Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

EQUITIES COMMENTARY

Feb 20, 2020

European equity shorts

Brief: Drivers behind popular short positions

- Premier Oil short relates to debt refinancing dispute

- Wirecard largest EU short (€3.4bn on loan)

- Cineworld shorts as part of global theater theme

- Declining borrow demand for Aston Martin shares

Overall the short loan value, that is the amount of securities finance transactions deemed likely to be related to short selling, has increased by just over 4% YTD. That suggests little overall change in positioning, with the short positions little change shares terms so that the increase in balances matches the advance for broad EU market indices. Beneath the surface of relatively steady aggregate short demand there have been some movers which warrant a closer look. We'll examine a few such names here as well as some of the most popular shorts overall.

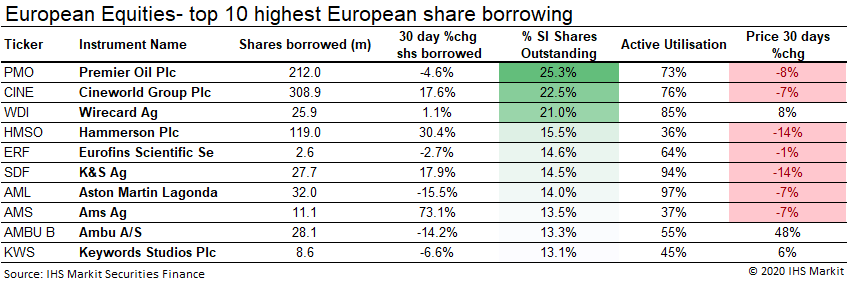

The Premier Oil share price surged following the early January announcement of a debt refinancing plan. The increase in share price was met with an increase in share borrowing, making PMO shares the most heavily borrowed in Europe as a percentage of outstanding shares. The largest publicly disclosed short position is from Asia Research & Capital Management Ltd. (ARCM), who revealed a position of more than 140m shares in July 2019 (there are a total of 217m shares on loan). ARCM is also Premier Oil's largest creditor and released a statement on February 12th indicating that they will "vigorously oppose" the firm's proposed restructuring plan in court on March 17th.

Shares of Cineworld have seen a 23% increase in borrow demand YTD, largely maintaining a consistent borrow value of ~£530m despite a 20% decline in the share price. Short sellers may be betting against the prospects for the firm, specifically the debt assumption required to facilitate the proposed takeover of Cineplex (an all-cash deal expected to close in the first half of 2020) and other challenges faced by global theatre brands. The latter concern is also reflected in the increased short demand for AMC shares and the February 18th bankruptcy filing for VIP Cinema Holdings (maker of luxury cinema chairs).

Hammerson Plc has also seen increased borrow demand, likely driven by a perceived likelihood that the UK REIT will cut its dividend. IHS Markit Dividend Forecasting predicts the August 2020 dividend will be cut 23% YoY. Hammerson currently has 15.5% of outstanding shares borrowed, worth £268m.

Borrow demand for Future Plc surged following the January 31st release of a research report from Shadowfall Capital & Research, which was linked in a tweet that disclosed its short position. The number of borrowed shares has more than doubled after the report was released to 7m shares for settlement on Feb 18th. The borrow cost remains low with more than 15m shares reported as available for borrow.

Borrow demand for shares of Wirecard has been flat over the last month, however that follows demand surges in October and December. Shares of WDI are the most heavily borrowed for any EU equity in nominal terms, with over €3.4bn on loan. The massive borrow balance is the result of the share price increasing just over 30% from the December low, while shares on loan have increased by just over 20%.

Moving in the opposite direction, the number of Aston Martin shares on loan decreased 22% from the post-IPO peak observed on January 24th. The move toward the exit appears to be motivated by the January 31st announcement of strategic equity investment in the firm by a consortium led by billionaire Lawrence Stroll, which provided a boost to the share price.

Another UK equity with declining borrow demand is NMC Health Plc. The UAE healthcare group has come under increased scrutiny following a Muddy Waters research report in December, which revealed that the firm held a short position. While the share price has declined by 67% since the report was released, the trajectory hasn't been on a straight line with four days seeing a greater than 10% increase in price, two of which were increases of more than 30%. The volatility may be shaking some short sellers out of the trade, reflected in a 50% decline in share borrowing YTD. The decline in borrowing is also notable in that the 52% decline in share price YTD may have been softened by the impact of short covering.

To wrap up we'll head back to the continent to look at shares of AMS Ag, which have seen a net increase in share borrowing YTD, based on coronavirus related concerns for the Apple supplier and questions surrounding the acquisition of Osram Licht Ag. The number of borrowed AMS shares has more than doubled YTD, 10.8m shares, however that figure also represents a decline from the peak borrow demand of 14.4m shares on February 4th. The share price has oscillated, but is little changed, with a net increase of 1.1% YTD.

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2feuropean-equity-shorts.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2feuropean-equity-shorts.html&text=European+equity+shorts+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2feuropean-equity-shorts.html","enabled":true},{"name":"email","url":"?subject=European equity shorts | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2feuropean-equity-shorts.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=European+equity+shorts+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2feuropean-equity-shorts.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}