Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Jan 25, 2021

Daily Global Market Summary - 25 January 2021

Most APAC equity markets closed higher, the US was mixed, and all major European indices closed lower. US and benchmark European government bonds closed sharply higher. European iTraxx closed wider across IG and high yield, while CDX-NA was almost flat on the day. Oil closed higher, copper flat, and gold/silver were lower. COVID-19 hospitalizations continue to decline in the US, which has led California to lift regional stay-at-home orders today and other states like New York are also easing certain restrictions.

Americas

- US equity indices closed mixed; Nasdaq +0.7%, S&P 500 +0.4%, DJIA -0.1%, and Russell 2000 -0.3%, with the NASDAQ and S&P 500 reaching new record high closes. The S&P 500 declined 1.5% between 10:48-11:10am EST, before turning course and ending the day at the new record high close.

- 10yr US govt bonds closed -6bps/1.03% yield and 30yr bonds -5bps/1.80% yield.

- CDX-NAIG closed +1bp/52bps and CDX-NAHY +2bps/307bps.

- DXY US dollar index closed +0.2%/90.39.

- Gold closed -0.1%/$1,855 per ounce, silver -0.3%/$25.48 per ounce, and copper flat/$3.63 per pound.

- Crude oil closed +1.0%/$52.77 per barrel.

- COVID-19 hospitalizations in the U.S. fell to their lowest level since mid-December, while newly reported infections continued to decline, falling below 200,000 for the eighth consecutive day. California, a hotspot in the fall surge, ended regional stay-at-home orders as intensive-care capacity improved. (WSJ)

- Moderna plans to begin human studies of a booster shot for its vaccine to help protect against a more-transmissible South Africa virus variant, after a test showed it may be less potent against that strain. Even with the lower antibody levels, the existing vaccine should offer protect against the South Africa strain, Moderna said. But study results may indicate that immunity will wane faster, the company said. (Bloomberg)

- Ford is idling its Louisville Assembly plant in the United States for two weeks from today (25 January) over a semiconductor shortage. This is the second time this month that Ford has introduced downtime at the plant over the issue. The automaker produces the Ford Escape and the Lincoln Corsair at the plant, which was idled for a week over parts issues earlier this month. Automotive News reports that a Ford spokesperson confirmed the introduction of the downtime at the plant, as well as that hourly workers will receive 75% of their gross pay during the downtime. At the time of the shutdown earlier this month, Ford indicated that it would bring forward a previously planned week of downtime at the plant, but that is not part of the latest downtime. When the supply of semiconductor chips resumes at the plant, it should be early enough in the year for Ford to recover the lost production. Of the situation overall, IHS Markit executive director Mark Fulthorpe said that, as of 22 January, "The situation remains highly fluid and we continue to track the impact of these developments. Currently, there are varying estimates as to the length of the semiconductor shortage, with some suggestions that the situation will improve from the second quarter onwards, while some of the lower level disruption could even be recovered within the current quarter. Overall, the global volume at risk has risen to 628,000 units with this update, up from 498,000 units previously. At this level we still expect the majority of volume can be recovered across the balance of the year, so we think of the impact of the current shortages to be more of a seasonal, with volume lost in the first quarter, displaced to later in the year. We expect this rather than an absolute reduction to the 2021 calendar year forecast." (IHS Markit AutoIntelligence's Stephanie Brinley)

- EPA last week launched a regulatory process to develop national drinking water standards for two per- and polyfluoroakyl substances (PFAS), handing a surprising win to environmentalists and public health advocates who have long clamored for stricter oversight of the "forever chemicals." In an announcement made in the final hours of the Trump presidency, EPA issued the final regulatory determinations for PFOA and PFOS, triggering the start of a rulemaking to set standards for the two chemicals under the Safe Drinking Water Act (SDWA). The agency will now begin work on a maximum contaminant level (MCL) for PFOA and PFOS and has also proposed requiring public water utilities to test for the presence of 29 other PFAS chemicals. In addition, EPA issued an advanced notice of proposed rulemaking (ANPR) to get data and public comments on whether it should take any additional steps to address PFAS contamination in the environment. Now-former EPA Administrator Andrew Wheeler said the sweeping proposal reflects the Trump administration's effort under its PFAS Action Plan to address the public health concerns from the widely-used industrial chemicals. There are some 5,000 PFAS chemicals, widely considered a potential public health risk because of studies linking exposure to a range of serious health problems, including cancer, thyroid disease, and autoimmune disorders. The chemicals - used in an array of industrial applications including non-stick cookware and food packaging - are virtually indestructible, sparking concern amid evidence of widespread groundwater contamination, largely from manufacturing plants and from use in firefighting foams on military bases across the country. Tests by EPA and state agencies have found the chemicals in drinking water supplies for 16 million Americans in 33 states and the extent of the pollution is likely far greater. (IHS Markit Food and Agricultural Policy's JR Pegg)

- Baker Hughes has announced an order with Petrobras to provide

digital solutions across Petrobras sites in Brazil. (IHS Markit

Upstream Costs and Technology's Helge Qvam)

- Baker Hughes will support Petrobras' thermal plants, refineries, gas treatment units, production plants, offshore platforms, FPSOs, all ensuring the latest regulatory requirements are achieved.

- The order includes flare monitoring and calibration

technologies, cybersecurity and remote monitoring services, and

interconnected machinery protection systems and sensors. Baker

Hughes use real-time analytics to help improve machinery health,

eliminate unplanned outages, reduce downtime, and avoid

catastrophic failures. The scope with Petrobras includes:

- Bently Nevada's Orbit 60 system, System 1 software licenses, and remote monitoring services for industrial asset management.

- Panametrics' Flare IQ flare gas monitoring and optimization system, and FlareCare services and parts for reduced carbon and methane emissions.

- Nexus Controls' distributed control systems, cybersecurity services and human-machine interface upgrades for more reliable operations.

- Nicaragua's monthly index of economic activity (IMAE) in

November contracted by 4.7% month over month (m/m) primarily

because of the devastation caused by Hurricanes Eta and Iota. (IHS

Markit Economist Lindsay Jagla)

- This is the first monthly contraction since the height of the COVID-19-virus pandemic in March and April, when economic activity contracted by 4.8% and 7.2% m/m, respectively.

- The driver of this contraction was fishing and aquafarming at -43.7% m/m, which was directly hit by the hurricanes. Other sectors, such as the mining and hospitality industries, including hotels and restaurants, continue to suffer from low export demand and the lack of tourism amid the global pandemic.

- Nicaragua is one of few countries to not implement strict lockdown procedures during the initial outbreak of the pandemic. This did not prevent economic activity from contracting significantly, and it has remained below 2019 levels for a prolonged period.

- The global pandemic has lowered demand for Nicaraguan exports, while the spread of domestic COVID-19 cases has damaged consumer activity even without official isolation measures.

- Still, the lack of government-mandated isolation measures allowed Nicaragua's economic activity to return to pre-COVID-19 levels in October - earlier than most countries. Hurricanes Eta and Iota reversed much of this recovery in November, bringing economic activity down to its lowest level since June.

- IHS Markit expects economic activity in Nicaragua to rebound following the external shocks of the hurricanes, but overall economic recovery will remain muted in 2021 at 1.7% year on year (y/y). The country is coming off of its third consecutive year of economic contraction, and lack of significant government stimulus coupled with the continued risks from COVID-19 virus will result in a more prolonged damage to the economy.

- France's President Emmanuel Macron stated on 13 January that

the country should reduce its dependency on imports of Brazilian

soy to avoid contributing to further deforestation of the Amazon.

Brazilian President Jair Bolsonaro and Brazilian Vice-President

Hamilton Mourão have responded, denying that soy production

contributes to Amazon deforestation. (IHS Markit Country Risk's

Ailsa Bryce and Bibianna Norek)

- Soy is primarily produced in the Cerrado area rather than in the Amazon region. Data from ABIOVE, the Brazilian Association of Vegetable Oil Industries, show that roughly 50% of Brazilian of the 2018/2019 soy crop was cultivated in the Cerrado region, the single largest soy producing area, and that in this region, 93% of the growth in soy crops took place on land cleared before 2013.

- Despite Brazil's continued participation in the Paris Climate Agreement and formally rigorous environmental laws, President Bolsonaro's actions demonstrate ideological opposition to environmental controls. Brazilian law states that, in the Amazon region, agricultural producers must preserve 80% of all native forest on their land, using only 20% of land for cultivation. However, Bolsonaro pledged in 2019 to open the Amazon to agribusiness and mining, while Environment Minister Ricardo Salles has sought to deregulate environmental practices, claiming that this will reduce poverty in the region. As a result, enforcement of existing regulations had been weak, giving scope for soy grown by unregistered growers operating in the Amazon and contributing to deforestation to enter agribusiness supply chains.

- President Macron's comments or a decision by France to boycott Brazilian soy products are unlikely to cause a significant drop in Brazil's exports. The EU receives under 10% of Brazil total soy exports, with 73% going to China. The EU, including France, primarily imports soymeal for animal feed, with the EU accounting for 49.5% of Brazil's soymeal exports.

- Macron's remarks on deforestation risks in the Amazon align with his administration's focus on ecological transition, compounding existing pressure against the EU-Mercosur deal.

- Even without a drive for official EU regulation, companies face growing pressure from NGOs, consumers and ESG-oriented shareholders to demonstrate deforestation-free supply chains for agricultural products, with increased focus on environmental sustainability threatening Brazilian exports. High-profile comments such as those by Macron are likely to encourage shareholder activism, particularly by French ESG funds (such as Amundi and AXA, already high-profile exponents of shareholder activism), increasing pressure on major food companies to prove that supply chains are ESG-compliant, even without regulatory changes.

Europe/Middle East/Africa

- European equity markets closed lower; Germany/Spain -1.7%, France/Italy -1.6%, and UK -0.8%.

- 10yr European govt bonds closed higher; Italy -6bps, Spain/UK -5bps, and France/Germany -4bps.

- iTraxx-Europe closed +2bps/51bps and iTraxx-Xover +10bps/264bps.

- Brent crude closed +0.5%/$55.68 per barrel.

- The UK's Office for National Statistics (ONS) has reported that

UK public-sector net borrowing (excluding public-sector banks; PSNB

ex) stood at GBP270.8 billion in the first nine months

(April-December) of the current fiscal year (FY). This was up from

GBP58.1 billion a year earlier and was the highest borrowing in any

April-December period since the records began in 1993. (IHS Markit

Economist Raj Badiani)

- Central government net cash requirements (excluding UK Asset Resolution Limited and Network Rail) were GBP333.6 billion in April-December 2020, up from GBP30.6 billion in the equivalent period a year earlier.

- Central government finances are displaying considerable stress from the COVID-19 virus crisis. Substantial fiscal costs are resulting from the public health measures and policies deployed to support businesses and households. The Office for Budget Responsibility (OBR) estimates that the cost of COVID-19 virus support measures to assist public services, households, and businesses now stands at GBP280 billion this year.

- The ONS also reported that general government borrowing (PSNB excluding public-sector banks) stood at GBP34.1 billion in December 2020, GBP28.2 billion higher than a year earlier. This was the both the highest December borrowing and the third-highest borrowing in any month since the monthly records began in 1993.

- Central government receipts collected by HM Revenue & Customs fell for the 11th straight month and at a brisker pace in December 2020. They declined by 2.8% year on year (y/y) to GBP60.2 billion because of lower-than-normal economic activity, job losses, and companies deferring tax payments.

- Central government expenditure increased by 43.5% y/y to GBP26.1 billion in December 2020. This partly reflects the still rising cost of the Coronavirus Job Retention Scheme (CJRS) and Self-Employment Income Support Scheme (SEISS).

- The furlough schemes (the CJRS and SEISS) added GBP66.1 billion to borrowing in April-December 2020. In December, the total cost of the CJRS and SEISS was GBP9.3 billion.

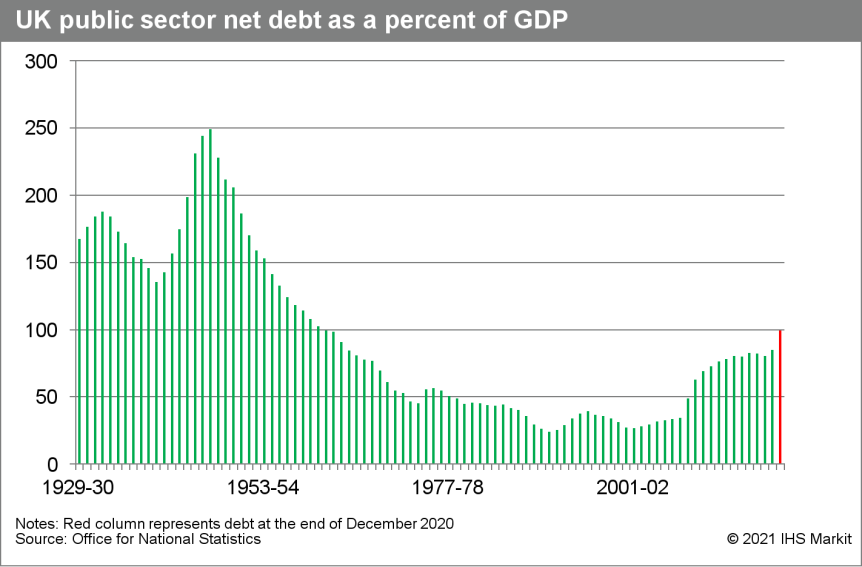

- The UK's net debt position increased by 15.3 percentage points over the year, standing at 99.4% of GDP in December 2020 (see chart below), the highest level since 1962. In monetary terms, it was at a record high of GBP2.312 trillion, GBP333.5 billion more than in October 2019.

- According to IHS Markit's January forecast, general government borrowing requirements in the current FY (April 2020 to March 2021) are likely to be around GBP400 billion or 19% of GDP. Meanwhile, the fiscal watchdog, the OBR, suggests that borrowing in the FY could be GBP394 billion.

- The balance of risks is probably tilting to the downside. The

pace of government borrowing could accelerate in the next few

months because of rising COVID-19 infections, the imposition of

tighter restrictions on the hospitality and retail sectors, and the

prospect of renewed GDP losses in late 2020 and early 2021. Indeed,

the government has pledged extra money to provide support for

hospitality businesses forced to close across the UK, giving them

new scope to furlough workers until the end of April 2021.

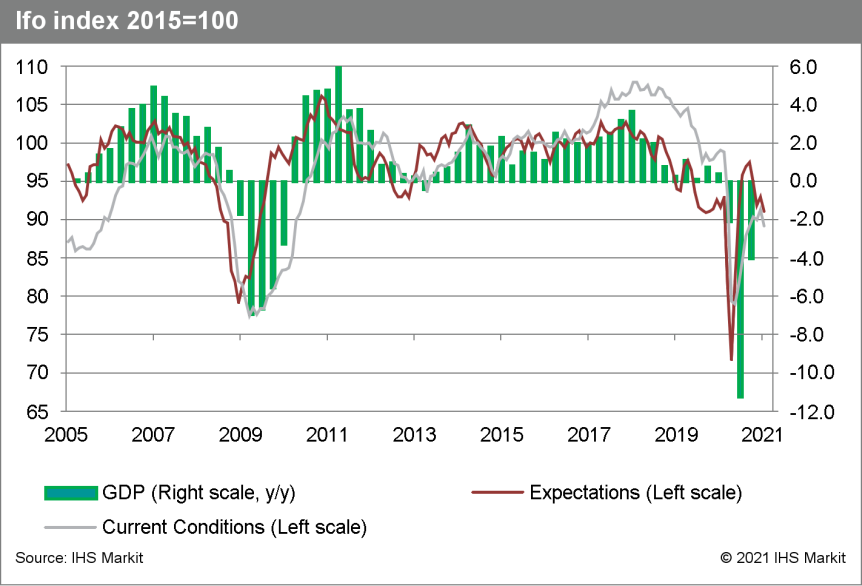

- In January, Germany's headline Ifo index, which reflects

business confidence in industry, services, trade, and construction

combined, has resumed the downward correction observed since

October 2020 after only a short-lived rebound in December. It

declined from 92.2 in December (revised up from 92.1) to 90.1 in

January, thus remaining well below the February 2020 pre-pandemic

level of 95.8 and its long-term average of 97.0. Although the

latest level is still far above the all-time low of 75.5 in April

2020, the Ifo institute confirms what we had expected: "The second

wave of coronavirus has brought the recovery of the German economy

to a halt for now." (IHS Markit Economist Timo Klein)

- There was no material difference between the respective developments of current conditions and expectations in January. Business expectations deteriorated from 93.0 (revised up from 92.8) to 91.1, while current conditions declined from 91.3 to 89.2. Expectations worsened across the board, led by retail trade, whereas current conditions in the manufacturing sector improved against the general trend. The latter underlines that this sector is the least vulnerable to the strict lockdown measures that were imposed in mid-December and that have been tightened during January - manufacturing exports to Asia (and especially China) are still booming. In contrast, the forced closure of non-essential shops and services have hit retail and (to a lesser extent) service-sector optimism hard - they had come too late to much affect the December numbers already.

- January's breakdown of overall indices by sector, which combines expectations and current conditions, shows that business confidence remained roughly stable in the manufacturing sector, as worsened expectations and improved current conditions offset each other. At the opposite end, retailer confidence plummeted, led by current conditions, and the business climate among wholesalers, service-sector providers, and construction firms all posted moderate declines. In level terms, the manufacturing climate now markedly outperforms that in all other sectors, contrasting with underperformance between early 2018 and mid-2020, and it also is the only one with a positive balance between optimists and pessimists.

- The Ifo graph portraying the cyclical position of the diffusion index of the headline measure - setting the current conditions and expectations balances against each other - signals that the economy has reversed course. Although it had still been in downswing territory in December, it was directionally pointing towards boom territory - now it has moved back towards the recession field, although the improvement in the current conditions component in manufacturing has prevented it from entering recession ground already. The assessment of current conditions fell back from 8.2 to 3.2, while expectations moved more deeply into the red (from -5.1 to -9.0). This reflects the recent extension and in part even tightening of COVID-19 related restrictions until mid-February.

- January Ifo survey results have demonstrated that the December

rebound was misleading, as most survey responses had been handed in

before the strict lockdown implemented in mid-December had become a

reality. Nevertheless, it is noteworthy that business expectations

(defined as "for the next six months") did not show a larger

decline than current conditions in January. This indicates that

most businesses still see the light at the end of the tunnel but

have had to scale back their optimism in view of ongoing

uncertainty about how long the phase of tight restrictions will

need to last.

- The Volkswagen (VW) Group is looking to claim damages against

some of its suppliers which have caused temporary production

stoppages due to a shortage of semiconductors, reports Reuters,

citing an article in Automobilwoche. (IHS Markit AutoIntelligence's

Ian Fletcher)

- The German trade publication has been told by sources that this type of action is being considered against Bosch and Continental so that they can share the burden of costs related to alternative sourcing of these components, which is expected to be more expensive. A Bosch company source added to Automobilwoche that the supplier was ready to discuss the matter directly with its customers and suppliers in due course. A VW Group spokesperson declined to comment on the matter to Reuters, and the suppliers did not respond to requests for comment.

- In an attempt to ease the supply shortage of semiconductors to the automotive industry, the German government has sought to use diplomatic channels. According to a letter seen by Reuters, Germany's Minister for Economic Affairs and Energy, Peter Altmaier, has written to Wang Mei-hua, Taiwan's Minister for Economic Affairs, to address the issue in talks with Taiwan Semiconductor Manufacturing Co Ltd (TSMC). He said, "I would be pleased if you could take on this matter and underline the importance of additional semiconductor capacities for the German automotive industry to TSMC," adding that the aim was to have additional capacity and deliveries in the short-to-medium term.

- Production disruptions related to the shortage in semiconductors for the automotive sector began to emerge late in 2020, but have accelerated significantly during the first quarter of 2021. The shortage is linked to stronger-than-expected demand in the second half of 2020 in the wake of COVID-19 virus-related production stoppages and demand disruption.

- The problem is also exacerbated by strong demand experienced by consumer electronics firms.

- Although a wide array of global OEMs have been hit to varying degrees, VW Group seems to be one of the worst affected. IHS Markit intelligence suggests that eight of its plants in Europe will be hit at some point during the first quarter, alongside both its key Chinese joint ventures (JVs), FAW-VW and SAIC-VW will be hit by stoppage and reductions of output.

- Germany's Federal Motor Transport Authority (Kraftfahrt-Bundesamt: KBA) is said to be looking into the safety issues related to the touchscreen used on certain Tesla models, reports Reuters. A spokesperson for the KBA was quoted as telling the Bild am Sonntag newspaper that it was in contact with the US National Highway Traffic Safety Administration (NHTSA) and Tesla, asking for more information. The representative added that the KBA was also launching its own investigation, and that the results are "still pending". The investigation in Germany is related to a request by the NHTSA for Tesla to recall about 158,000 units of model year (MY) 2012-18 Model S and the MY 2016-18 Model X to address touchscreen failures related to an NVIDIA processor. Specific issues that have been raised by the NHTSA include the fact that the failure results in the loss of the rear view/reversing camera as well as heating, ventilating, and air conditioning (HVAC) controls, including defogging and defrosting setting controls. The agency also states that the failure has an adverse impact on the Autopilot system, turn signal functionality (the loss of audible chimes), and alerts associated with these functions. It is unclear whether any of these issues have emerged with German owners or whether it has been alerted by the NHTSA recall, but it remains to be seen whether it plans to implement a similar recall. (IHS Markit AutoIntelligence's Ian Fletcher)

- According to a Bloomberg report, energy company Petronas (Kuala Lumpur, Malaysia) is a possible contender to acquire Lonza's specialty ingredients division. Petronas is working with an adviser as it considers a second-round bid for the Lonza Specialty Ingredients (LSI) division, which is up for sale, says the report. Lonza has asked interested parties to submit second-round bids by early February, the report says. Petronas Chemicals Group (PCG), the chemicals subsidiary of Petronas and one of the largest producers of petrochemicals in Southeast Asia, tells CW that it "regularly evaluates potential business opportunities, however, as a matter of practice we do not comment on speculation." Lonza told CW recently that it is in discussions with potential buyers for the LSI business, but does not "comment on speculation," and that "as soon as we have more information, we will share it with the markets." Lonza earlier declined to comment on reports that Lanxess and private equity groups including Advent International, Carlyle Group, Partners Group, and a consortium comprising Bain Capital and Cinven had been shortlisted for the second round of bidding for LSI. The Bloomberg report says that the LSI division could fetch about 3.5 billion Swiss francs ($3.9 billion). Sazali Hamzah, managing director and CEO of PCG, told CW in December that the company continues to focus on its growth ambitions and is extending further in the downstream value chain by venturing into derivatives and specialty chemicals to cement its position as a regional leader in the chemicals market. PCG in September 2019 acquired specialties company Da Vinci (Amsterdam, Netherlands). (IHS Markit Chemical Advisory)

- Swiss start-up Mirai Foods has raised USD2.4 million in seed funding to prepare the commercialization of cultivated meat. High-profile backers include Finnish food company Paulig Group and technology investment company Team Europe. Mirai is the only cultivated meat player in Switzerland and claims to be one of the few globally that do not genetically manipulate their cells but keeps the cells as they naturally occur in the animal. "Our mission is to accelerate the world's transition to producing food that is environmentally, ethically and economically sustainable," says Christoph Mayr, Mirai co-founder and CEO. "And we want to do it as cleanly and naturally as possible since this is important to many consumers and regulators, particularly in Europe." Mirai says the benefits of cultivated meat also include controlling the composition of fatty acids and fat levels as well as the elimination of the use of antibiotics. Paulig has a tradition of focusing on plant-based food but Marika King, head of the group's venture arm PINC, says innovative technologies open up new avenues. "It is not a question of plant versus animal. At Paulig, we see it is a new choice for consumers, let's make sure that they get it," he notes. Mirai is based in Zürich, Switzerland, and focuses primarily on Wagyu beef. The company is now accelerating product development of their slaughter-free meat and is working on transforming their prototype into a commercial product. (IHS Markit Food and Agricultural Commodities' Max Green)

- The Ukrainian government has signed eight production-sharing agreements (PSAs) since the beginning of the year, signaling a renewed determination to kick-start upstream investment and boost the country's flagging oil and gas production. The PSAs, comprising blocks in several regions across the country (see table below), are valid for 50 years, with a 5-year exploratory stage requiring license holders to drill at least two wells and invest at least UAH450 million (USD16.1 million). Ukraine initiated the PSA tender process in mid-2019, but the process of negotiating terms and finalizing contracts with PSA winners was delayed as a result of Ukraine's July 2019 parliamentary elections that ushered in a new government. Separately, state-owned Naftogaz Ukrainy has acquired full control of Nadra Yuzivska, the license holder for the Yuzivska block in eastern Ukraine, the country's largest shale gas project. Shell had won the rights to the Yuzivska contract and signed a PSA with the government in 2013, but the company subsequently withdrew from the project after the eruption of armed conflict between pro-Russian separatists and the Ukrainian military in the area. Ukraine has made start-stop progress over the past few years in its effort to boost domestic production and reduce its reliance on oil and gas imports. Energy self-sufficiency has become an overt policy goal, with the decision to halt gas imports from Russia in 2015 following Russia's annexation of Crimea and its support of a separatist rebellion in eastern Ukraine the year before, but Ukraine's efforts continue to flounder. The government launched an aggressive push to auction licenses and offer blocks under PSA terms in 2019 during the presidential and parliamentary elections; predictably, the political uncertainty of the time undercut investor interest, with several blocks failing to receive bids and a cancellation of the results of the Dolphin PSA tender following the installation of the new government. Against the backdrop of the global economic downturn from the COVID-19-virus pandemic, Ukraine struggled to elicit interest in a number of onshore blocks that were offered to investors in 2020; meanwhile, domestic gas production fell by 2.3% year on year to 20.2 billion cubic meters (Bcm). (IHS Markit E&P Terms and Above-Ground Risk's Andrew Neff)

- The China International Development Cooperation Agency and the

Export-Import Bank of China on 20 January offered Kenya debt

service suspension amounting to USD245 million for the first half

of 2021. This follows the Paris Club of creditor nations on 11

January granting Kenya official debt service relief under the G20's

Debt Service Suspension Initiative (DSSI), with Kenyan authorities

stating they would seek to extend such relief to all bilateral

lenders. (IHS Markit Country Risk's William Farmer, Thea Fourie,

and Eva Renon)

- The COVID-19 pandemic has severely disrupted economic activity in Kenya, worsening fiscal and external liquidity constraints. For example, Kenya's tourism ministry announced on 2 December 2020 that fewer than 500,000 international tourists visited the country between January to October 2020, versus 1.7 million international travelers visiting during the same period in the previous year. The government also has lost tax revenue by reducing PAYE and value-added tax rates in early 2020 to help the population cope with COVID-19-pandemic-related disruption and provided employment programs for unemployed youths. As a result, IHS Markit assesses that Kenya's fiscal deficit is expected to widen to an estimated 7.5% of GDP in 2021, from 6.4% of GDP in 2019.

- The government has failed to disburse money to county governments for November, December, and January, exacerbating ongoing public-sector strikes and causing project delays. Clinical officers and nurses in county-funded public health departments across Kenya have staged strikes since 8 December 2020 over inadequate supply of personal protective equipment (PPE) and compensation payment arrears.

- Granting Kenya payment relief worth USD630 million up to June, the DSSI, and wider bilateral debt relief should facilitate renewed funding to county governments. Savings made under the DSSI are tracked and must be used to fund countries' COVID-19 responses; payment of arrears to striking frontline healthcare workers, therefore, is likely. The modest debt relief granted will not ease Kenya's rising debt servicing obligations, with projected debt service in 2021 at 68.3% of total foreign reserves. However, Kenya's DSSI membership did not negatively affected its credit rating or market standing ahead of a successful issuance of a record volume of infrastructure bonds worth USD1.14 billion (KES125.3 billion) on 19 January.

- In response to budgetary shortfalls, the Kenyan government is likely to rationalize expenditure on loss-making parastatal agencies. Reportedly, the government has agreed to cut parastatal spending to facilitate access to an USD2.3-billion extended fund facility from the IMF. However, in line with IMF recommendations, major fiscal changes are unlikely at least until July 2021, when the new financial year begins, with the Fund recognising that controlling and coping with the impacts of the COVID-19 pandemic are a more-urgent priority than improving longer-term fiscal sustainability.

- Real seasonally adjusted retail trade sales in South Africa

contracted by 4.0% year on year (y/y) during November 2020, from a

2.3% y/y fall in the previous month. This brought real seasonally

adjusted retail sales down by 7.7% during the first 11 months of

2020. (IHS Markit Economist Thea Fourie)

- Retail categories that showed the largest contribution to the 4.0% y/y decline during November included 'other' retailers (-3.2 percentage points); textiles, clothing, footwear and leather goods (-1.1 percentage point); and general dealers (-1.1 percentage point).

- Only the household furniture, appliances and equipment and the hardware, paint and glass retail categories made positive contributions to the annual growth, contributing 0.4 and 1.1 percentage point respectively during November.

- The weak retail numbers recorded in the South African market during November was not a surprise. Disappointing 'Black Friday' sales during November - despite more days allowed for special offers by most retailers compared to previous years - bode negative for the overall retail numbers. Retail sales of home improvement products such as hardware, paint, and glass continue to perform well as the culture of 'working-from-home' becomes more entrenched amid the ongoing COVID-19 pandemic. Furthermore, an increase in housing sales during the second half of 2020 supported retail categories such as household furniture, appliances, and equipment.

- Latest statistics released in the South African Reserve Bank (SARB)'s quarterly bulletin show that real durable spending during the third quarter of 2020 recovered to pre-COVID-19-pandemic levels after harsh COVID-19 lockdown measures were lifted in June. The downturn in real spending on non-durable goods has been less severe compared to the significant drop in semi-durable goods and services spending over the period, which will take at least until 2022, or even later, to reach pre-pandemic levels.

- Currently, IHS Markit expects only a moderate increase in GDP quarter-on-quarter (q/q) growth of 0.5% in the fourth quarter of 2020. This will follow the 13.5% q/q rebound in growth during the third quarter of last year. Overall real GDP is expected to have contracted by 7.3% in South Africa in 2020.

Asia-Pacific

- Most APAC equity markets closed higher except for India -1.1%; Hong Kong +2.4%, South Korea +2.2%, Japan +0.7%, Mainland China +0.5%, and Australia +0.4%.

- Foreign direct investment (FDI) flows into China rose by 4%

year on year (y/y) to USD163 billion, making China the world's

largest recipient of global investment in 2020, according to a

report released on 24 January by the United Nations Conference on

Trade and Development (UNCTAD). Meanwhile, the global FDI plunged

by 42% y/y with the decline in developed countries reaching 69%

y/y. (IHS Markit Economist Yating Xu)

- According to China's Ministry of Commerce (MOF), FDI flows into the non-financial sector expanded by 4.5% y/y to reach USD144.4 billion in 2020, the fastest rate achieved in five years and marking the fourth consecutive year of increase. Services continued to drive the headline FDI inflow, with FDI into the sector growing 12.9% y/y, accounting for 77.7% of total FDI. FDI into the high-tech manufacturing sector increased 11.4% y/y, with high-tech services FDI rising 28.5% y/y. Total FDI growth for December 2020 stood at 8.4% y/y, the fastest rate registered in the second half of 2020.

- By investor, FDI from the Netherlands and England rose 47.6% and 30.7%, respectively. By regional recipient, China's eastern regions, particularly Jiangsu, Guangdong, Shanghai, Shandong, and Zhejiang, received nearly 90% of total FDI.

- A fast return to positive GDP growth and sustained recovery, in addition to the government's foreign investment facilitation program, will continue to underpin mainland China's FDI inflows in 2021. China reported real GDP growth of 2.3% for full-year 2020 and is expected to be the only major economy to have realized economic growth; this resulted in China becoming a safe haven for multinational investment during the COVID-19 pandemic-ravaged year.

- Meanwhile, global dependence on the supply chains of multinational enterprises in China will continue to support the economy's FDI and export growth while the pandemic still rages on.

- The disruptions caused by the pandemic have temporarily reversed the two-year trend of declining FDI inflows in China. However, whether the current growth trend will last depends on the scope of China's service sector liberalization and developments in China-US relations.

- Uisee, a Chinese autonomous vehicle (AV) firm announced that it had raised over CNY1 billion (USD154 million) in a new funding round, reports Pandaily. The latest funding round included National Manufacturing Transformation and Upgrade Fund, a CNY50.1-billion state-owned fund to promote the China's manufacturing industry. According to the source, the company has also recorded growth during the COVID-19 virus pandemic due to its collaborations with Changan Minsheng Logistics, FAW Logistics, BASF and Dongfeng Motor. Uisee was founded in 2016, and is engaged in the creation of mobility and logistic solutions with AI driving. The company was founded by Gansha Wu and Yan Jiang, and has its headquarters in Beijing. Robert Bosch Venture Capital is one of the lead investors of Uisee, along with Shenzhen government-backed Shenzhen Capital Group and state-backed CCI Investment. Uisee has bypassed advanced driver-assistance systems (ADAS) and focuses on autonomous operation. Uisee has supplied its technology to scenarios including airports, parks, buses, and robo-taxis over the past years, and Hong Kong International Airport is using Uisee's solutions to automate its baggage tractors. In September 2020, Uisee partnered with SAIC-GM-Wuling to build the first unmanned logistics route in China. In January 2021, AV startup WeRide also completed a Series-B funding round of USD310 million. (IHS Markit Automotive Mobility's Automotive Mobility)

- Chinese EV startup XPeng has said its P7 electric sedan is to feature a Surrounding Reality (SR) display, which will work together with its Navigation Guided Pilot (NGP) function, an automated highway-driving feature, to give the driver an intuitive automated driving experience. NIO has said that it is to introduce a new software update in the ES8, ES6, and EC6 models to add new features or improve existing features such as automated functions. Xpeng and NIO have rolled out automated driving systems for highway autopilot functions to compete with Tesla in the field of automated driving. Tesla has been a dominate player in the EV market in terms of sales volumes; however, the high purchase price of its Full Self-Driving (FSD) automated driving system has hindered the adoption of the technology among mass-market consumers. (IHS Markit AutoIntelligence's Abby Chun Tu)

- Reliance Industries says that EBDITA dropped 28% year-on-year

(YOY) at its oil-to-chemicals (O2C) business, to 97.56 billion

Indian rupees ($1.34 billion) in the fiscal third quarter ended 31

December. Quarterly sales for the sector were Rs838.3 billion, down

29.6% YOY. (IHS Markit Chemical Advisory)

- The O2C business includes refining, petrochemicals, fuel retailing through the Reliance BP Mobility business, aviation fuel, and bulk wholesale marketing.

- However, Reliance's O2C business achieved sequential improvement with fiscal-third-quarter revenue up 10% quarter-on-quarter (QOQ) primarily on higher volumes of transportation fuels, purified terephthalic acid (PTA), and polyester supported by improved product realization across polymers, intermediates, and polyester. "We have delivered strong operational results during the quarter with a robust revival in the O2C segment," says Mukesh Ambani, chairman and managing director at Reliance.

- Segment EBITDA in the third quarter improved by 10.3% sequentially due to higher product sales and shifting of product placement from exports to the domestic market. Throughput grew from 16.8 million metric tons (MMt) to 18.2 MMt on a QOQ basis owing to improved demand.

- In the polymers business, prices of polypropylene (PP), polyethylene (PE), and polyvinyl chloride (PVC) strengthened during the quarter by 18%, 8%, and 29% QOQ, respectively, amid a strong demand recovery in Asian markets. The company says that margins of PP and PE over naphtha increased by 31% ($698/metric ton) and 13% ($541/metric ton), respectively, and PVC margins over naphtha and ethylene dichloride rose 15% ($628/metric ton) on a QOQ basis led by strong demand recovery across sectors. PVC prices were at a decade-high level during the quarter, Reliance says.

- In the intermediates and polyesters business, prices of para-xylene (p-xylene), PTA, and ethylene glycol (EG) strengthened during the quarter by 3%, 15%, and 8% QOQ, respectively, amid a hike in energy values and improved downstream demand. P-xylene, PTA, and EG margins increased by 4% ($141/metric ton), 57% ($168/metric ton), and 17% ($218/metric ton), respectively, amid lower inventory across the polyester chain in China. Reliance says it achieved higher capacity utilization rates on the back of festive demand and the availability of labor in the downstream sector. Polyester margins improved QOQ through differentiated and specialty products.

- Reliance's average steam cracker operating rate was 96%, despite a scheduled shutdown at the company's refinery off-gas cracker at Jamnagar, India.

- The company's other business units include oil and gas, retail, digital services, and financial services.

- VinFast revealed several new products recently, including plans for two to go on sale in the US and Canada as soon as June 2022. VinFast announced three new utility vehicles on 22 January, with two of them also planned for US and Canadian sales. The VF32, a D-segment entry, and the VF33, an E-segment entry, are planned to be offered in the US and Canada, while the smaller VF31 is not. The VF32 and VF33 will offer electric and gasoline (petrol) engine options, depending on market. The VF32 is 4,750 mm long, with a 2,950-mm wheelbase while the VF33 is 5,120 mm long and has a 3,150-mm wheelbase. The top-specification versions of all three vehicles will also include a high level of driver assist, including "Level 3 autonomous features," according to the VinFast statement. The vehicles will have intelligent driver assist, adaptive lane control, active cruise control, multi-point collision warning systems, collision mitigation, intelligent automatic parking and a driver monitoring system. High-specification versions will have LiDAR sensors, 14 cameras capable of detecting objects up to 687 meters away, and 19 360-degree sensors for warnings at high speeds. VinFast's autonomous system will use the Orin-X chip and the company says it can process up to 200 gigabytes of data per second. Depending on market, VinFast intends to offer automatic parking and vehicle summoning. The interiors will use virtual cockpit technology and leverage artificial intelligence technology, machine and deep learning, facial recognition and a multilingual virtual assistant, and over-the-air updates are also a part of the equation. The VF31 will have a 10.28-inch center screen, while the two larger utilities will have 15.4-inch screens. VinFast aims to have all three models capable of achieving top 5-star ratings from global safety agencies, including the US National Highway Traffic Safety Administration (NHTSA) and Euro New Car Assessment Program (NCAP). The VF32 and VF33 are planned to go on sale in the US, Canada and Europe from November 2021, with deliveries in June 2022. (IHS Markit AutoIntelligence's Stephanie Brinley)

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-25-january-2021.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-25-january-2021.html&text=Daily+Global+Market+Summary+-+25+January+2021+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-25-january-2021.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - 25 January 2021 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-25-january-2021.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+25+January+2021+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-25-january-2021.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}