Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Aug 22, 2024

Flash UK PMI signals faster economic growth and lower inflation in August

August is witnessing a welcome combination of stronger economic growth, improved job creation and lower inflation, according to provisional PMI survey data.

Both manufacturing and service sectors are reporting solid output growth and increased job gains as business confidence remains elevated by historical standards.

Although GDP growth looks set to weaken in the third quarter compared to the impressive gains seen in the first half of the year, the PMI is indicative of the economy expanding at a reasonably solid quarterly rate of around 0.3%.

Inflationary pressures have meanwhile moderated further in August, including notably in the service sector, which has been a key area of concern for the Bank of England.

The latest survey data therefore help lower the bar for further interest rate cuts, although the still-elevated nature of inflation in the service sector suggests that policymakers will move cautiously.

Output growth ticks higher

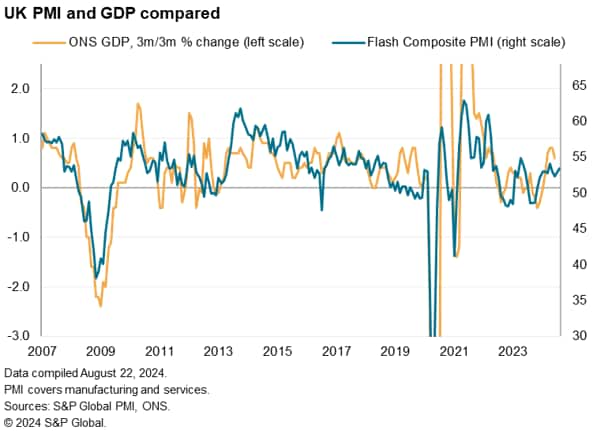

Business activity rose for a tenth month running in August, according to early PMI survey data, the rate of growth picking up momentum to the fastest since April and the second fastest in the past 15 months. The headline economic growth indicator from the flash PMI surveys, the seasonally adjusted S&P Global UK PMI Composite Output Index, rose from 52.8 in July to 53.4 in August.

The latest PMI reading is broadly indicative of the UK economy growing at a quarterly rate of 0.3%, based on the historical relationship of the PMI with GDP, adding to signs that the economy sustained a robust pace of expansion in the third quarter.

Official GDP data have come in stronger than the PMI so far this year, signaling a 0.7% expansion in the first quarter and a 0.6% rise in the second quarter, but many economists, including those at the Bank of England, expect the pace of growth to moderate in the second half of the year to a rate more in line with that signalled by the PMI.

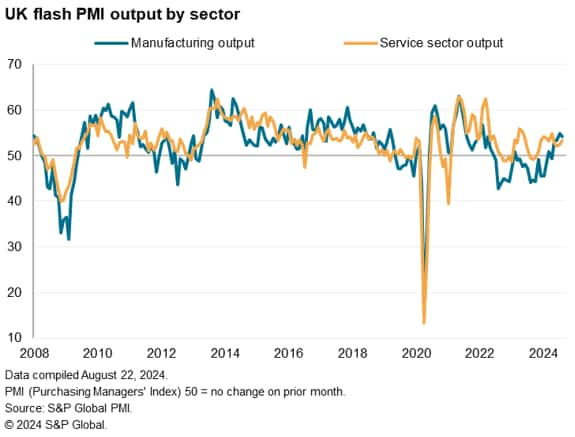

Manufacturing sector continues to revive alongside sustained services expansion

A reviving manufacturing sector led the economic expansion for a fourth consecutive month in August. Factory output has now risen in five of the past six months, marking a welcome recovery after the steep declines seen throughout late 2022 and much of 2023. Although manufacturing output growth slowed in August, the past two months have seen the strongest back-to-back increases since the opening months of 2022.

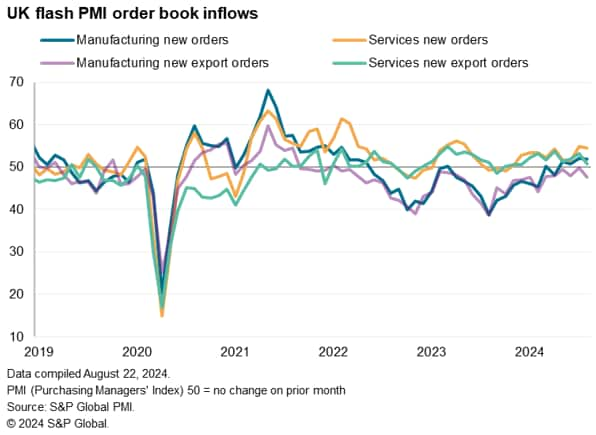

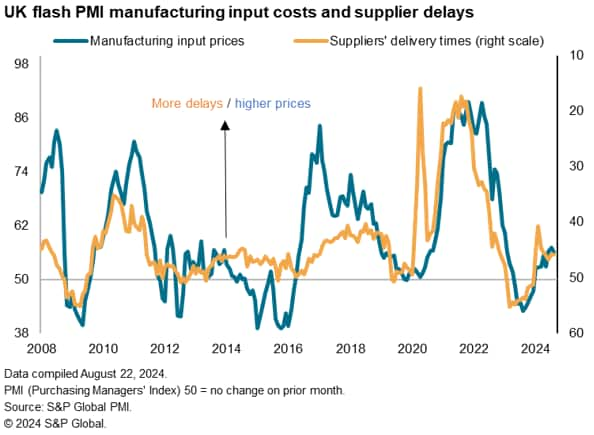

The latest manufacturing production expansion was driven by reviving domestic demand, as export orders for goods continued to fall in August, dropping at an increased rate to register a thirty-first successive monthly decline.

Service sector activity meanwhile grew at the fastest rate since April, rising for a tenth month in a row. As with manufacturing, the main stimulus to services activity was domestic demand, with export sales growth weakening in August to an eight-month low to register only a modest increase. Within services, the expansion was largely fueled by Tech & IT followed by Financial services.

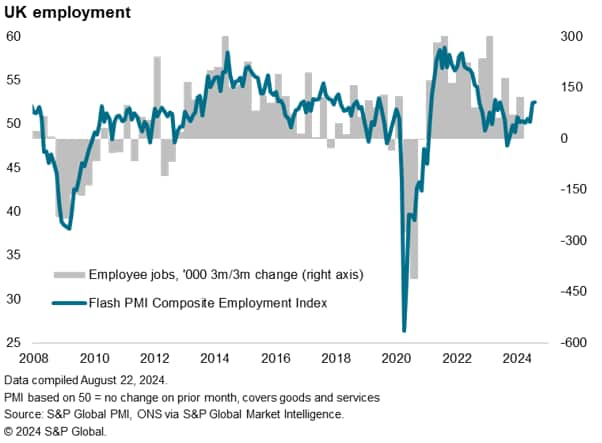

Jobs growth edges up to 16-month high

The sustained expansion of output in August was accompanied by increased job creation. Employment rose at the fastest rate for 16 months, representing an eighth month of net job gains after the falling employment seen in the closing four months of 2023. The current PMI employment index is broadly consistent with 100,000 jobs being added to the economy in the third quarter.

Service sector jobs growth cooled slightly compared to July, but the August rise was still the second largest for over a year. However, the biggest improvement in recent months has been seen in the manufacturing sector, where employment rose for a second month in August, increasing at a rate not seen for just over two years.

Inflationary pressures wane further

Despite rising staff costs continuing to be widely reported amid the expansion of workforce numbers, overall inflationary pressures cooled further in August.

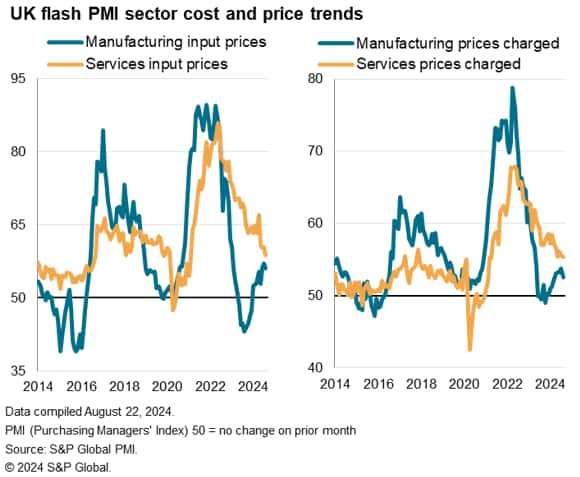

Input costs across goods and services rose collectively at the slowest rate since January 2021, led lower notably by a softening of services inflation to the lowest since February 2021. Importantly, the current rate of services inflation is now only marginally above ten-year average preceding the pandemic, pointing to a normalisation of cost trends in a sector which has been the principal inflationary concern of policymakers in recent months.

While manufacturing input costs rose, often linked to supply chain shortages, shipping delays and higher import prices, the rate of increase moderated from July's one-and-a-half-year high.

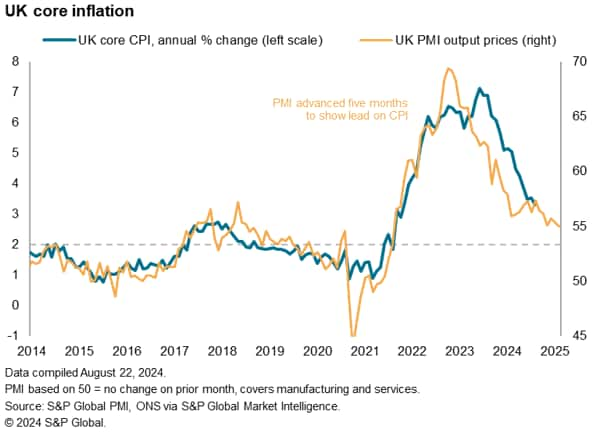

The softening of input cost pressures fed through to lower selling price inflation, which moderated for both goods and services in August. The overall PMI selling price gauge consequently fell to its joint-lowest since February 2021, consistent with a further reduction of core inflation from its current 3.3% annual rate. The rate of inflation signalled by the PMI nevertheless remains elevated by historical standards - the current selling price index reading of 55.0 compares with a pre-pandemic decade average of 52.2 - to suggest some stubbornness of price pressures, particularly in the service sector.

Outlook

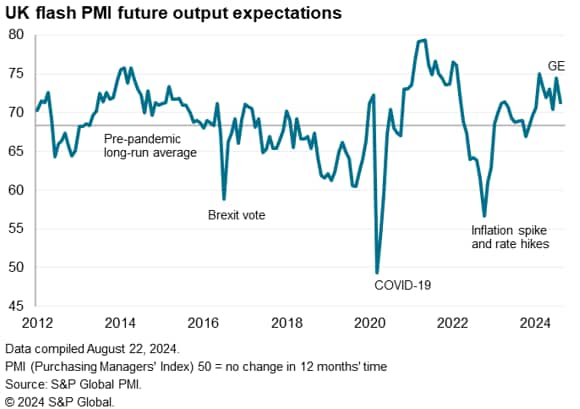

Looking ahead, future output expectations softened in both manufacturing and services in August though the overall level of optimism remained well above the survey's long-run average. Thus, while the pull-back in sentiment hints at output growth potentially slowing in September, any slowdown is likely to be only modest with contraction avoided in the near term.

S&P Global Market Intelligence economists are therefore forecasting UK GDP growth to slow to around 0.25% in both the third and fourth quarters of 2024. After the strong 0.7% and 0.6% gains seen in the first two quarters of the year respectively, that would result in 1.0% GDP growth for the year.

This slowdown, combined with the further moderation of price pressures seen in the August flash PMI surveys, opens the door further for a loosening of monetary policy later in the year.

The Bank of England lowered its policy rate by 25 basis points to 5% at its July meeting, its first cut since March 2020. The decision was 'finely balanced' with five of the nine members of the Bank's Monetary Policy Committee voting for a rate cut. Bank Governor Andrew Bailey stated that this should not be seen as the start of a rapid decline in rates, highlighting the risk of loosening monetary policy too quickly while inflation remains high. S&P Global Market Intelligence economists consequently expect only one additional 25-basis-point cut this year, taking the policy rate down to 4.75%, though there is clearly a chance that MPC could be further encouraged towards a September rate by these recent PMI numbers.

Access the press release here.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Tel: +44 207 260 2329

© 2024, S&P Global. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-uk-pmi-signals-faster-economic-growth-and-lower-inflation-in-august-2024.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-uk-pmi-signals-faster-economic-growth-and-lower-inflation-in-august-2024.html&text=Flash+UK+PMI+signals+faster+economic+growth+and+lower+inflation+in+August+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-uk-pmi-signals-faster-economic-growth-and-lower-inflation-in-august-2024.html","enabled":true},{"name":"email","url":"?subject=Flash UK PMI signals faster economic growth and lower inflation in August | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-uk-pmi-signals-faster-economic-growth-and-lower-inflation-in-august-2024.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Flash+UK+PMI+signals+faster+economic+growth+and+lower+inflation+in+August+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fflash-uk-pmi-signals-faster-economic-growth-and-lower-inflation-in-august-2024.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}