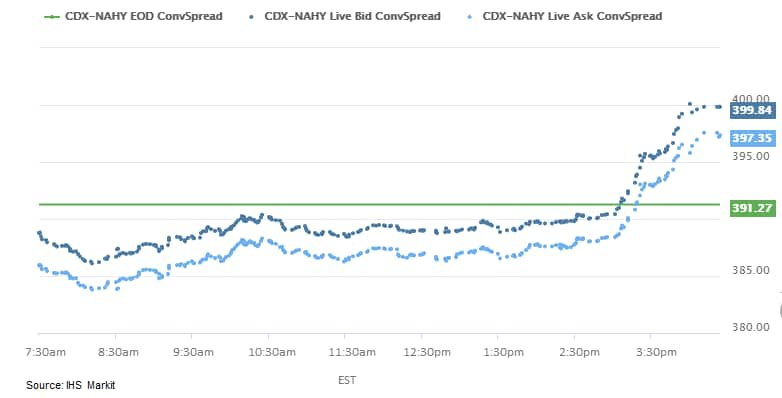

- CDX-NAIG closed +1bp/67bps and CDX-NAHY +7bps/399bps (intraday

chart below).

- Gold closed-4.6%/$1,946 per ounce (10-day price chart below), which is its worst daily percentage decline since 13 March.

- Silver closed -11.0%/$26.05 per ounce (10-day price chart below), which is its worst daily percentage decline since 16 March.

- Crude oil closed -0.8%/$41.61 per barrel.

- The Big Ten Conference announced shortly after 3:00pm EST that they voted today to postpone college football and other fall sports because of the coronavirus pandemic, a move that could begin the final unraveling of a lucrative season that collegiate sports officials have labored for months to save. (WSJ)

- The US total producer price index (PPI) for final demand rose

0.6% in July, its largest monthly gain since October 2018. This

followed a string of mostly pandemic-related drops in producer

prices that drove the PPI into the negatives during four of the

prior five months. (IHS Markit Economists David Deull and Michael

Montgomery)

- Total goods prices rose 0.8% with food down 0.5% and fuels up 5.3%. Core goods posted a moderate 0.3% firming.

- The relatively quiet month for food prices came as a rise in dairy prices did a little to offset the continued unwinding of the 69% jump in beef and veal prices in May, the result of the interrupted operations at meatpacking plants.

- Energy goods' 5.3% increase was the third solid month of gains after far steeper drops between February and April. The 12-month change of PPI energy goods was -13.5%.

- Total services prices posted a 0.5% increase, with trade margins up 0.8%, transportation and warehousing down 0.8%, and "other" services up 0.4%. Transportation and warehousing services were dragged down mainly by a 7.0% drop in passenger airfares.

- Within the trade margins group, major movers included a 5.1% drop in gasoline station margins but a 20.5% jump in auto retailer margins. Over short spans, trade margins tend to run counter to goods prices. Gasoline stations, for example, trim prices a bit more slowly than wholesale prices fall when the price of oil plunges, but margins return to more normal levels when wholesale prices climb.

- A 10.1% increase in gasoline prices in July trimmed the gasoline margin further back closer toward its year-earlier level, though it was still up 26.2%.

- In terms of 12-month changes, the headline PPI was down 0.4% in July, with goods down 2.0% and services up 0.3%. Excluding food and energy, the PPI was up 0.3%, and also excluding trade margins, prices were up a mere 0.1% from a year before—the first month in four with this figure above water.

- Yelp Inc., the online reviewer, has data showing more than 80,000 permanently shuttered from March 1 to July 25. About 60,000 were local businesses, or firms with fewer than five locations. About 800 small businesses did indeed file for Chapter 11 bankruptcy from mid-February to July 31, according to the American Bankruptcy Institute, and the trade group expects the 2020 total could be up 36% from last year. (Bloomberg)

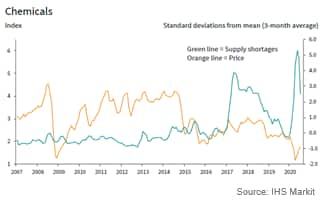

- Chemical prices continued to recover in July from their

collapse earlier this year. The IHS Markit Chemical Prices Index

rose 6% during the month, leading to an overall 51% increase from

April's 18-year low. The latest mark-up was largely due to a

rebound in global demand following the economic impact of the

COVID-19 pandemic. All three monitored commodities rose for the

third successive month, led by polypropylene which increased by 9%.

Rubber prices climbed 6%, while polyethylene saw the smallest

uptick of just 4%. Only rubber was in line with its 24-month

average; both polypropylene and polyethylene prices remained

relatively weak. At the same time, panel mentions of chemical

shortages continued to decrease in July, having reached a record

high in May. That said, supply concerns were still relatively

strong as some countries kept lockdown restrictions in place. (IHS

Markit Purchasing Managers' David Owen)

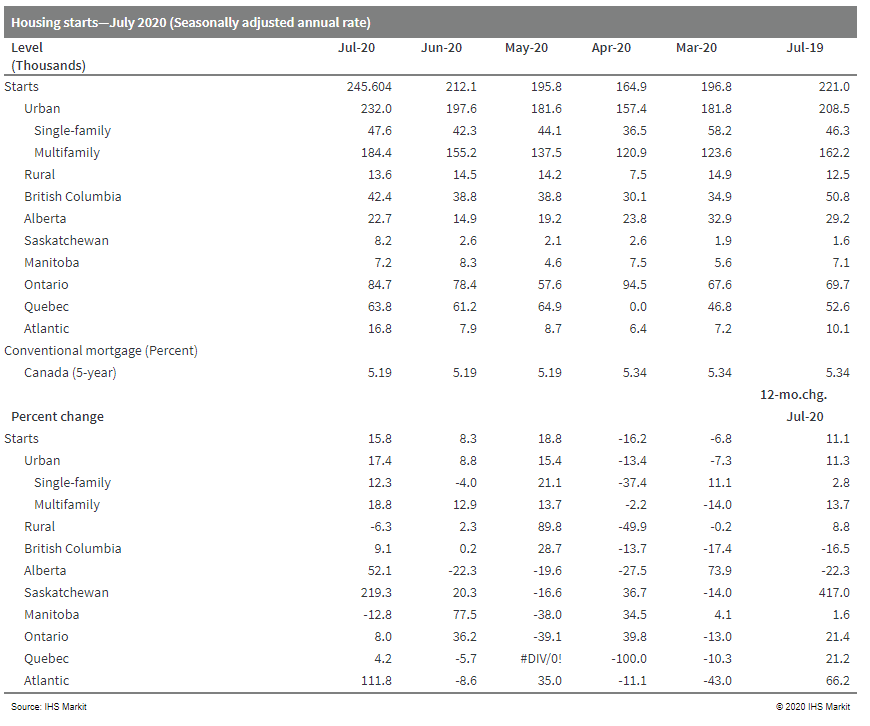

- Total housing starts in Canada increased 15.8% month on month

(m/m) to 245,604 units in July, which was the highest level since

November 2017. (IHS Markit Economist Jeannine Cataldi)

- Both urban single-family and multifamily units showed strong growth, at 12.3% and 18.8% m/m, respectively, while rural starts declined 6.3% m/m.

- All provinces except for Manitoba reported higher levels of housing starts in July m/m.

- The strongest rates of increase were in Saskatchewan and the Atlantic Provinces.

- With low interest rates and strong housing demand, real business residential investment is expected to rebound solidly in the third quarter.

- Urban housing starts in Canada increased 17.4% m/m in July.

Growth was led by an 18.8% m/m increase in multifamily starts.

Regionally, the increase in multifamily starts was widespread, led

by Alberta, Saskatchewan, Nova Scotia, and New Brunswick. Urban

single-family starts increased by 12.3% m/m in July, erasing the

decline from the previous month as Ontario's single starts jumped

21.4% m/m.

- Startup Nikola Motor has announced an order for 2,500 battery-electric waste trucks, with the option to increase to 5,000 units, with refuse company Republic Services. Deliveries are scheduled to begin in 2023, with on-road testing "likely" to begin in early 2022, according to Nikola's statement. Nikola will provide the truck chassis and body to Republic Services, which is a waste collection company operating in 41 US states. The truck is expected to drive 150 miles and be able to collect from 1,200 cans on a single charge. Nikola founder and executive chairman Trevor Milton said, "Nikola specializes in heavy-duty, zero-emission Class 8 trucks. The refuse market is one of the most stable markets in the industry and provides long-term shareholder value. The Nikola Tre powertrain is ideal for the refuse market as it shares and uses the same batteries, controls, inverters and e-axle. By sharing the Tre platform, we can drive the cost down for both programs by using the same parts. Refuse trucks are a logical application for electric vehicles, in part on relatively short routes with stop-and-go operations that can lead to the opportunity for regenerative braking to help recoup some battery power on the road. According to Republic Services' 2019 annual report, the company has about 16,000 refuse trucks in service, with an average age of 7.6 years. Ahead of the Nikola order, Republic's annual report said it was focusing on converting its fleet to compressed natural gas (CNG) and operates 39 CNG fueling stations, although it is also evaluating alternative fuel solutions. Nikola notes that the first deliveries are scheduled for 2023, although it does not say how long it will take to complete the order. (IHS Markit AutoIntelligence's Stephanie Brinley)

- PPG Industries says that its July sequential sales increase came in better than the company had previously anticipated. July sales volumes were down 6-11% year on year (YOY), compared with a previously expected 8-15% YOY decrease. This represents "a continuation of the solid demand recovery experienced in June," PPG says. Margins also improved in July. "Led by improving demand trends in our Chinese and European businesses across a variety of coatings end-use markets and in global industrial production, our July sales increased sequentially from the month of June and were down 7% compared to the prior year," says Michael McGarry, chairman and CEO of PPG. "Our diverse and global business portfolio is providing benefits from the demand recovery as it happens across different geographies and end-use markets. We remain focused on aggressively managing our costs, including executing the previously communicated restructuring programs, to support strong operating margin leverage as demand continues to improve." Further details, including exact sales figures, will be included in the company's third-quarter earnings release in October.

- The Organization for Economic Co-operation and Development (OECD) has warned that COVID-19 will weaken agri-food demand in the coming year and maybe longer. In a new analysis, the OECD explored the potential macroeconomic impacts of the COVID‐19 pandemic on food demand and identified a potential oversupply in many agricultural commodities. The team of economists said this would be driven by farmers addressing previous delays in production which may cause a glut in the short run and eventually see an increase in global commodity stocks. The OECD analysis said this would be reinforced by an expected slump in oil prices over the coming two years, which would incentivize more agricultural production because of the sector's access to cheaper fuel and fertilizers. They predict that these factors will combine to cause global vegetable oil prices to drop by 17%, beef and veal by 14%, butter by about 13%, pig meat by 11%, cheese by 10%, poultry by 9%, wheat by 8% and rice by 6%. (IHS Markit Food and Agricultural Policy's Steve Gillman)

Europe/Middle East/ Africa

- European equity markets closed higher across the region; Spain +3.0%, Italy +2.8%, France +2.4%, Germany +2.0%, and UK +1.7%.

- 10yr European govt bonds closed lower across the region; UK +7bps, Germany +5bps, France +4bps, and Spain/Italy +3bps.

- iTraxx-Europe closed -1bp/53bps and iTraxx-Xover -4bps/342bps.

- Brent crude closed -1.1%/$44.50 per barrel.

- According to the Office for National Statistics (ONS), the

number of UK workers on payroll plunged by 730,000, or 2.2%,

between March and July. The new release is based on experimental

data of the number of employees on payroll using the HM Revenue and

Customs' Pay As You Earn Real Time. (IHS Markit Economist Raj

Badiani)

- The claimant count, which measures the number of people claiming benefit principally for being unemployed, rose to 2.7 million in July and represented an increase of 116.8%, or 1.44 million, since March. The claimant count also includes the increasing number of people becoming eligible for unemployment-related benefit support despite still being employed.

- According to the ONS, total UK employment (all aged 16-plus) shrunk by 220,000 to 32.924 million in the three months to June compared with the three months to March, the largest quarterly decline since May-July 2009, the height of the financial crisis.

- In annual terms, the employment rate in the three months to June was 0.3% higher compared with a year earlier.

- The ONS reports that the number of self-employed shrunk by 199,000 year on year (y/y) to 4.76 million compared with a year earlier.

- The number of unemployed people on the Labour Force Survey (LFS) or the International Labour Organization (ILO) measure decreased by 10,000 in the three months to June, standing at 1.338 million.

- The unemployment rate remained at 3.9%, at odds with falling employment during the period.

- The statistics department argues that the stable unemployment

rate during the COVID-19 virus crisis is driven by these factors:

- A larger number of people who left their jobs are not currently looking for a new one and are therefore becoming economically inactive, rather than unemployed.

- An increased number of respondents who were previously unemployed had moved to economic inactivity in March-May, suggesting that some who were previously unemployed are no longer looking for a job.

- The current unemployment rate is lagging, with some information gathered before the lockdown began.

- The average annual weekly earnings (total pay including bonuses) growth slowed by 0.9 percentage points to -1.2% in the three months to June. In addition, regular pay (which excludes bonus payments) growth slowed for the 11th straight month to -0.2% y/y in the three months to June.

- Total pay in real terms fell by a sharper 2.0% y/y in the three months to June, which was the third drop since January 2018.

- Bayer says that it will acquire KaNDy Therapeutics (Stevenage, UK), a clinical-stage biotechnology company, to expand Bayer's drug-development pipeline in women's healthcare. Bayer will pay an upfront consideration of $425 million and potential milestone payments of up to $450 million until launch followed by potential additional triple-digit-million sales milestone payments, under the terms of the agreement, the company says. Completion of the deal is subject to customary conditions, in particular antitrust approval, and is expected by next month, Bayer says. The transaction is another step in augmenting Bayer's own women's healthcare portfolio through collaborations and agreements, it says. "Bayer is focusing on innovative options to address the unmet medical needs of women worldwide," says Stefan Oelrich, board member and president/pharmaceuticals at Bayer. "With this acquisition Bayer will broaden its women's healthcare pipeline by adding a potential novel non-hormonal oral treatment option for women during menopause." Bayer's pharmaceuticals business's development and licensing team facilitated the transaction, it says. Morgan Stanley is serving as financial advisor to Bayer, with Linklaters serving as legal counsel, the company says. Goldman Sachs International is serving as financial advisor to KaNDy Therapeutics and Goodwin is serving as legal counsel.

- Germany's Ibeo Automotive System will supply its solid-state LiDAR, ibeoNEXT, for a new generation of vehicles built by China's Great Wall Motor from 2022. Ibeo will develop the sensor using Austrian company AMS's vertical cavity surface-emitting laser (VCSEL) technology. LiDAR sensors are necessary for autonomous vehicle operation as they measure distance via pulses of laser light and generate 3D maps of the world around them. IbeoNEXT will provide Great Wall Motor's vehicles with a highway pilot to drive semi-autonomously at Level 3. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- ZF Friedrichshafen has posted a combined net loss of EUR911 million in the first half of 2020, according to a company statement. This follows a huge decline in revenue as a result of the coronavirus disease 2019 (COVID-19)-virus pandemic to EUR13.5 billion, a fall of 27% year on year (y/y) from EUR18.4 billion during the equivalent period last year. Like other major Tier-1 suppliers and OEMs, ZF rapidly instigated a program of cost savings and efficiencies that helped to keep the overall adjusted earnings before interest and taxes (EBIT) loss at EUR177 million. Like its major Tier-1 rivals such as Continental, ZF has responded very rapidly to the challenge of the huge drop in global vehicle production in the first half of the year through strict cost-management program and the idling of plants where necessary. The company is responding to short- and long-term challenges alike, with 50,000 workers in Germany working flex hours through the so-called 'Transformation Collective Agreement'. In addition, the company will also form a new division from the current Car Powertrain Technology and E-Mobility divisions to offer customers electrified driveline solutions from a single source. (IHS Markit AutoIntelligence's Tim Urquhart)

- A report commissioned on behalf of US pharmaceutical company Biogen forecasts that the healthcare and societal costs from dementia and Alzheimer's disease conditions in Norway will reach NOK182 billion (USD20 billion) per year over the next two decades. This represents an increase from an estimated cost to the Norwegian society today of NOK95 billion. Nearly half of the projected NOK182 billion cost per annum is attributed directly to healthcare. The report concludes that Norway's municipal authorities will bear the largest financial pressures. These authorities currently account for about 80% of the costs associated with the care of dementia patients. Norway's ageing demographics over the next 20 years is also predicted to increase the number of dementia patients diagnosed and the related financial pressures that are placed on municipal authorities. The model is based on the prediction that the number of dementia cases will increase from 80,000 today to 180,000 by 2040, according to the Norwegian Public Health Association. (IHS Markit Life Sciences' Eóin Ryan)

- The Central Bank of Russia (CBR) announced on 10 August that it will extend some of the regulatory relief measures implemented in connection to the COVID-19-virus pandemic outbreak. Most of the previously adopted measures were set to expire by the end of September, but given rising credit risks and slowdown in lending, the regulator has extended the support until 31 December. In particular, the regulator has extended forbearance measures regarding provisioning to restructured loans for individuals and small and medium-sized enterprises (SMEs), has lowered the premiums to the risk ratios for unsecured consumer loans, and has kept the countercyclical capital buffer at zero. However, the CBR has stressed that provisions for loans restructured before the end of 2020 must be formed in full by 1 July 2021. The CBR has also decided not to extend certain liquidity easing measures, citing the improvement of the banking-sector liquidity since the start of the pandemic. According to the preliminary estimates of the central bank, the year-on-year deposit growth had reached 11.6% as of 1 August versus 10% as of 1 June. Between 20 March and 29 July, banks restructured loans from 2.4 million individual borrowers. Earlier this month, the CBR said that July data showed a sustained trend towards decreasing number of individuals applying for loan restructuring, whereas the number of applications submitted by SMEs was almost the same. (IHS Markit Economist Lilit Gevorgyan)

- The Central Bank of the United Arab Emirates (CBUAE) announced additional COVID-19-virus-related support measures for the banking sector on 8 August. The CBUAE will allow banks to breach the net stable funding ratio (NSFR), lowering the minimum ratio to 90%. Additionally, the CBUAE will relax the advances to stable resources ratio (ASRR), raising the maximum ratio to 110%. The central bank's statement said that the relaxation will "provide banks with enhanced flexibility in managing their balance sheets". Both measures will be in effect until end-2021. The CBUAE also announced that the central bank's zero-interest loan facility, announced as part of the Targeted Economic Support Scheme (TESS), should be treated as stable funding when calculating liquidity ratios, with 50% weights. (IHS Markit Banking Risk's Gabrielle Ventura)

- Sasol has issued a trading statement in advance of releasing

its financial results for the fiscal year ended 30 June 2020. The

company warns of a large annual loss on impairment charges totaling

almost 112 billion South African rand ($6.3 billion).

- Sasol says that its performance in the fiscal year was pressured by the COVID-19 pandemic and "a severe decline in crude oil and chemical product prices." This was partly mitigated by a strong cash cost, working capital, and capital expenditure performance, the company says.

- Sasol expects to post a full-year headline loss per share of between R8.72 and R14.86 compared with headline earnings per share of R30.72 in the previous fiscal year.

- Sasol says it is taking the impairments following the decline in the long-term macroeconomic outlook, and a fair value impact following the commencement of partnering discussions for the company's base chemicals assets in the US. Base chemicals, primarily in the US, account for R71.3 billion of the R111.5-billion impairments. Performance Chemicals account for R27.7 billion of the impairments, primarily related to Sasol's "share of ethylene-producing assets in the US." The company's energy business accounts for the remaining R12.5 billion of impairments "across the portfolio," Sasol says.

- The company expects its full-year adjusted EBITDA to drop by between 17% and 37% from R47.6 billion in the prior year, to between R30.0 billion and R39.5 billion. "This results from an 18% decrease in the rand per barrel price of Brent crude oil coupled with much softer global chemical and refining margins impacting our gross margins adversely, especially during the second half of the 2020 financial year," Sasol says.

- Depreciation of R3.9 billion attributable to the production units at Sasol's Lake Charles Chemicals Project (LCCP) in Louisiana that have reached beneficial operation will also be included in Sasol's full-year results, the company says.

- Sasol is scheduled to publish its results for the full fiscal year on 17 August.

- CPChem, ExxonMobil, Hanwha Solutions, Ineos, and LyondellBasell have each expressed an interest in buying a stake in Sasol's US base chemicals assets, primarily the LCCP, according to press reports.

- The Business Daily reported on 11 August that the Kenya Mortgage Refinance Company (KMRC) will start operating before 30 September. The KMRC has been set up with an ownership split between the government (25% stake), financial companies including banks, and the World Bank's International Finance Corporations. The KMRC aims to provide long-term lending to banks at a concessionary rate of 5%, which will then be lent to mortgage borrowers at 7%, a discount from the average market interest rate of nearly 12%. To be eligible for the lower mortgage rate of 7%, borrowers have to earn less than KES150,000 (USD1,374) a month. (IHS Markit Banking Risk's Angus Lam)

- The monetary policy committee of the Democratic Republic of the

Congo's central bank decided to keep the key interest rates

unchanged at the end of July, having last cut the rates during an

emergency meeting on 24 March, wary of increasing downside risks to

the economy stemming from the COVID-19-virus pandemic and liquidity

concerns. The bank has also announced that it will introduce

measures for its exchange market. (IHS Markit Economist Alisa

Strobel)

- The monetary policy committee (MPC) of the Democratic Republic of the Congo (DRC)'s central bank, the Banque Centrale du Congo (BCC), met on 29 July to discuss the latest developments in the domestic economy and the implications of current global economic conditions for the country's macroeconomic growth performance. The emphasis of this special meeting with the BCC's Governor Mutombo Mwana Nyembo was to discuss the latest depreciation trend of the Congolese franc.

- The MPC decided at the meeting to maintain the BCC's key policy rates, after cutting the discount rate from 9% to 7.5% in March. However, the committee also announced that it will intervene in the country's exchange market via direct and indict measures such as puncturing the obligatory reserve requirement to improve currency offerings in the market and stabilize the Congolese franc.

- The latest move by the BCC comes as no surprise, as IHS Markit has previously indicated that we expect to see further BCC interventions to support the Congolese franc, including liquidity injections into the banking sector. On 27 July, the DRC's foreign reserves reached USD836.11 million, down by USD81.11 million recorded at the end of May, which is equivalent to three weeks of import cover. We maintain our view that given the low reserves, increased inflation risks, and a deteriorating currency, space for monetary policy adjustments in the form of further rate cuts is limited.

Asia-Pacific

- Most APAC equity markets closed higher except China -1.2%; Hong Kong +2.1%, Japan +1.9%, South Korea +1.4%, India +0.6%, and Australia +0.5%.

- The Chinese vehicle market experienced its fourth consecutive

month of growth in July. New vehicle sales on a wholesale basis

increased by 16.4% year on year (y/y) to 2.11 million units during

the month, while production rose by 21.9% y/y to 2.20 million

units, according to preliminary data from the China Association of

Automobile Manufacturers (CAAM). (IHS Markit AutoIntelligence's

Abby Chun Tu)

- Thanks to a rebound in new vehicle demand that began in April, vehicle sales and production volumes in the year to date (YTD) are narrowing the gap each month with the equivalent period of last year. In the YTD for July, China's new vehicle sales were down 12.7% y/y at 12.37 million units, while production volumes contracted by 11.8% y/y to 12.31 million units.

- The passenger vehicle (PV) market posted an increase of 8.5% y/y to 1.665 million units in July, while PV production increased by 13.2% y/y to 1.730 million units. The CAAM definition of passenger vehicles includes sedans, sport utility vehicles (SUVs), multi-purpose vehicles (MPVs), and minivans.

- In the YTD, sales of PVs were down 18.4% y/y at 9.533 million units, while production of PVs fell 17.8% y/y to 9.483 million units.

- Sedan sales in the YTD declined by 22.1% y/y, SUV sales fell by 11% y/y, MPV sales plummeted by 40.6% y/y, and microvan sales fell by 15.8% y/y.

- Commercial vehicle sales continue to rally. Sales volumes of commercial vehicles surged 59.4% y/y to 447,000 units during July, contributing to the strong rebound in new vehicle sales.

- Driven by surging market demand, commercial vehicle production increased 70.3% y/y to 472,000 units in July.

- In the YTD, sales of commercial vehicles were up by 14.3% y/y at 2.832 million units, while production of commercial vehicles increased by 16.4% y/y to 2.831 million units.

- Sales of new energy vehicles (NEVs) - which include battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and fuel-cell vehicles (FCVs) - increased 19.3% y/y to 98,000 units in July, while NEV production rose by 15.6% y/y to 100,000 units.

- Sales of BEVs grew by 24.2% y/y to 78,000 units in July, while production of BEVs increased by 17.9% y/y to 79,000 units.

- Sales of PHEVs totaled 19,000 units (up 2.7% y/y) in July, while production of PHEVs increased 7.8% y/y to 21,000 units.

- In the YTD, sales of NEVs were reported at 486,000 units (down 32.8% y/y), while NEV production volumes were down 31.7% y/y to 496,000 units.

- Bridgestone has reported a consolidated net loss of JPY22.04

billion (USD208 million) during the first half of 2020, compared

with a profit of JPY98.7 billion in the same period last year,

according to a company statement. (IHS Markit AutoIntelligence's

Nitin Budhiraja)

- Revenues were down by 22.1% year on year (y/y) to JPY1.355 trillion during the period and operating income declined by 86.7% y/y to JPY19.76 billion.

- Revenues from Japan were down by 18% y/y to JPY357.3 billion, revenues from the Americas fell by 22% y/y to JPY646.7 billion, while China and Asia Pacific experienced a 23% y/y decline in revenue to JPY181.7 billion.

- For the full year 2020, Bridgestone has projected a 23% decrease in total revenue to JPY2.7 trillion and an adjusted operating profit of JPY100 billion, down by 70.2%.

- The forecast is based on the assumption that there is a possibility of a second wave of the COVID-19 virus globally and that there will be a decrease in demand in the fourth quarter of 2020.

- Bridgestone has not commented on the expected consolidated profit attributable to the equity holders.

- Bridgestone experienced JPY23.8 billion in losses owing to the COVID-19 virus outbreak, including JPY11.9 billion owing to plant shutdowns and JPY11.9 billion on account of the impairment of assets for business use in Russia.

- Japan's Ministry of Heath, Labor and Welfare (MHLW) plans to award a total of JPY90 billion (USD850 million) in grants to six pharmaceutical companies to support an expansion of manufacturing capacity for the domestic supply of coronavirus disease 2019 (COVID-19) vaccines, the MHLW said in a statement. The MHLW awarded grants to Takeda (Japan; JPY30.1 billion), Shionogi (Japan; JPY22.3 billion), AstraZeneca (UK; JPY16.2 billion), AnGes (Japan; JPY9.4 billion), KM Biologics (Japan; JPY6.1 billion), and Daiichi Sankyo (Japan; JPY6 billion). Pharma Japan cited Health Minister Katsunobu Kato as saying that the six drug makers were selected from nine applicants. The grants are part of the Japanese government's second supplementary budget that was approved in June, under which JPY145.5 billion was allocated to expedite the commercialization of COVID-19 vaccines. (IHS Markit Life Sciences' Sophie Cairns)

- A Japanese town in Gunma Prefecture will begin a trial of a driverless amphibious tour bus this year, reports The Japan Times. The trial - which is the first of its kind in the world - will operate around the Yamba Dam in Naganohara, and is being conducted as a part of a project to "foster tourism and facilitate the transport of goods between islands". Organizations involved in the project will conduct research and development on the 40-seat autonomous bus for two years, with the aim of putting the vehicle into practical use in five years. The team has set a fiscal year 2020 budget of JPY250 million (USD2.36 million) for the project. (IHD Markit Automotive Mobility's Surabhi Rajpal)

- Murphy is targeting FDP (field development plan) submission for Lac Da Vang (LDV) field in Block 15-1/05 in the Cuu Long Basin, off Vietnam in the third quarter of 2020. The operator has received approval of the LDV retainment/development area. The ODP (overall development plan) was approved in August 2019. Development of LDV involves a minimum facility WHP (wellhead platform). Other planned facilities include a FSO (floating storage and offloading) vessel for condensate and tie-back flowlines to the existing production facilities on Cuu Long JOC-operated Block 15-1 in the vicinity. First oil is anticipated in 2022. Murphy has a 40% operating interest in Block 15-1/05 with partners PVEP (35%) and SK Innovation (25%). (IHS Markit Upstream Costs and Technology's Kelvin Sam)

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-11-august-2020.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-11-august-2020.html&text=Daily+Global+Market+Summary+-+11+August+2020+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-11-august-2020.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - 11 August 2020 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-11-august-2020.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+11+August+2020+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-11-august-2020.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}