Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Jul 24, 2024

Flash PMI shows UK businesses gaining confidence as selling prices rise at slowest rate for 3½ years

The flash PMI survey data for July signal an encouraging start to the second half of the year, with output, order books and employment all growing at faster rates amid rebounding business confidence, while the rate of output price inflation moderated.

The first post-election business survey paints a welcoming picture for the new government, with companies operating across manufacturing and services having gained optimism about the future, reporting a renewed surge in demand and taking on staff in greater numbers. Prices charged have meanwhile risen at their lowest rate for nearly three and a half years, further raising the prospect of a summer rate cut.

However, policymakers will likely take a cautious approach to loosening policy amid signs of inflationary pressures pivoting away from services towards manufacturing, where Red Sea shipping delays and higher freight prices are adding to costs again. The renewed hiring trend could also add to pay pressures, sustaining some stickiness of inflation in the coming months.

Output growth accelerates into third quarter

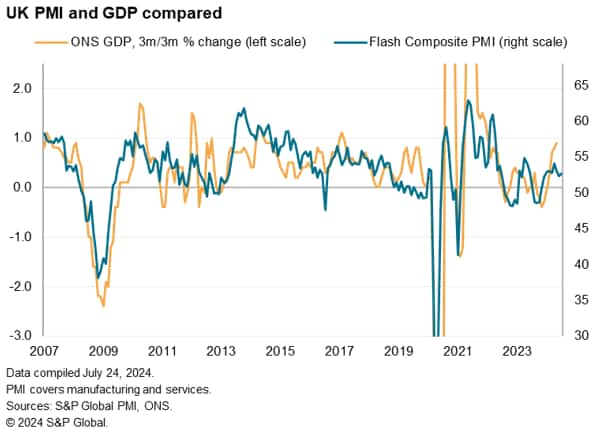

Business activity rose for a ninth successive month in July, according to early PMI survey data, the rate of growth picking up momentum amid rising levels of new business. The headline economic growth indicator from the flash PMI surveys, the seasonally adjusted S&P Global UK PMI Composite Output Index, rose from 52.3 in June to 52.7 in July. Although the latest expansion was the second-weakest recorded so far this year, the latest PMI reading is broadly indicative of the UK economy growing at a quarterly rate of just over 0.2%, based on the historical relationship of the PMI with GDP, pointing to a robust start to the third quarter.

Prior PMI data indicated an expansion of just under 0.3% in the second quarter and a 0.25% rise in the first quarter. So far this year, official GDP data have come in stronger than the PMI, signaling a 0.7% expansion in the first quarter and hint at growth of 0.5-0.6% in the second quarter. However, these GDP gains in 2024 so far come on the heels of a weaker picture in the second half of 2023 than signalled by the PMI, with the GDP data having indicated a mild recession in the final two quarters of the year. This greater variance than the PMI could in part be due to greater seasonality being present in the GDP data.

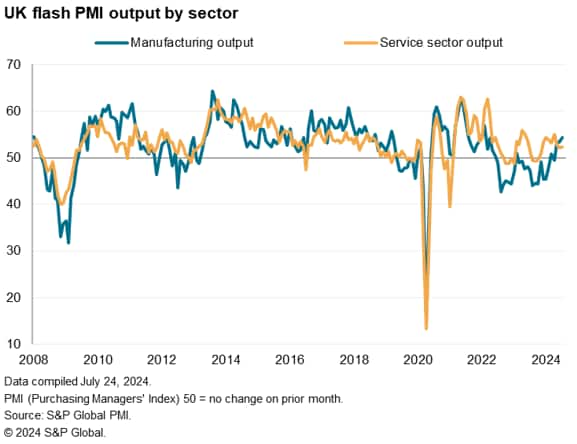

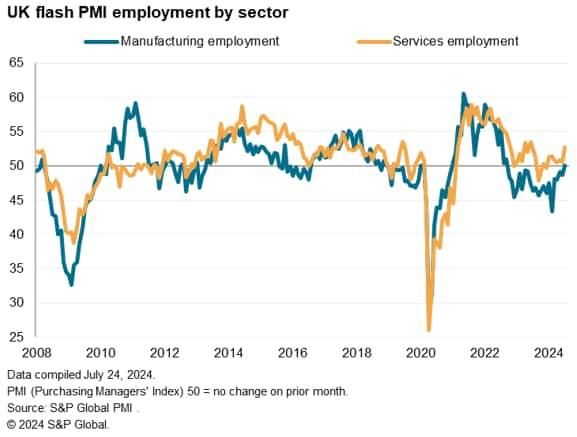

Manufacturing sector drives the upturn

Growth accelerated in both manufacturing and service sectors in July, though it is the goods producing sector which has reported the stronger pace of expansion now for three successive months. The July survey showed manufacturing output growing at the fastest rate for 29 months, outpacing the expansion seen in services to a degree not seen since the COVID-19 lockdowns of January 2021, which inhibited service sector activities. However, service sector growth also ticked higher from June's seven-month low, albeit remaining the second-weakest recorded since last November.

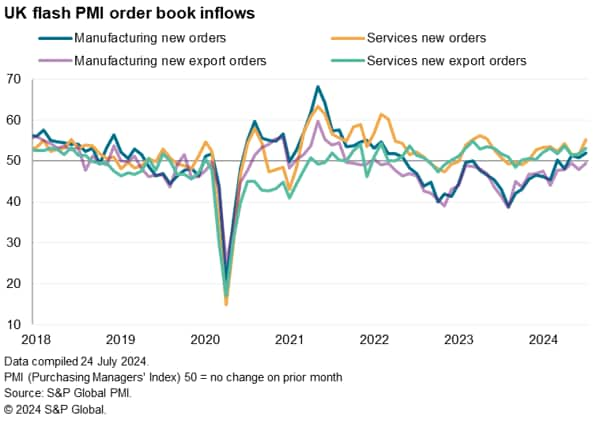

Resurgent demand

While the service sector lagged manufacturing in terms of current output, the picture reversed for new order inflows. New orders in the service sector rose in July at the steepest rate recorded since May of last year, the rate of increase accelerating sharply from the subdued rates seen in the prior two months. A relatively more modest gain was recorded in terms of manufacturing order inflows, where order book growth was impeded by a further decline in exports (albeit the smallest for 28 months). However, even in the goods-producing sector the rise in orders was the largest seen since February 2022.

The overall rise in orders for goods and services was consequently the largest reported since April of last year.

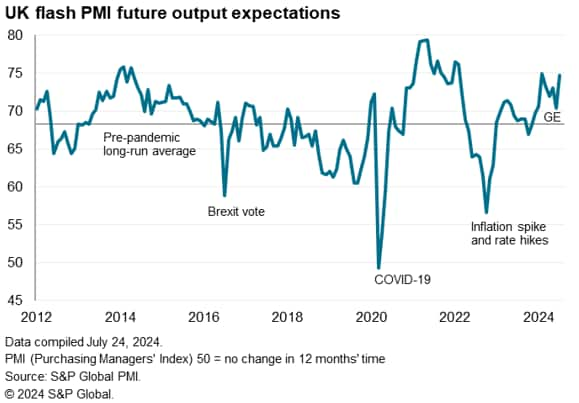

Future optimism rebounds

In addition to order inflows improving, business optimism about the year ahead revived from June's six-month low to fall just shy of the two-year high recorded back in February. The improvement in confidence in part reflected positive sentiment following the General Election (GE), as well as reflecting signs of strengthening customer demand, additional marketing and the expansion of capacity through higher employment.

Future output expectations improved in both manufacturing and service sectors, pushing the overall degree of confidence well above the pre-pandemic long run average.

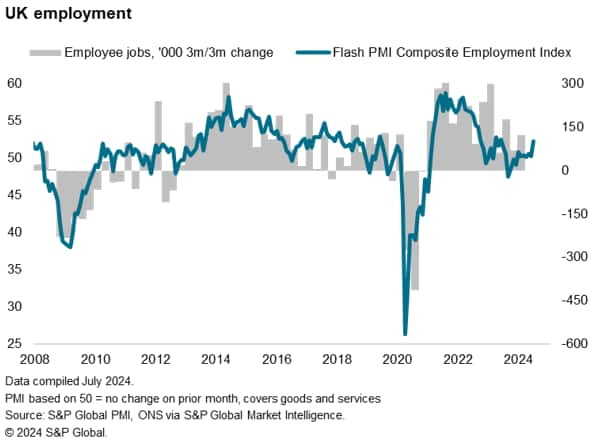

Jobs growth at 13-month high

Employment rose across manufacturing and services in July at a rate not seen since June of last year as firms expanded workforces to meet demand. Although the rise in employment was limited to the service sector, the July survey was notable in recording a stabilisation of factory payroll numbers to end a 21-month run of continual job shedding in the sector.

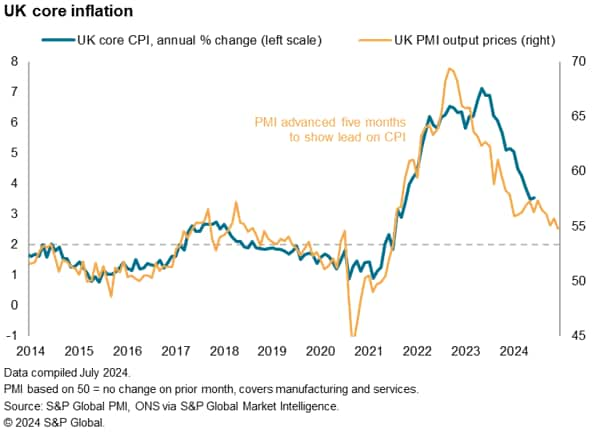

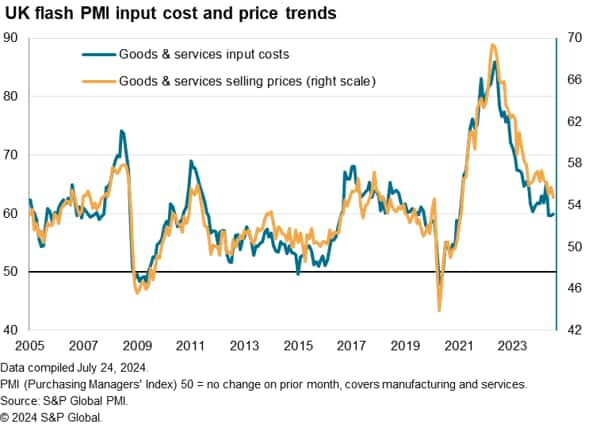

Inflation set to cool further

The overall PMI selling price gauge, covering both goods and services meanwhile fell to its lowest since February 2021, indicating a further moderation of inflationary pressures. The composite PMI price charged index is consistent with core consumer price inflation cooling to around 2.5% from its current 3.5% rate.

With policymakers especially keen to see signs of softer service sector inflation, which has been worryingly stubborn in recent months, the July survey brought encouraging signals. Service sector selling price and input cost inflation rates both moderated to their lowest since February 2021.

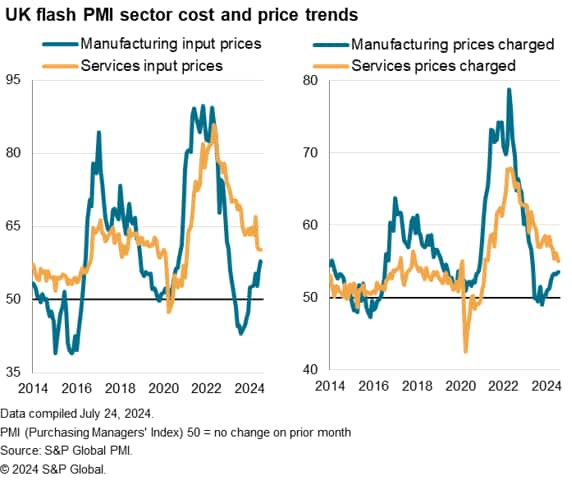

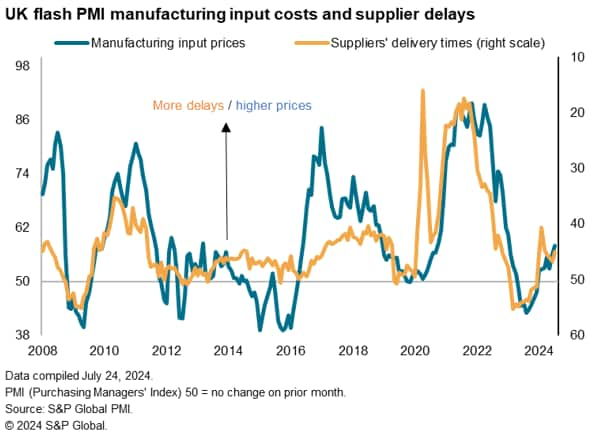

Goods prices rise at increased rate amid tighter supply

The news on inflation was not all good, however, with the July survey sounding a cautionary note from an inflation perspective. While service sector price pressures moderated, manufacturers reported a further increase in selling price inflation amid steeper cost growth. Average prices charged for goods leaving the factory gate rose at the fastest rate since May of last year, with input cost inflation accelerating to its highest since January of last year.

Manufacturers reported higher supplier prices in part due to the recent strengthening of demand, though supply constraints - often linked to Red Sea disruptions - and higher shipping costs were also widely reported. Measured overall, supplier delivery times lengthened in July to the greatest extent since March, and have lengthened continually so far this year to signal a shift from a buyers'- to a sellers'-market for many inputs.

Although the upturn in manufacturing input costs meant the survey's overall gauge of cost growth also ticked higher for a second successive month, the overall rate of cost inflation remains only modestly higher than witnessed over the decade preceding the pandemic. At present levels, the cost index is therefore consistent with relatively moderate consumer price inflation, and arguably further downward pressure on selling prices, but hawkish policymakers will potentially raise some concerns about cost growth in the light of the upturn in factory input prices and the renewed strengthening of the labour market.

Access the press release here.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Tel: +44 207 260 2329

© 2024, S&P Global. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-pmi-shows-uk-businesses-gaining-confidence-as-selling-prices-rise-at-slowest-rate-for-3-years-Jul24.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-pmi-shows-uk-businesses-gaining-confidence-as-selling-prices-rise-at-slowest-rate-for-3-years-Jul24.html&text=Flash+PMI+shows+UK+businesses+gaining+confidence+as+selling+prices+rise+at+slowest+rate+for+3%c2%bd+years+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-pmi-shows-uk-businesses-gaining-confidence-as-selling-prices-rise-at-slowest-rate-for-3-years-Jul24.html","enabled":true},{"name":"email","url":"?subject=Flash PMI shows UK businesses gaining confidence as selling prices rise at slowest rate for 3½ years | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-pmi-shows-uk-businesses-gaining-confidence-as-selling-prices-rise-at-slowest-rate-for-3-years-Jul24.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Flash+PMI+shows+UK+businesses+gaining+confidence+as+selling+prices+rise+at+slowest+rate+for+3%c2%bd+years+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-pmi-shows-uk-businesses-gaining-confidence-as-selling-prices-rise-at-slowest-rate-for-3-years-Jul24.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}