Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Oct 19, 2020

Daily Global Market Summary - 19 October 2020

Most APAC equity markets closed higher, while most European and all major US indices ended lower. US government bonds and the dollar were weaker on the day, while European bonds were mixed. iTraxx closed almost flat, but CDX was wider across IG and high yield. Oil closed modestly lower and gold/silver were higher.

Americas

- US equity markets closed lower for the fourth time in five sessions and near the lows of the day; Nasdaq -1.7%, S&P 500 -1.6%, DJIA -1.4%, and Russell 2000 -1.2%.

- 10yr US govt bonds closed +2bps/0.77% yield and 30yr bonds +3bps/1.56% yield.

- CDX-NAIG closed +2bps/59bps and CDX-NAHY +9bps/383bps.

- DXY US dollar index closed -0.3%/93.39.

- Gold closed +0.3%/$1,912 per ounce and silver +1.2%/$24.70 per ounce.

- Crude oil closed -0.1%/$41.06 per barrel.

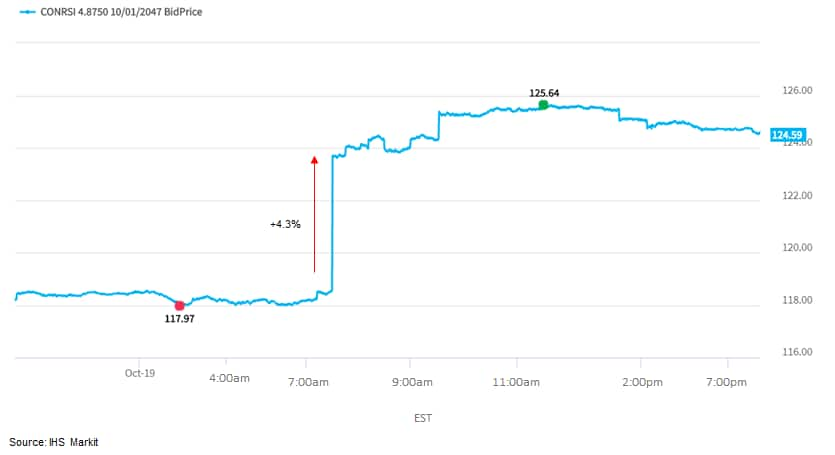

- In a press release, ConocoPhillips announced the signing of an agreement to acquire Concho Resources Inc. in an all-stock transaction valued at $13.3 billion. The transaction is expected to close in the first quarter of 2021. Under the deal, Concho shareholders will receive 1.46 common shares of ConocoPhillips for each Concho share. Based on ConocoPhillips' closing price on 16 October 2020 and 198.5 million Concho shares outstanding (including restricted and performance units), the total equity offer value is $9.79 billion or $49.30 per share. The offer price is a 1.5% premium to the 16 October closing price of Concho. The total transaction value includes the assumption of Concho's 30 June 2020 working capital surplus of $607 million and $4.1 billion of long-term debt and liabilities. On closing, Concho shareholders will own approximately 21% of the combined company. ConocoPhillips and Concho expect the synergies from the merger to result in $500 million in annual cost and capital savings by 2022. The enlarged company is expected to hold 1.5 million net acres (620,000 acres in Bakken, 440,000 acres in Delaware, 260,000 acres in Midland and 200,000 acres in Eagle Ford) in the core area. ConocoPhillips said the acquisition is consistent with its financial and operational framework and meets criteria for merger and acquisitions. Concho's net proved reserves were 1.0 billion boe (62% oil and NGLs; 74% developed) at year-end 2019 and its production averaged 319,833 boe/d (63% oil and NGLs) during the second quarter of 2020. Concho Resources is an independent exploration and production company, focused in the Permian Basin. The company is based in Midland, Texas. (IHS Markit Upstream Companies and Transactions' Karan Bhagani)

- The below is a Price Viewer screen of today's live intraday

bond prices for the Concho Resources 4.875% 10/2047 issue, which

indicates that the issue's price increased 4.3% on the

aforementioned announcement of being acquired by

ConocoPhillips:

- Almost one-fourth of all hospital beds in the El Paso, Texas, area are occupied by virus patients and the region with almost 1 million residents has just 16 intensive-care beds available, state health department data showed. In the state's newest hotspots of El Paso, Lubbock, Amarillo and Laredo, hospitals' virus loads are approaching or already above the 15% threshold set forth by Governor Greg Abbott for emergency status. (Bloomberg)

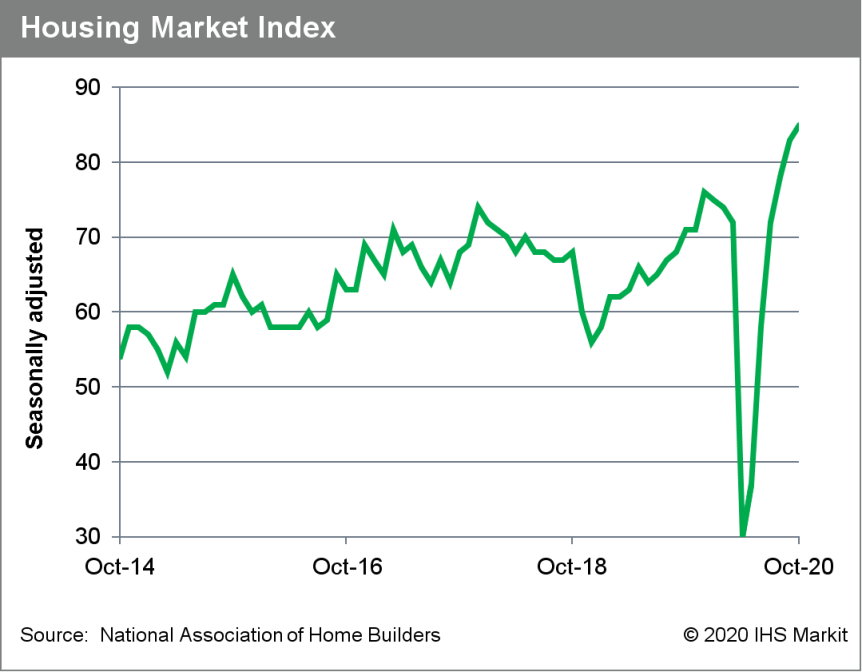

- In April, the US housing market index and its three sub-indexes

plunged to record lows. In October all four indexes set or tied

record highs. (IHS Markit Economist Patrick Newport)

- Part of the story is mortgage rates dropping to all-time lows.

- Another reason is that social distancing is possible in building homes.

- A third driver is bidding wars brought about by record-low interest rates and inventories, and pent-up demand from bidders displaced from the market earlier this year.

- Perhaps pivotal to strength—but hard to measure—is demand from those working remotely because of the pandemic wanting to relocate.

- The headline index increased two points to 85—the highest reading in its 35-year history.

- All three sub-indexes set or tied record highs. The current sales conditions index climbed two points to 90, the index measuring sales prospects over the next six months rose three points to 88, and the traffic of prospective buyers' index was unchanged at 74.

- All four regions set monthly three-month average record

highs.

- International investment business LetterOne has conducted a meta-analysis that demonstrates how pets are significantly contributing to both human health and the global economy. The company determined pet owners are likely to be more active and healthier, meaning pets contribute to reduced healthcare spending in humans. In the US, this equates to a $118 billion reduction. When factoring in this figure, the firm said pets in the country represent a total economic contribution of £222.7 billion. In Germany, the total economic contribution of pets was $49.7bn, followed by the UK at $30.1 billion and Australia at $16.7bn. LetterOne's analysis found pet owners in the US are spending $106 billion a year on their companion animals. Those in Germany spend $25.7 billion, the UK spends $21.1 billion and Australia spends $9.4bn. In the US, $20.3 billion of expenditure is on pet food, $19.5 billion on veterinary services and $18.6 billion on grooming. The majority of expenditure is $47.6 billion on other products, including parasite prevention, pet insurance, toys and accessories. The analysis found in total, 67% of households in the US own a pet. 38% of households in the country own a dog and 25% have a cat. Australia has similar levels of ownership at 61% total, while 40% own dogs and 27% have cats. In contrast, only 45% of German households have pets. Notably, the percentage of cat owning households was higher at 23%, while households with a dog was 19%. LetterOne stated: "Since the global COVID-19 pandemic began, research and data suggests more people are seeking to purchase or to adopt a pet than ever before. (IHS Markit Animal Health's Sian Lazell)

- Karma Automotive is launching its first battery electric vehicle (EV), the GSe-6, in 2021 and has announced a US launch price of USD79,900, prior to potential federal or state incentives. The company is taking reservations for the EV for a fully refundable deposit of USD100. Karma says the GSe-6 will have the body of the Revero GT plug-in hybrid electric vehicle (PHEV), but so far it has provided only a detailed image of the new car. In a statement, Karma's vice-president of global sales and customer experience, Joost de Vries, said, "We are pleased to announce that our first all-electric vehicle is now available for pre-order at a price point that is competitive with other vehicles in the space… the new all-electric GSe-6 was the next logical step in our progression as a company. We like to say we go 'beyond EV' and this vehicle - combined with our existing extended range EV technology in the Revero GT - offers consumers a unique solution for their next vehicle purchase." According to the reservations page on the company's website, the GSe-6 will be offered in several "personas". The standard version of the GSe-6 has the exterior colour New Dawn Silver, specific 21-inch wheels and yellow calipers, and an interior called Palisades. The GSe-6 Luxury has a different exterior color called Sage green, specific 22-inch wheels and burnt orange calipers, and the interior is called Palisades Ceramic. The GSe-6 Sport has the exterior color West Coast yellow, different 22-inch wheels and slate calipers, and an interior called Rebel Ceramic with high-gloss carbon-fiber jewel inlays. All GSe-6 models go "beyond EV", according to Karma, with a fully aluminum body, one-pedal driving, adaptive headlights, haptic steering wheel controls, Level 2 automated driving capability, and surround-view camera. The GSe-6's price is above those of the Tesla Model S, in part as its price was dropped to USD71,990 in October, and the Lucid Air. (IHS Markit AutoIntelligence's Stephanie Brinley)

- Nikola CEO Mark Russell says the company will revert to a base plan, if the proposed GM deal falls apart, during an interview with Automotive News. The report quotes Russell as saying, "We have the ability and we have a base plan of doing it ourselves. If we have a partner, that just enables us to consider going faster and helps reduce the risk. We've proven that over the years that we are a partnership company when those things are available to us." However, Russell also said that Nikola is prepared to drop plans for its Badger pick-up truck if it cannot secure an agreement with an OEM on production; this is in line with plans Nikola indicated when it revealed the truck and indicated it was looking for partner production. In this interview, Russell said, "The Badger is part of our discussions with GM. And we've been clear all along that we wouldn't build a Badger without an OEM partner." Nikola and GM announced plans for a strategic partnership in September, with a 3 December 2020 deadline to conclude the terms. The deal may be at risk in part because deals at the level of talks announced in September do have a chance of failing in any circumstance and because of negative attention on Nikola in the days after the announcement. However, the report does not provide any insight as to whether talks are running into specific issues or going to plan. An investor analysis company accused Nikola of false statements; the fallout from that report led to the departure of Nikola's founder. At this point, there is no clarity on whether the allegations were true, but the situation put Nikola in a negative light and caused some to question GM's due diligence. GM has continued talks, however, and was not included in any of the allegations. (IHS Markit AutoIntelligence's Stephanie Brinley)

- General Motors (GM) has renamed the Detroit-Hamtramck Assembly Center in Michigan, United States, as Factory Zero, reflecting that it is GM's first all-electric vehicle (EV) plant. GM also re-confirmed that the first EVs the plant will produce will be the GMC Hummer electric pick-up and the Cruise Origin shuttle vehicle. The Hummer will be first, in late 2021, and other, unnamed vehicles will follow; a specific production date for the Cruise Origin has not been disclosed. GM invested USD2.2 billion in converting the plant (a figure announced previously), which the company said is its largest single plant investment in the company's history. In a statement, Gerald Johnson, GM executive vice-president of global manufacturing, said, "Factory Zero is the next battleground in the EV race and will be GM's flagship assembly plant in our journey to an all-electric future. The electric trucks and SUVs that will be built here will help transform GM and the automotive industry." The Factory Zero name is intended to be reminiscent of the Factory One site in Flint, Michigan, which was GM's first assembly facility. (IHS Markit AutoIntelligence's Stephanie Brinley)

- Local Motors' parent company LM Industries has raised USD15 million funding from Mirai Creation Fund II, managed by Japanese investment firm SPARX Group. The company will use the capital for product development, production and deployment of Local Motors' Olli, a 3D-printed electric autonomous shuttle, to "transform the future of mobility". Jay Rogers, co-founder and CEO of Local Motors, said, "We share a dream with SPARX Group to completely reimagine the mobility and automotive industry, with the goal to truly move society forward in a profound way. Delivering innovative and locally relevant vehicles and mobility solutions has been at the core of our company from the beginning, and we look forward to pushing the industry to be a more clean, customer-centric business". Local Motors uses multiple micro-factories to design high-technology vehicles and developed the Olli autonomous electric shuttle, which made its debut at the National Harbor in Maryland (US) in 2016. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Spot block cheese settled slightly higher at USD2.7200 per pound, up USD0.0725 from last Friday, and barrels settled at USD2.2050 per pound, up USD0.1500 compared with last week. The spread between the block/barrel market narrowed to USD0.5150 per pound on only six trades total for the week. The barrel market continues to show strength this week and the block cheese market remains tight with prices not far from record highs. A large inverse is starting build up again in the cheese futures market rivalling the one from this summer and 2014, with front month contracts like November diverging sharply higher from January to March 2021 contracts. The strength of demand during October continues to be impressive but a shift lower in demand still lies around the corner. (IHS Markit Food and Agricultural Commodities' Jana Sutenko)

- According to the Central Bank of Paraguay (Banco Central del

Paraguay: BCP), the monthly index of economic activity (MIEA) fell

by a seasonally adjusted rate of 3.6% month on month (m/m) in

August, indicating a slowdown of what had been a strong recovery

from May to July. (IHS Markit Economist Jeremy Smith)

- In addition to falling on a m/m basis, the MIEA experienced a 2.5% year-on-year (y/y) decline. Another high-frequency indicator, the index of business sales, also dropped by 3.5% m/m in August after increases in recent months because of a renewed weakness in retail sales, and hotel and restaurant bookings.

- Contributing to the outcome was an increase in COVID-19 cases that prompted the government to reinstate mobility restrictions in late July, although those measures are now being relaxed.

- The service sector, which accounts for half of the size of the economy, has been the hardest affected overall, contracting by 10.9% y/y in the second quarter. Also struggling is the electricity sector (10.4% decrease y/y in the second quarter) as a result of historically low water levels in the Paraná River, as well as depressed electricity demand in Brazil, the primary recipient of Paraguay's hydropower exports.

- On a positive note, the BCP observed strength in the construction sector, bolstered by an influx of new projects, and agriculture, which is thus far having a better year after prolonged droughts damaged the 2019-20 harvest.

- Despite the decline in August, Paraguay's overall outlook for 2020 is relatively positive when considered from a regional perspective. On a cumulative basis, from January to August, the MIEA was only down by 0.4% y/y and the 6.5% GDP contraction in the second quarter was among the shallowest compared with its peers.

- Fitch Ratings (Fitch) has downgraded Chile's sovereign credit ratings to A- (25) from A (20), still at good quality within the investment grade category. In Fitch's view, higher public spending was driven by large-scale protests that developed in October to November 2019 and the COVID-19-virus pandemic in 2020, paired with cyclical revenue shock. In this context, Fitch expects Chile's fiscal deficit to reach 8.5% of GDP, government debt to rise up to 34% of GDP, and GDP to contract by 5.8% in 2020. Fitch has lifted the outlook to Stable from Negative, supported by a lower debt burden relative to A-range peers and a credible macroeconomic policy. With the downgrade, Fitch assesses a higher risk than IHS Markit, Moody's Investors Service, and S&P Global Ratings, which currently assess a similar medium-term sovereign risk. (IHS Markit Economist Claudia Wehbe)

- Chile's central bank left its monetary policy rate unchanged at

0.5% during its 15 October meeting, maintaining the use of

non-conventional liquidity and credit support. IHS Markit expects

the central bank to keep rates at this technical minimum over the

next two years. (IHS Markit Economist Claudia Wehbe)

- After decelerating since February, annual inflation accelerated in September, reaching 3.1% on the back of a transitory impulse to household consumption of goods driven by an early withdrawal of up to 10% pension savings, as well as supply shortages related to such higher demand.

- A price spike in food and non-alcoholic beverages mainly drove an acceleration in monthly inflation of 0.6%.

- During August, Chile's monthly economic indicator (a proxy for GDP) contracted by 11.3% year on year (y/y), a larger drop in comparison with the August -10.7% result.

- The non-mining and mining sectors fell by -12.2% y/y and -3.4% y/y, respectively. Services - mainly education, transportation, restaurants and hotels, and business services, construction, and manufacturing were the most affected, performing negatively because of mandatory closures or restrictions, while commerce continued to advance.

- The seasonally adjusted broad indicator advanced by 2.8% compared with the July result; non-mining continued to recover but the mining sector fell into negative territory in August.

Europe/Middle East/Africa

- Most European equity markets closed lower except for Spain +0.2%; UK -0.6%, Germany -0.4%, and France/Italy -0.1%.

- 10yr European govt bonds closed mixed; Italy +7bps, Spain +4bps, France +1bp, and UK/Germany -1bp.

- iTraxx-Europe closed flat/54bps and iTraxx-Xover +1bp/328bps.

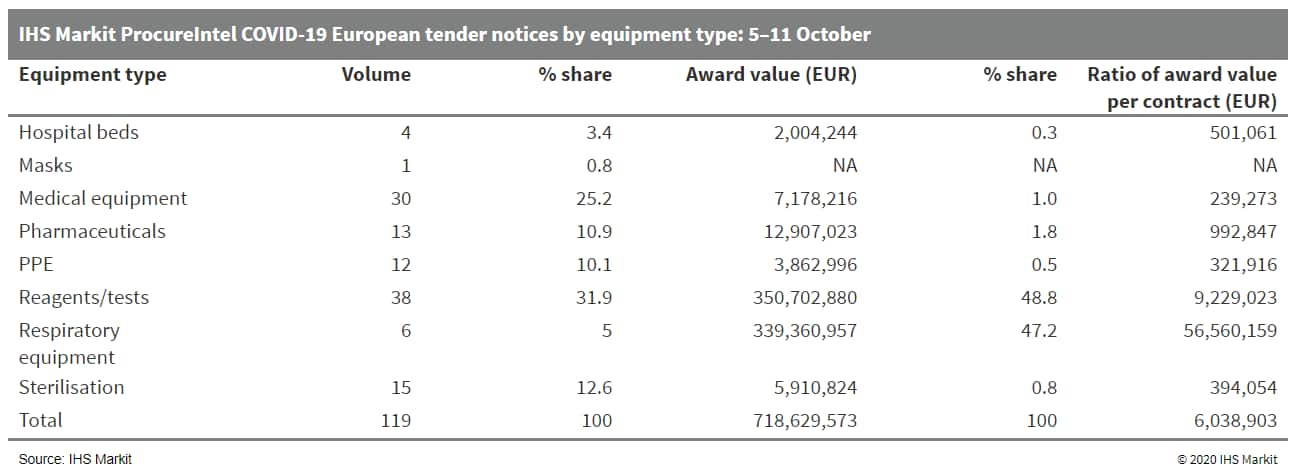

- IHS Markit's weekly ProcureIntel tendering analytics report for

5-11 October identified 119 COVID-19-related European tenders. This

represents a slight increase in volume compared with the previous

highest peak in tender activity - which was registered by IHS

Markit during the last week of September - when the number of

tender awards and award notices reached 110. The estimated value of

the procurement market, including awards and award notices, has

increased to EUR718 million (USD842 million). This is up from

EUR415 million during 28 September-4 October. The seven-day

estimate of the potential award value of European COVID-19-related

tenders brings the weekly average to about EUR372 million to date

in October. IHS Markit ProcureIntel notes that average weekly

procurement amounted to about EUR181 million in September, preceded

by EUR270 million and EUR224 million per week in July and August

respectively. Assuming the trend of strong purchasing demand for

COVID-19-related medical supplies continues in the European tender

market for the remainder of the month, then IHS Markit anticipates

the highest weekly averages since April or May. (IHS Markit Life

Sciences' Choukri Genane and Eóin Ryan)

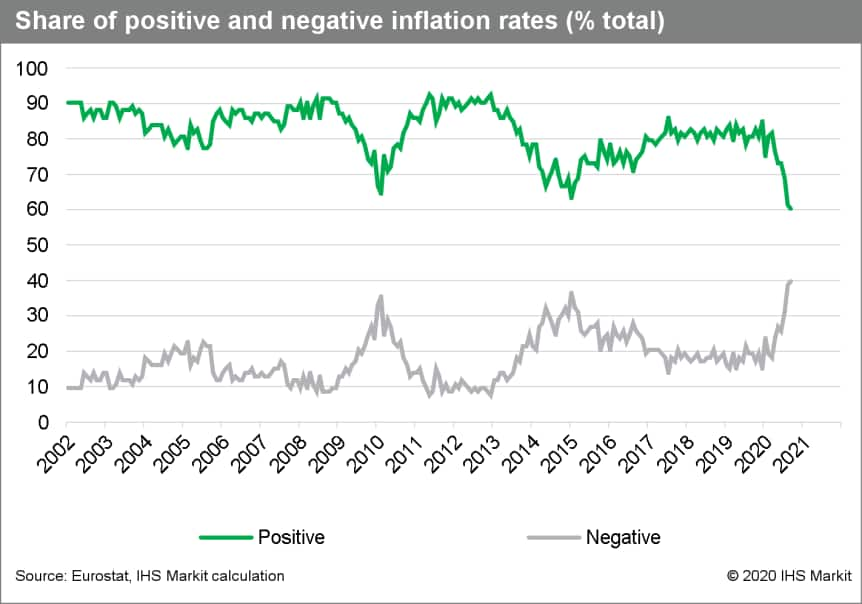

- Eurostat's release of final HICP data for September has

confirmed the downward surprises to both headline and core

inflation rates already signaled in the prior 'flash' release. HICP

inflation edged down from -0.2% to -0.3%, a notch below the initial

market consensus expectation, confirming back-to-back sub-zero

rates for the first time since mid-2016. (IHS Markit Economist Ken

Wattret)

- The unexpected drop in the rate excluding food, energy, alcohol, and tobacco prices from 0.4% to 0.2%, a record low, was also confirmed in the final release (see chart below).

- Driving the core deceleration was a fall in eurozone services inflation (confirmed at a record low of just 0.5%) and continued weakness in non-energy industrial goods inflation (-0.3%).

- The full breakdown of September's HICP data also allows us to update our "super core" measure of inflation. This fell sharply in September, from 1.1% to 0.9%, the first sub-1% reading in the series' history (see chart below).

- As a reminder, the "super core" rate includes only the HICP items sensitive to the eurozone output gap and hence is more reflective of domestic economic developments than the overall inflation rate.

- September's full breakdown also allows us to check on the distribution of positive and negative inflation rates across all HICP items. We keep a close watch on this metric along with our deflation vulnerability index to monitor the risk of deflation in the eurozone.

- The proportion of negative inflation rates has shot up in

recent months, echoing the trends after the global financial crisis

in 2008-09 and the subsequent eurozone crisis in 2011-12, and

reached a record high in September.

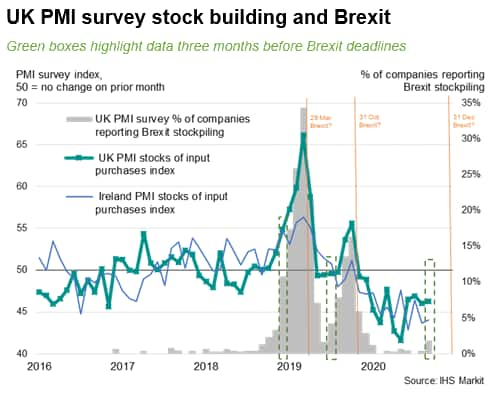

- When the UK first faced the real possibility of leaving the EU,

back in March 2019, the country's manufacturers were building up

their safety stocks. Inventories were being amassed to ensure

continuity of production in case of potential supply shortages,

given that foreign trade flows could dry up without a trade deal in

place. Brexit was eventually postponed. (IHS Markit Economist Chris

Williamson)

- But in 2020, as the UK is once again set to leave the EU at the end of the year, the situation looks a lot different. Three months before the first Brexit deadline in 2019, the IHS Markit/CIPS Purchasing Managers' Index (PMI) survey reported a rise in inventories of raw materials of a magnitude exceeded only once in almost two decades of survey history.

- An analysis of reasons cited for the increase in inventories showed that over one-in-ten producers were specifically building up safety stocks in case of Brexit-related disruptions to supply chains. This would rise to just over one-in-three by March of that year.

- A similar situation was seen in the lead up to the next potential (but also subsequently postponed) Brexit deadline of 31st October 2019, with stockpiling by manufacturers widely reported. This time, the amount of stock building was less - approximately half - than seen ahead of the first Brexit deadline. But it was still one of the largest spells of inventory building seen over the survey's history.

- In contrast, September 2020 has so far found extremely limited evidence of Brexit-related stock building by UK manufacturers. Whereas three months before the March and October 2019 Brexit deadlines, the survey found 11% and 4% of manufacturers having already started to build up Brexit-related stockpiles, so far there have under 2% of companies reporting such stock building.

- The lack of pre-Brexit stock building so far in 2020 can in

part be explained by manufacturers having been disrupted by

COVID-19, which has served as a major distraction among many firms,

including in relation to ongoing difficulties sourcing inputs from

abroad due to non-essential business closures earlier in the year

and transportation issues. It is also possible that Brexit

'fatigue' has set in, especially after costly stockpiling and

warehousing in 2019 ultimately proved unnecessary as Brexit

deadlines came and went.

- BMW UK has signed a second-life battery deal with leading battery-energy storage firm Off Grid Energy. BMW announced the new partnership with Off Grid Energy in the United Kingdom, which will see the automaker use used batteries from its cars to create a network of second-life batteries which can be fed into the power grid. According to the company statement, BMW UK will supply Off Grid Energy with battery modules for it to adapt to create mobile power units. This will give batteries in older BMW and MINI electric vehicles (EVs) a second-life usage when they can no longer efficiently be used in cars. BMW and MINI EV batteries have a warranty of eight years or 100,000 miles. After this period, the battery can still retain up to 80% of its initial capacity. However, it is inevitable that, at some stage, the battery will no longer function at an optimum level for the car - but it can serve a 'secondary use' purpose as a mobile power source. The second-life battery market has a great deal of potential for OEMs to monetize older batteries and potentially help cover the cost of a battery replacement or give the owner access to retained value at the end of a vehicle's life. Second-life batteries also have the potential to give power-generation companies and power grids much greater flexibility in terms of smoothing out periods of high energy demand by releasing energy stored in the second-life batteries. However, for the scheme to work, BMW will presumably have to keep careful track of ownership of its older EVs and maintain a dialogue with the owners of those vehicles. (IHS Markit AutoIntelligence's Ian Fletcher)

- Traton it has reached an agreement in principle to acquire Navistar for USD44.50 per share. The announcement came on 16 October, just under the deadline that Traton gave to Navistar for responding to its offer of USD43 per share. Volkswagen (VW) Group's Traton heavy truck unit revived talks on the full acquisition of Navistar in September 2020, after the postponement of negotiations because of the COVID-19 virus pandemic. Traton already holds a 16.8% share of Navistar and will buy all remaining shares. Matthias Grundler, CEO of Traton SE, said in the statement, "We are pleased to have reached agreement in principle for a transaction after intensive negotiations with Navistar. We are looking forward to completing our due diligence and obtaining the necessary approvals in respect of this exciting deal in order to welcome the new Traton family member." However, the statement also notes that "there is no assurance that the parties will reach agreement on definitive transaction documentation, or as to the terms" of the transaction. According to Traton's statement, next steps include finalizing due diligence to the satisfaction of Traton, agreeing on the conclusion of a merger agreement and related documents. The new agreement must also be approved by the board and executives of Traton, VW, and Navistar. The 16 October announcement keeps the deal alive, after Traton had given Navistar a deadline. In January 2020, Traton first announced an intention fully acquire Navistar, offering USD35 per share. In September, Navistar issued a statement saying its board felt the USD43 per share offer, which was an increase from USD35 per share offered in January 2020, "significantly undervalues the Company and substantial synergies from a combination." (IHS Markit AutoIntelligence's Stephanie Brinley)

- Clariant is relaunching the sale of its pigments business, saying the formal market kick-off was postponed earlier in the year as a result of the COVID-19 pandemic. The company tells CW that since the COVID-19 outbreak, the business has focused successfully on actions to mitigate the pandemic as well as implement an efficiency program to further enhance the intrinsic value of the pigments unit. "Clariant's pigments remains a leading global player in the industry and as such, any convincing offer will have to reflect this leading position," it says. The planned divestment of the pigments business is part of Clariant's transformation program, which will see it concentrate on its faster-growing segments, according to the company. The ongoing program "has so far seen the successful divestment of the healthcare packaging and masterbatches businesses," it says. Clariant is expected to send out information packages to prospective buyers of the unit this month, according to a Reuters report. People familiar with the preparations added that buyout groups including PAI, Lone Star, Triton, and SK Capital are expected to express interest. In April, before the company's decision to delay the divestment process for the pigments business, the unit was expected to fetch up to 900 million Swiss francs ($984 million), or around 8 times core earnings. Clariant's failed merger with Huntsman in the face of activist investor resistance, and a joint venture it abandoned in August with [Sabic] have led to asset sales beyond what the Swiss company originally envisioned, according to Reuters.

- Navya has expanded its partnership with public transport operator Keolis to launch a fully autonomous shuttle service without safety operator on board in Châteauroux, France. Navya has deployed the Autonom Shuttle Evo at the city's National Sport Shooting Centre, allowing athletes and visitors to travel on a 1.5-kilometre route between the car park and the reception area. Etienne Hermite, CEO of Navya, said, "We are taking these steps one at a time, gradually increasing our level of technical expertise to meet increasingly ambitious challenges. Today, fully autonomous operations on closed sites are the first step in the progressive deployment of Level 4 autonomous mobility solutions, so that in the future we will be able to see them driving in more complex environments." This launch is a step towards development of a multimodal service incorporating Level 4 autonomous vehicles. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Denmark-based European Energy has filed for final permission to build its two offshore wind farms Omø South and Jammerland Bay. The announcement comes five months after the Danish Energy Agency approved the company's preliminary environment impact assessments for both projects. European Energy has commenced technical inspections of the seabed at the project locations and has stated that it is confident of the projects' viability. The company revealed that the application process has so far taken eight years and its target is to complete the final design and wind turbine selection by the end of 2021, with installation and grid connection targeted for 2023. Both projects are expected to contribute 560 MW of capacity. (IHS Markit Upstream Costs and Technology's Melvin Leong)

- US-headquartered Mars has localized ice cream production in Russia under a contract at the facilities of the Unilever plant in the Tula region. In Russia, Mars has four factories for the production of chocolate and chewing gum, and five factories for making pet food, but there was no local production of ice cream: the company used to import it from France. Under contract production in Tula, Mars manufactures three types of ice cream: Snickers ice cream bars, and Snickers and Mars in 500 ml buckets. Other well-known ice cream brands, such as Bounty and Twix, the company will continue to import. While the company did not disclose how much ice cream it will be producing in Russia, it only specified that local products will account for about 30% of sales. According to Euromonitor International, Mars in 2019 ranked 15th in ice cream sales in Russia with a share of 1.5%. Unilever remained the top ice cream company in Russia, with a market share of 22%. The demand for ice cream in Russia is growing and imports are unable to satisfy it, a Mars spokesman told Vedomosti. According to Soyuzmoloko, sales of ice cream in Russia in this year's January-May increased 22% to 207,100 tons. Production is also growing: in January-June it increased by 21% to 302,500 tons. Ice cream imports also increased - by 32%% in January-August to 16,300 tons, but the share of imported ice cream in total consumption is small, because it is more expensive than locally-produced ice cream. (IHS Markit Food and Agricultural Commodities' Jana Sutenko)

- Sabic says it is reevaluating and expanding the scope of its planned crude oil-to-chemicals (COTC) project with Saudi Aramco in Saudi Arabia to include the integration of existing facilities. Both companies intend to "study the integration of Saudi Aramco's existing refineries in Yanbu with a world-scale mixed feed steam cracker and downstream olefin derivative units." The decision to expand the scope of the project with Aramco "to include existing development programs of advancing crude to chemicals technologies as well as through integrating existing facilities" comes after taking into consideration the future plans and opportunities of both companies, it says in a statement to the Saudi stock exchange. Sabic says its update statement is in reference to an announcement made by the company in November 2017 when it confirmed the signing of a memorandum of understanding (MOU) with Aramco to study the feasibility of developing a COTC complex. Both companies remain committed to continue advancing COTC technologies through existing development programs, with the goal to increase cost efficiency, competitiveness, and value creation opportunities for petrochemicals, it adds. In November 2017 the companies signed the MOU to develop the world's largest integrated complex to convert crude oil into chemicals at Yanbu on Saudi Arabia's Red Sea coast. The COTC plan envisaged the processing of up to 400,000 barrels/day (b/d) of crude oil to produce approximately 9 million metric tons/year (MMt/y) of chemicals and base oils. It was originally penciled in to start operations by 2025, with capital expenditure estimates of up to $20 billion. Converting crude directly into high-value chemicals instead of transportation fuels is part of Aramco's plan to diversify away from selling oil and maximize its profit per barrel. In March 2018 the companies awarded a contract to Wood Group (Aberdeen, United Kingdom) to carry out project management and front-end engineering and design (FEED) work on the COTC project. Aramco bought a 70% stake in Sabic for $69 billion earlier this year. Both Sabic and Aramco have made substantial cuts in planned capital expenditure this year due to the impact of lower oil prices and COVID-19, which saw Aramco report a sharp plunge in first-half 2020 net profit and Sabic report first- and second-quarter losses.

Asia-Pacific

- Most APAC equity markets closed higher except for Mainland China -0.7%; India/Japan +1.1%, Australia +0.9%, Hong Kong +0.6%, and South Korea +0.2%.

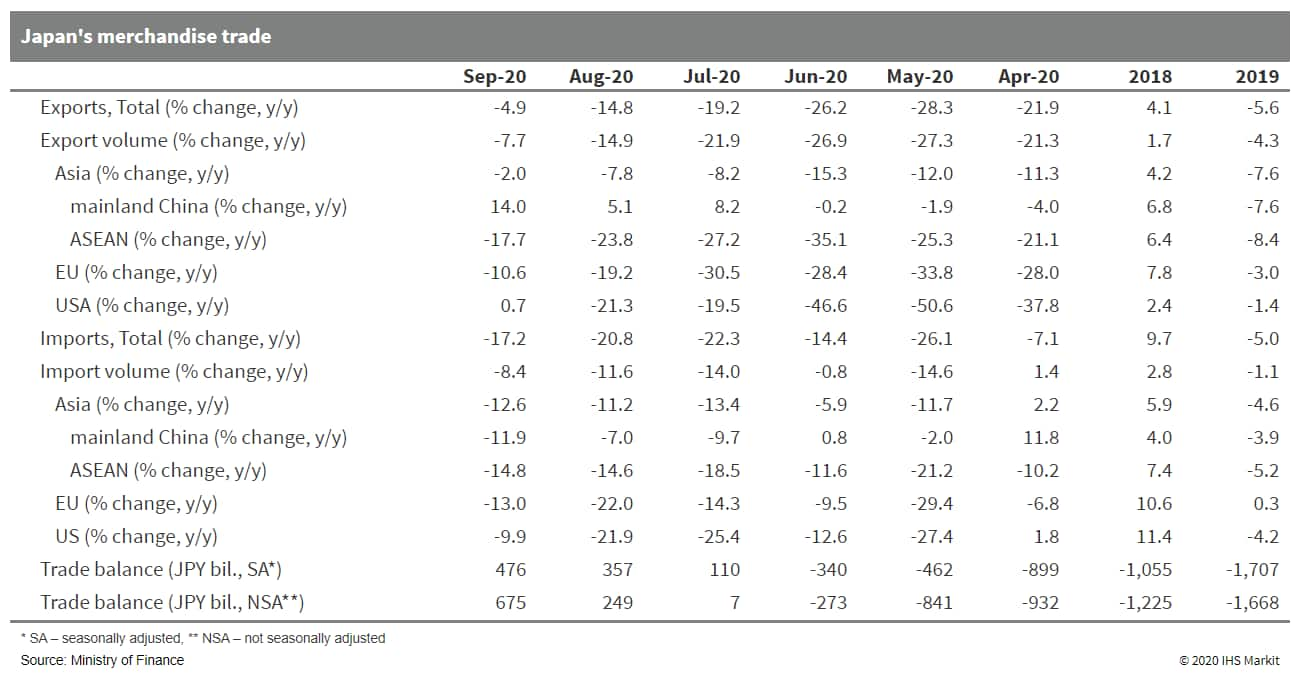

- Japan's trade surplus widened in September, thanks to continued

improvement in exports and sluggish imports. Uncertainties over the

COVID-19 virus pandemic could continue to suppress the recovery of

exports over the near term. (IHS Markit Economist Harumi Taguchi)

- Japan's trade surplus rose by 33.2% month on month (m/m) to JPY476 billion (US4.5 billion) on a seasonally adjusted basis in September and turned to a surplus of JPY675 billion from a deficit of JPY129 billion a year ago.

- The continued increase in the trade surplus was thanks to a softer year-on-year (y/y) decline in exports (down 4.9% y/y) while imports remained sluggish (down 17.2% y/y).

- The improvement in exports reflected increased exports to the US and mainland China. Exports to the US recorded their first rise (up 0.7% y/y) in 14 months, driven by exports of autos, electrical power machinery, and medical products.

- The continued rise in exports to mainland China (up 14.0%) came on in exports of non-ferrous metals, semiconductor machinery, and autos.

- Exports to other regions, including the European Union (down 10.6%y/y) and ASEAN countries (down 17.7% y/y) remained weak.

- Sluggish imports were due largely to lower prices for resources and mineral fuels. Mineral fuels contributed 7.6 percentage points to the contraction for imports. Other major contributors to the decline were imports of mobile phones, clothing accessories, semiconductors, and medical products.

- The September results suggest net exports are likely to be one

of the major drivers for the rebound of real GDP for the third

quarter of 2020. However, the recovery for exports is still lagging

given that export volumes were 7.7% below the year-earlier level

and the seasonally adjusted level (calculated by IHS Markit)

remains below the February level.

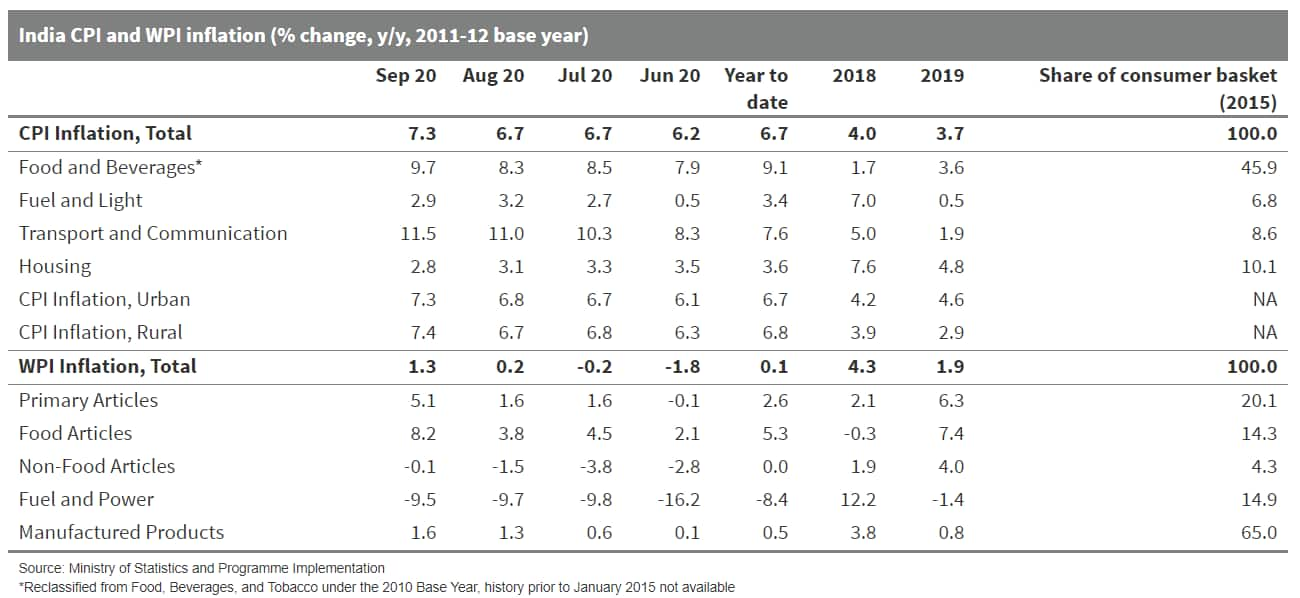

- India's retail inflation reached 7.3% y/y in September, while

industrial output shrank again by 8.0% y/y in August. The Reserve

Bank of India (RBI) will look through the current inflation spike

and support the fragile growth recovery with additional policy

easing following the government's fresh fiscal mini-stimulus. (IHS

Markit Economist Hanna Luchnikava-Schorsch)

- Indian consumer price index (CPI) inflation jumped to 7.34% y/y in September - its highest in eight months - up from 6.69% y/y in August, according to data released by the Ministry of Statistics and Program Implementation (MOSPI).

- Sharply rising food prices were again the culprit of high headline inflation, with the food and beverages component of CPI reported at 9.73% y/y against 8.29% y/y in August, led by higher prices of vegetables, pulses and meat.

- Inflation in transport and communication category also accelerated sharply to 11.5% y/y in September from 11.0% y/y in August, reflecting a recent rise in taxes on petroleum products.

- Wholesale price index (WPI) inflation also accelerated to 1.3% y/y in September from August's 0.2%, when it turned positive following four months of deflation. Within the WPI basket, prices of manufactured products rose by 1.6% y/y.

- In a separate data release by the MOSPI, the index of

industrial production contracted by 8.0% y/y in August, narrowing

the pace of decline from July's 10.8% y/y, as factories continued

to reopen following the government's gradual easing of lockdown

restrictions.

- All three major industry groups including mining, manufacturing and power, registered contraction in output in both annual and monthly terms.

- On a use-based approach, most notable was the annual drop in consumer non-durable goods production in August (it fell by 3.3% y/y) after two months of expansion, pointing to the waning effect of pent-up demand immediately after the strict national lockdown was lifted. Sustained weakness in domestic demand was also evident from a continued steep contraction in output of capital and investment goods, as well as consumer durables.

- The September uptick in inflation is somewhat sharper than expected and well above the central bank's target range of 2-6%, but it is unlikely to change the Reserve Bank of India's accommodative monetary policy course, at least not yet. In its October policy meeting, the RBI stated it would look through the current uptick in inflation, which it views as transient amid the supply chain disruptions related to the COVID-19 virus pandemic and recent increases in petrol taxes and transportation costs.

- Along with other real sector activity indicators, the improving

but still very weak industrial output data point at a very fragile

state of domestic demand and a further need for fiscal and monetary

support, particularly as the virus continues to spread rapidly

through India.

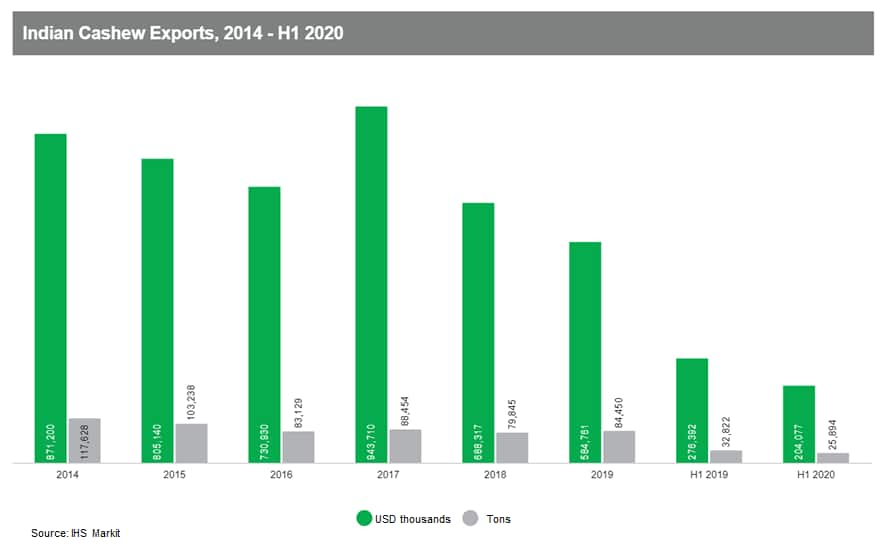

- Indian cashew exports fell by 29% year-on-year in volume to

34,700 tons and by 28.5% in value to US273.0 million in

January-August 2020. The main importers were the UAE and the

Netherlands, both global re-exporters, taking 20.0% and 17.0% of

the total exported volume, respectively. Imports fell by 9% y-o-y

to 592,890 tons in January-August 2020, after halving to 87,000

tons in August 2020 compared with the same month last year. Indian

processors lifted purchases for West African raw cashew nut

origins, after Tanzania took three-quarters of the total in Q1.

Benin, Ghana and Ivory Coast (West Africa) accounted for 21.4%,

16.0% and 9%, respectively, of the total volume. (IHS Markit Food

and Agricultural Commodities' Jose Gutierrez)

- China reported that its economy grew by 4.9% in the three months ended Sept. 30 from a year earlier, accelerating from the second quarter's 3.2%. Accompanied by separate data on Monday showing better-than-expected growth in retail sales, hiring and industrial production, that bolsters China's case for being the only major world economy likely to expand this year. (WSJ)

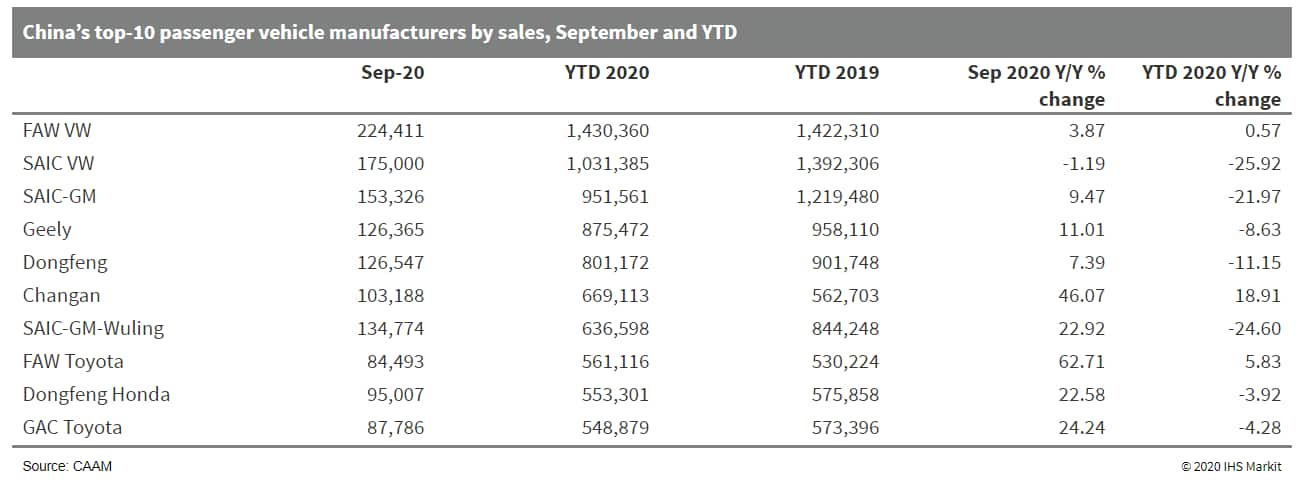

- The auto market of mainland China continued to gain traction in

September, the sixth consecutive month of growth since a rebound

began in April. According to data from the CAAM, China's new

vehicle sales, on a wholesale basis, increased 12.8% year on year

(y/y) to 2.57 million units in China during the month, while

production rose by 14.1% y/y to 2.52 million units. (IHS Markit

AutoIntelligence's Abby Chun Tu)

- In the year to date (YTD) for September, China's new vehicle sales were down 6.9% y/y at 17.12 million units, and production volumes contracted 6.7% y/y to 16.96 million units. In September, passenger vehicle (PV) sales increased 8.0% y/y to 2.09 million units, while PV production grew by 9.5% y/y to 2.05 million units.

- In the YTD, sales of PVs decreased 12.4% y/y to 13.38 million units, while production of PVs fell by 12.4% y/y to 13.22 million units.

- Sales volumes of new energy vehicles (NEVs) climbed to their highest monthly level of the year in September, driven by favorable policies and incentives. Sales of NEVs, which include battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and fuel-cell vehicles (FCVs), increased 67.7% y/y to 138,000 units in September, while NEV production rose by 48.0% y/y to 136,000 units.

- Sales of BEVs grew by 71.5% y/y to 112,000 units in September, while production of BEVs increased 40.0% y/y to 107,000 units.

- In September, sales of PHEVs were 26,000 units, up 53.9% y/y, while production of PHEVs increased 89.5% y/y to 29,000 units. In the YTD, sales of NEVs were reported at 734,000 units, down 17.7% y/y, while NEV production volumes were down by 18.7% y/y to 738,000 units.

- Electric PVs remain the highest-selling category of NEVs in the Chinese market. In September, sales of electric PVs were 100,000 units, up 70.2% y/y, while sales of electric commercial vehicles totaled 12,000 units, up 82.7% y/y.

- The strong performance of the Chinese auto market in September

is further evidence of the continuing recovery of consumer demand

amid an improved economic outlook.

- Chinese car-sharing platform GoFun has raised over CNY100 million (USD15 million) in a Series B funding round, reports Gasgoo. The latest funding round is financed mainly by large national investment funds and Chinese local industry guidance funds. The company will use the infused capital to upgrade vehicle resources, software, hardware, offline operations, and standardized services. According to the report, GoFun is also in talks with domestic investment banks to go public. GoFun was launched in 2016 to offer rental new energy vehicles (NEVs) on an hourly basis. The GoFun platform, which is backed by Shouqi Group, a Chinese state-owned transportation company, completed its Series A financing in 2017. The platform is available in more than 80 cities across China. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Tesla has cut the prices of its Model 3 in Australia. According to online news portal Drive, the base Standard Range Plus model is now priced at from AUD66,900 (USD47,300) before on-road costs, so is cheaper by AUD7,000, and it has a range of 490 kilometers (km), up 30 km from previous versions. The mid-specification Long Range variant now costs AUD83,425 before on-road costs, a price cut of AUD6,000, and its range has increased to 657 km from 620 km previously. The top-of the range version now costs AUD92,425, which is AUD5,000 less than the earlier price, and its range has increased by 68 km to 628 km. Although the prices have decreased, the level of equipment on offer as standard has been either upgraded or revised. The Model 3 now features the Model Y's heat-pump HVAC system, a redesigned center console with wireless charging pads for two smartphones, an updated storage compartment with a sliding lid, and two more USB-C ports for high-powered device charging. Tesla recently reduced the pricing of the Model 3 in China. The reduction in price can be attributed to the use of lithium iron phosphate (LFP) batteries. Compared with the lithium-ion (Li-ion) batteries equipped in Tesla's models, LFP batteries are less expensive as they do not contain cobalt - one of the most expensive materials in Li-ion batteries. (IHS Markit AutoIntelligence's Nitin Budhiraja)

- The South Korean government has eased regulations to expedite the recycling of discarded electric vehicle (EV) batteries, reports AJU Business Daily. Currently, all EV owners who received government subsidies upon their purchase must return car batteries to local governments when their cars are scrapped. However, there are no guidelines on how to use discarded batteries that still have up to 80% capacity. The South Korean Ministry of Trade, Industry, and Energy said in a statement on 19 October that nine companies, including Hyundai Glovis, LG Chem, Hyundai Motor, and GoodByeCar, will start a recycling business using discarded EV batteries. "Discarded EV batteries could bring negative effect to the environment but new business models could be created when they are reused," said the ministry, adding that the companies involved would share data after a two-year test period. The project using discarded EV batteries is designed to check the potential of future green energy businesses. The ministry said energy storage systems (ESSs) can be deployed in urban areas to provide fast charging for EVs. (IHS Markit AutoIntelligence's Jamal Amir)

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-19-october-2020.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-19-october-2020.html&text=Daily+Global+Market+Summary+-+19+October+2020+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-19-october-2020.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - 19 October 2020 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-19-october-2020.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+19+October+2020+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-19-october-2020.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}