Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Jul 13, 2021

Daily Global Market Summary - 13 July 2021

Most major APAC equity indices closed higher, US indices closed lower, and Europe was mixed. US government bonds closed sharply lower after being modestly higher during the first half of the trading session, while most benchmark European bonds were higher on the day. CDX-NA closed wider across IG and high yield, iTraxx-Xover closed wider, and iTraxx-Europe was flat. The US dollar, oil, and gold closed higher, while copper, silver, and natural gas were lower on the day.

Please note that we are now including a link to the profiles of contributing authors who are available for one-on-one discussions through our newly launched Experts by IHS Markit platform.

Americas

- All major US equity indices closed lower; DJIA -0.3%, S&P 500/Nasdaq -0.4%, and Russell 2000 -1.9%.

- 10yr US govt bonds closed +6bps/1.42% yield and 30yr bonds +5bps/2.05% yield.

- Today's higher than expected US CPI report led to a 'hybrid' reaction in 10yr US govt bonds that mirrored components of each of the two prior CPI releases. Today's price action mimicked the modest rally that occurred on the 10 June release until selling off 8bps after 1:05pm ET to mirror the extreme sell-off that occurred on the 12 May release.

- CDX-NAIG closed +1bp/49bps and CDX-NAHY +3bps/280bps.

- DXY US dollar index closed +0.5%/92.75, surging +0.4% during the 50 minutes that followed the release of the US CPI report.

- Gold closed +0.2%/$1,810 per troy oz, silver -0.4%/$26.14 per troy oz, and copper -0.2%/$4.31 per pound.

- Crude oil closed +1.6%/$75.25 per barrel and natural gas closed -1.4%/$3.70 per mmbtu.

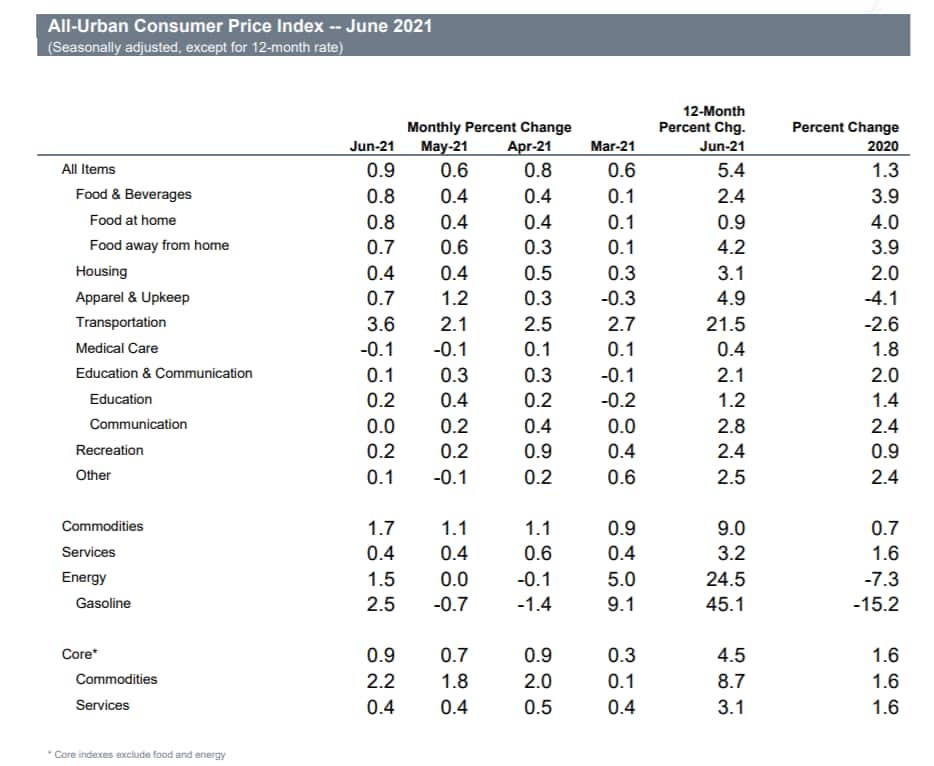

- The US consumer price index (CPI) and the core CPI (which

excludes the direct effects of moves in food and energy prices)

each rose 0.9% in June. The CPIs for food and energy rose 0.8% and

1.5%, respectively. (IHS Markit Economists Ken

Matheny and Juan

Turcios)

- Twelve-month changes in overall and core indices rose in June to 5.4% and 4.5%, respectively. As in previous months, headline CPI figures were boosted significantly by sharp increases in prices for motor vehicles, especially used vehicles. The price index for used cars and trucks leapt 10.5% in June and is up 31.2% over four months (not annualized). Since June 2020, it has risen 45.2%. Increases in prices for used vehicles accounted for approximately 0.4 percentage point of the increase in the core CPI in June and 1.4 percentage points of the latter's 12-month change. Shortages of computer chips have curtailed production of new vehicles, resulting in increased demand and sharply higher prices for used vehicles.

- Recent increases have pushed the core CPI above its pre-pandemic trend: over the 16 months since February 2020, the core CPI has increased at an annualized rate of 3.1%. (Excluding the jump in the CPI for used vehicles, the 16-month annualized change in the core CPI would have been a tame 2.1%.) We expect that annual inflation readings will moderate as base effects recede and supply-chain issues are resolved.

- Rents have firmed in the past couple of months but the trend in

rent inflation remains low. Owner's equivalent rent and rent of

primary residence rose 0.3% and 0.2%, respectively, in June. Their

12-month changes firmed to 2.3% and 1.9%, respectively.

- The cost of clean power generation fell faster than expected in recent years, driven by greater growth in the sector than forecast, and is set to continue to decline at a rapid rate, said BP Chief Economist Spencer Dale. In a letter accompanying the release of the energy company's 70th Statistical Review of World Energy, Dale said the cost of onshore wind and solar power had fallen by around 40% and 55%, respectively, over the past five years, more than double the pace the company expected. Although it is a "gross simplification," he said, cost reductions for renewables are often encapsulated in "learning-by-doing" framework. As increasing amounts of renewable capacity are produced and installed, the members of the supply chain learn how to become more and more efficient, driving costs progressively lower, he added. "Our analysis shows that the biggest factor accounting for the larger-than-expected falls in renewables costs is 'faster learning'—which explains around three-quarters of the error on wind costs and two-thirds for solar costs," he added. With global renewable capacity additions likely to continue apace, a virtuous circle will continue to be fed. The world's installed renewable power generation capacity must jump ten-fold by 2050 if there is to be any chance of limiting global warming to less than 1.5 degrees Celsius compared with pre-industrial levels, the International Renewable Energy Agency said in March. (IHS Markit Climate and Sustainability News' Keiron Greenhalgh)

- Corteva Agriscience is facing a new round of lawsuits brought by California farmworkers who allege their children suffered brain damage and other ill health effects from exposure to the insecticide chlorpyrifos. The four lawsuits, filed this week in California county courts in the Central Valley, contend the pesticide manufacturer - along with farm owners and pesticide applicators - should be held liable. The complaints mirror similar lawsuits filed last fall by the same West Virginia-based law firm on behalf of other California farmworkers. Although a California ban on spraying chlorpyrifos went into effect this year and Corteva stopped manufacturing the insecticide in 2020, attorneys for the farmworkers say the impact of chlorpyrifos use from the mid-1970s through 2017 is still affecting communities across the California counties of Fresno, Kings, Madera and Tulare. The lawsuit claims Corteva, previously Dow AgroSciences, hid the dangers of the insecticide and asks for general and compensatory damages as well as medical costs and punitive damages. (IHS Markit Food and Agricultural Policy's JR Pegg)

- In San Antonio de los Baños, some 30 kilometers south of Havana, dozens of people on 11 July spontaneously protested against power outages and shortages of basic products, and an increase in coronavirus disease 2019 (COVID-19) cases. Protests, which also included calls for political freedom, were replicated in multiple cities nationwide, including Havana. There were at least two confirmed reports of looting against state-owned stores in Artemisa and Matanzas provinces; in the latter, protesters also set a police vehicle on fire. President Miguel Díaz-Canel pointed to the US embargo on Cuba as the cause of the island's economic crisis and urged government supporters to "confront counter-revolutionaries" on the streets. Security forces have been deployed to contain the protesters, particularly in central Havana. The government cut off internet access on 12 July to limit access to information and the protesters' ability to coordinate action. These are the largest protests recorded in Cuba since 1994 and the first directed at President Díaz-Canel. The president has ordered the arrest of the key political activists who are leading some of the demonstrations and is likely to maintain widespread use of intelligence and security forces in the weeks ahead to enable further arrests. He and the ruling Communist Party (Partido Comunista de Cuba: PCC) control all state institutions and enjoy the full support of Cuba's security forces, making government change very unlikely. The likelihood of that scenario will rise if protests increase in size and intensity, and if repression and arrest of protesters lead to a fracture within the PCC and Cuba's security forces, which IHS Markit currently considers unlikely. (IHS Markit Country Risk's Carlos Cardenas and Jose Enrique Sevilla-Macip)

Europe/Middle East/Africa

- Major European equity indices markets closed mixed; UK/France/Germany flat, Italy -0.5%, and Spain -1.4%.

- Most 10yr European govt bonds closed higher except for German bunds closing flat for a second consecutive day; Italy -3bps, Spain/UK -2bps, and France -1bp.

- iTraxx-Europe closed flat/47bps and iTraxx-Xover +3bps/279bps.

- The UK government is set to announce plans to end diesel internal combustion engine (ICE) medium and heavy commercial vehicle (MHCV) sales by 2040 as part of emission reduction plans for the transportation sector to be announced later this week. People briefed on the proposals have told the Financial Times (FT) that this will include a proposal to end the sale of diesel medium commercial vehicles with a gross vehicle weight of under 26 tons by 2035, while sales of trucks over 26 tons will end in 2040. The proposal is also set to lay out plans for road pricing which will be used to help recoup the GBP37 billion in lost revenues from taxes on fuel and vehicle excise duty. Other measures are expected to include a proposal on a consultation related to automakers in the UK producing a minimum proportion of zero emission vehicles (ZEVs) under what has been referred to as a "ZEV mandate". The announcement will also show how decarbonization of the transport sector will help to contribute to the UK reducing CO2 emissions by 78% from 1990 levels by 2035. (IHS Markit AutoIntelligence's Ian Fletcher)

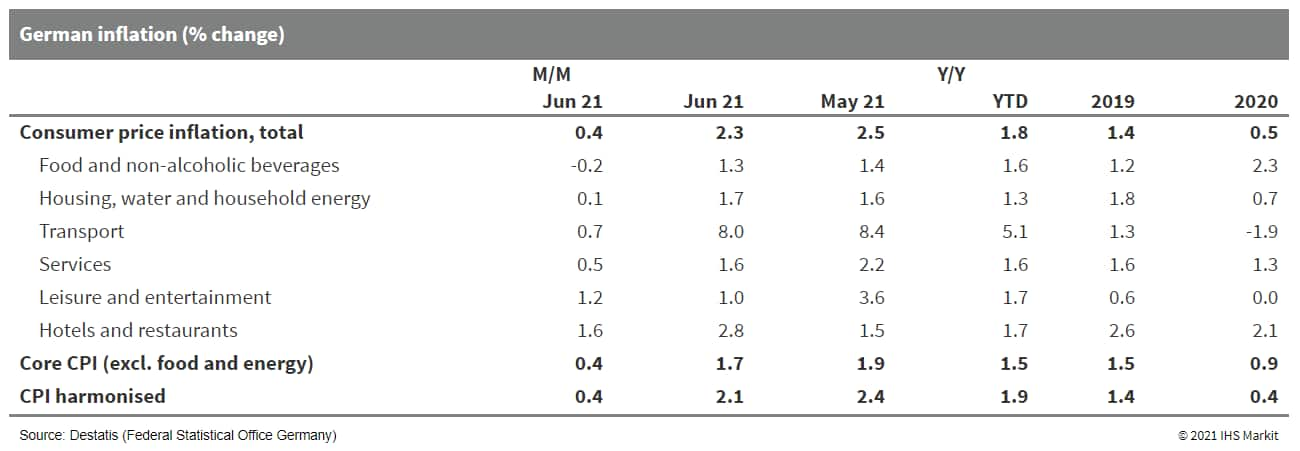

- In Germany, measures of both headline and core inflation

softened in June, owing entirely to base effects. The monthly

change either matched or exceeded its long-term average, pressured

by supply chain disruptions. (IHS Markit Economist Timo

Klein)

- Final June data based on national methodology from the Federal Statistical Office (FSO) have confirmed the "flash" data release of 29 June, posting 0.4% month on month (m/m) and 2.3% year on year (y/y). The latter is a decline from 2.5% in May, but remains well above average inflation of 1.4% in 2019 and 0.5% in 2020.

- The European Union (EU)-harmonized CPI measure also increased by 0.4% m/m in June, allowing its annual rate to correct downwards from 2.4% to 2.1% y/y. Nevertheless, this compares to -0.7% y/y as recently as in December 2020 and continues to exceed the eurozone average (1.9%).

- June's national measure of core CPI (ex-food and energy) has softened too, namely from 1.9% to 1.7% y/y. This remains above the 1.4% average during the first four months of 2021, let alone the December 2020 level of 0.4%. Much of this owes to the January 2021 normalization of the VAT rate following the temporary reduction during the July-December 2020 period, but the loosening of pandemic-related restrictions since May has contributed too. This is linked to companies engaged in recreation and culture activities increasingly returning to business. The - likely short-lived - reduction of the annual rate of core inflation appears to owe largely to a large swing of package tour inflation from May's 7.4% to -5.0% y/y, in turn reflecting the spike in June 2020 when holiday travel returned following the first wave of the pandemic.

- Goods price inflation remained steady at 3.1% whereas its

service-sector counterpart corrected temporarily from 2.2% to 1.6%

y/y due to the package tour effect.

- In France, higher prices of manufactured goods boosted

inflation in June, while services price inflation eased to a

four-month low. (IHS Markit Economist Diego

Iscaro)

- A second estimate shows France's EU-harmonized price rising by 1.9% year on year (y/y) in June. This matches a provisional estimate in late June. June's inflation rate was the highest since December 2018, when it had also stood at 1.9%

- Core inflation, which is not released with the provisional estimate, accelerated from 0.9% in May to 1.1%, the highest reading since July 2020 (when it was boosted by temporary factors related to the timing of the summer sales).

- The acceleration in core inflation was due to the higher prices of manufactured goods. The prices of clothing and footwear, which had fallen by 0.2% y/y in May, rose by 2.9% y/y, while the prices of furniture/furnishing and manufactured goods classified as 'other' rose by 2.7% y/y and 0.6% y/y, respectively.

- On the other hand, services price inflation eased from 1.1% y/y in May to 0.8% y/y. June's increase in services prices was the weakest reading in four months.

- Transport service costs declined by 0.8% y/y (+4.6% y/y in May) as a result of falling airfares (-10.8% y/y, -0.8% y/y in May), more than offsetting a slight acceleration in the prices of 'other' services (+1.1% y/y following +0.9% y/y in May).

- Volvo Cars has announced that it is increasing its stake in Polestar to 49.5%. According to a statement, the acquisition of the additional shares will be from PSD Investment, the private investment company of Eric Li, chairman of both Volvo Cars and its parent Zhejiang Geely Holding Group. Volvo added that it "has no plans to increase its stake further or to consolidate Polestar". However, the completion of the acquisition is said to be subject to certain conditions. Volvo Cars initially held a 50% stake in Polestar until a private placement of newly issued shares to a group of investors, which took place in April. (IHS Markit AutoIntelligence's Ian Fletcher)

- South Africa's real seasonally adjusted manufacturing

production fell by 2.6% m/m during May. The year-on-year (y/y)

growth rate of real seasonally adjusted manufacturing output was

36.9% in May, as production in the base year of comparison was

tempered by COVID-19-related government restrictions imposed during

April-May. (IHS Markit Economist Thea

Fourie)

- Sectors making the largest contributions to the annual growth in manufacturing production during May included motor vehicles, parts and accessories, and other transport equipment (contributing 8.9 percentage points). Other sectors making large contributions to the growth included basic iron and steel, non-ferrous metal products, metal products and machinery (contributing 8.0 percentage points); food and beverages (contributing 7.4 percentage points); and wood and wood products, paper, publishing and printing (contributing 4.0 percentage points).

- The m/m decline in real seasonally adjusted manufacturing production in May was broad based, with the biggest declines recorded in petroleum, chemical products, rubber and plastic products (down 8.9% m/m); electrical machinery (down 12.0% m/m); and motor vehicles, parts and accessories and other transport equipment (down 5.7% m/m). Output in the radio, television and communication apparatus and professional equipment sector showed the strongest monthly growth of 3.9% during May.

Asia-Pacific

- Most major APAC equity markets closed higher except for Australia flat; Hong Kong +1.6%, South Korea +0.8%, India +0.8%, and Mainland China/Japan +0.5%.

- Cathie Wood's Ark Investment Management has been selling Chinese tech stocks, with holdings in one of the firm's funds falling to the lowest on record as Beijing's crackdown on the sector intensifies. China's weighting in Wood's flagship Ark Innovation ETF has plunged to less than 1% from 8% as recently as February, while that of the Ark New Generation Internet ETF has fallen to 5.4%, the lowest compared to month-end figures since Bloomberg began compiling the data in October 2014. The China weighting in Ark's fintech ETF has remained steady at around 18%. (Bloomberg)

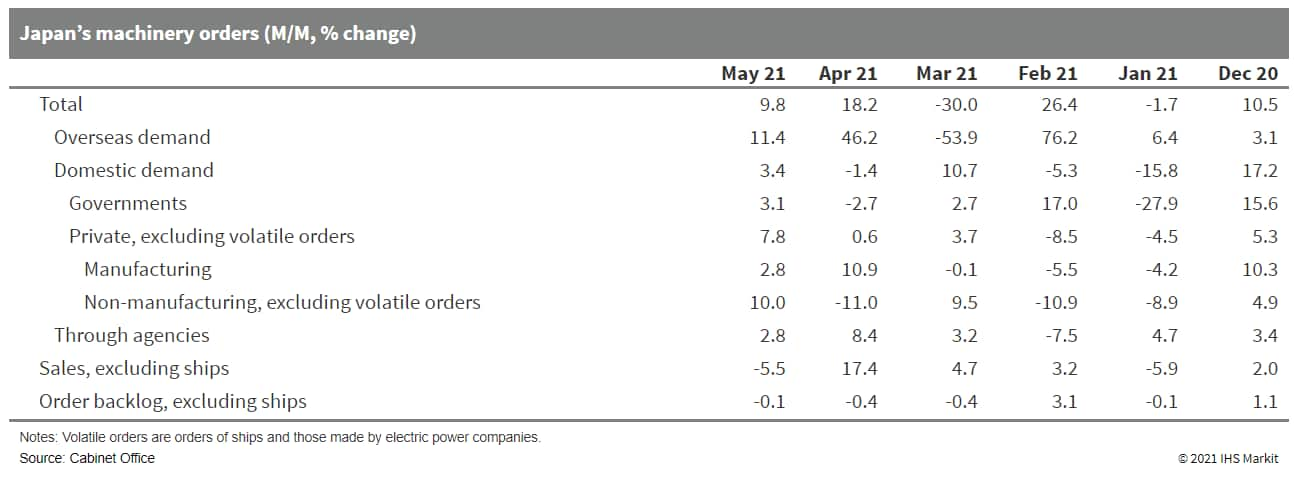

- Japan's private machinery orders (excluding volatiles), a leading indicator for capital expenditure (capex), rose by 7.8% month on month (m/m) in May, the third consecutive month of increase. (IHS Markit Economist Harumi Taguchi)

- The improvement reflected a 10.0% m/m rebound in orders from non-manufacturing (excluding volatiles) and a 2.8% m/m rise in orders from manufacturing.

- Orders from the public sector rose by 3.1% m/m following a 2.7% m/m decrease in the previous month.

- Orders from overseas continued to rise solidly, moving up by 11.4% m/m following a 46.2% m/m increase in April, supported by robust demand for electronics and communication equipment.

- The continued rise in orders from manufacturing largely

reflected increases in orders from electrical machinery,

shipbuilding, and miscellaneous manufacturing groupings, offsetting

declines in orders from non-ferrous metals, general-purpose and

production machinery, and some other groupings. A solid rebound in

orders from non-manufacturing was thanks largely to increases in

orders from telecommunications and the miscellaneous

non-manufacturing grouping.

- HW Electro, a Tokyo-based electric vehicle (EV) startup, plans to launch a multi-purpose small commercial EV called the Elemo, reports Nikkan Jidosha Shimbun. The company plans to commence pre-sale bookings for the Elemo from 24 July in the country, priced in the range of JPY2.18 million (USD19,856) to JPY3.3 million. The model is available in two grades: the Elemo-120 with battery capacity of 13 kWh and a cruising range of 120 km and the Elemo-200 with battery capacity of 26 kWh and a cruising range of 200 km. The official delivery of the model will start from November this year. The upcoming Elemo is aimed at customers moving small goods and carrying out last-mile deliveries in narrow lanes. The model will compete with Mitsubishi Motors's light commercial EV Minicab MiEV in the Japanese market. (IHS Markit AutoIntelligence's Isha Sharma)

- Hyundai Motor will run a pilot service of an autonomous on-demand shuttle for two months in the South Korean city of Sejong, starting 9 August, according to a company statement. The roboshuttle service will operate on the 6.1-km route from Sejong Government Complex to Sejong National Arboretum, with 20 stops. It will be conducted using the Hyundai H350, a light commercial van, equipped with the automaker's autonomous technology and artificial intelligence (AI) technology developed by AIRS Company, a specialized AI research lab under Hyundai. The shuttle, which has received a temporary permit of Level 3 automated operations, can be requested using the Shuckle app, a ride-pooling service developed by AIRS Company. Hyundai has also announced plans to trial the roboshuttle service at its Namyang R&D Center in the second half of this year. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Ola Electric Mobility (Ola Electric) has raised USD100 million in long-term debt for a period of 10 years from the Bank of Baroda, reports The Financial Express. The capital will be used to close the first phase of the development of its electric two-wheeler factory in Tamil Nadu. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Vietnamese automotive startup manufacturer VinFast has announced that it has opened offices in five international markets as of 12 July, including in North America and Europe, reports Reuters. According to the report, a Vingroup statement said, "VinFast has set up representative offices in five international markets and will soon open showrooms in California… VinFast USA's CEO has already relocated to the US from Vietnam recently." The report provides no further details on the locations of these offices and does not name the VinFast USA CEO. As we reported earlier this month, VinFast parent Vingroup is planning to invest USD2 billion to launch electric vehicle (EV) sales in the United States. Reportedly, it is also considering a public listing and raising funds through a special purpose acquisition deal. (IHS Markit AutoIntelligence's Stephanie Brinley)

- The Vietnamese Pepper Association (VPA) has asked the government to analyze freight forwarders' practices in Ho Chi Min City port after prices rose by 10-11 times to $13,500 for 40-foot containers delivered in the EU and by five or six times to $11,000 delivered in the US from July 2020-June 2021. VPA considers that many processors are suffering losses as they are selling under production costs to maintain their market share in the US against Brazil's industry. In addition, most US importers are forcing Vietnam's exporters to work with certified freight forwarders and most of them cannot provide legal services in the US customs. As a result, the association has asked the government to negotiate with sea shipping lines and set transparency rules for freight forwarders. (IHS Markit Food and Agricultural Commodities' Jose Gutierrez)

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-13-july-2021.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-13-july-2021.html&text=Daily+Global+Market+Summary+-+13+July+2021+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-13-july-2021.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - 13 July 2021 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-13-july-2021.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+13+July+2021+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-13-july-2021.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}