Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Nov 15, 2022

Global Trade Monitor – November 2022

This analytics article utilizes trade data published by S&P Global Market Intelligence-Global Trade Analytics Suite (GTAS)

Key Observations

- Data for mainland China show that after a positive trend in year-on-year growth for exports in June and July 2022 (17.7% and 17.8% increase, respectively), we can observe a significant slowdown in mainland China exports in August (7.0% growth y/y) and September (5.6% growth y/y).

- The highest growth in Value of Imports in August 2022 was noted by India, with imports increasing by 41.0 % y/y, followed by Brazil, marking 36.5% growth year on year.

- Adjusted Purchasing Managers' Index - New Export Orders (PMI NExO) for global manufacturing for September was the lowest since the first wave of COVID-19 pandemics in February-July 2020 suggesting the inevitable spillover of the global economy's slowdown into international trade.

- The newest data on inflation published by the S&P Market Intelligence team in October show another upward-revised forecast of inflation in the next few quarters.

- Global real GDP growth is projected to slow from 5.9% in 2021 to 2.8% this year and 1.4% in 2023. S&P Global Market Intelligence revised down the 2023 growth rate 0.6 percentage point from last month's forecast.

- Consequences of the global economic slowdown are not that apparent in the monthly data for 2022 as in the first three quarters of the year the dynamics of exports and imports were relatively strong in the top 10 economies.

Changes in trade of the top 10 economies

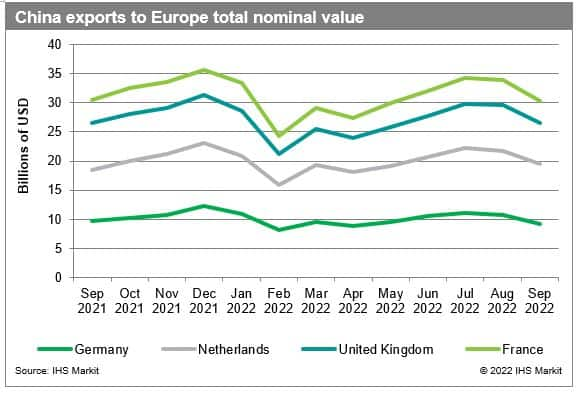

Data from Global Trade Analytics Suite (GTAS) for August 2022 show that the year on year growth in the value of exports is slowing down in most of the top ten economies, except for United Kingdom marking 36.8% growth y/y (up from 20.9% increase in July) and India reaching 10.6% growth y/y (up from 8.4% y/y in July). In August we could also observe negative growth rates in export value for EU External trade (-4.0% y/y) and Japan marking negative year on year growth for the fifth month in a row.

Mainland China data show that after a positive trend in year-on-year growth for exports in June and July 2022 (17.7% and 17.8% increase, respectively), we can observe a significant slowdown in mainland China exports in August (7.0% growth y/y) and September (5.6% y/y).

The slowdown in Chinese exports in August and September was driven by decelerating overseas demand caused by geopolitical tensions, rising interest rates and inflation on one hand and new COVID outbreaks and lockdowns, as well as heatwaves in south-western provinces on the other, adding additional constraints to factory output and domestic logistics and disrupting outbound shipments.

Looking at the most recent results in the value of imports, the highest growth in August 2022 was noted by India, with imports increasing by 41.0 % y/y (a slight decline from 43.1% in July). The country was followed by Brazil, marking 36.5% growth year on year (up from 35.2%in July).

The latest available data for mainland China imports show that after limited, but still positive growths in imports by 1.5% and 2.5% in June and July 2022, we can observe negative growth for imports in August and September 2022 (-0.2% y/y and -0.4% y/y, respectively).

The property crisis and heatwaves mentioned already earlier, have not only impacted export but also import side, weakening domestic demand. New covid outbreaks across the country have also disrupted inland logistics and hurt factories output. On the other hand, the heatwaves led to increase in coal imports as additional source of fuel was needed to meet growing demand for electricity.

Four economies had already published data for September 2022—Brazil, mainland China, Japan and South Korea, with the highest growth for exports reported by Brazil (18.8 % y/y). In terms of imports, Brazil also marks high increase in September 2022 (25.0% y/y),but slowing down from 36.5% noted in August. The country is followed by South Korea, with 18.6% growth y/y, also a significant slowdown from 28.1% y/y growth in August 2022.

September's results of adjusted Purchasing Managers' Index - New Export Orders (PMI NExO) for global manufacturing indicate another - already seventh in a row - drop below the benchmark of 50.0 points and equaled 45.9. The readout for September was the lowest since the first wave of COVID-19 pandemics in February-July 2020 suggesting the inevitable spillover of the global economy's slowdown into international trade.

At the same time, the results for global services fell below 50.0 points for the fourth time in a row, after seven months of consecutive above-50 readouts and equaled 48.1, which shows a relatively flat pattern over the last few months: 48.1 points in August, 48.3 in July and 48.5 in June. This may indicate stronger resilience of services to the global economic slowdown, which is in line with previous expectations for services to remain the engine of growth from the last few months.

Prospects for the Forthcoming Months

Global economic situation keeps worsening as inflation remains high and financial market conditions tighten. The months ahead will likely bring recessions in Europe, the United States, Canada, and parts of Latin America. With moderate growth in Asia Pacific, the Middle East, and Africa, the world economy can avoid a downturn, but growth will be minimal.

Global real GDP growth is projected to slow from 5.9% in 2021 to 2.8% this year and 1.4% in 2023. S&P Global Market Intelligence revised down the 2023 growth rate 0.6 percentage point from last month's forecast, reflecting dimmer outlooks in every major region of the world.

The newest data on inflation published by the S&P Market Intelligence team in October show another upward-revised forecast of inflation in the next few quarters. Now, it is estimated that inflation has reached an 8.10% level the third quarter of 2022 (0.1 p.p. less than expected before), compared to 7.61% in the second quarter, and 6.03 in the first quarter of 2022. The decay of inflationary pressure is expected to start in the second quarter of 2023 (5.20%) and return to the long-term trend from the further in 2024. At this point (the third quarter of 2022), the inflation in emerging markets exceeds the world average and advanced economies - 8.24% versus 8.10% and 7.76%, respectively.

Impact of the war in Ukraine on world trade is still expected to decrease global trade in 2022 by approximately 1 p.p. From the trade perspective the situation is stable, despite the dynamic changes in the conflict itself. At the same time, the most recent events in Sevastopol put into question the grain export deal between Ukraine and Russia. After the initial withdrawal of Russia, on November 2 Russian officials confirmed that the agreement is still valid after receiving appropriate guarantees from Ukraine. For now, the deal is mediated by Turkey via Joint Coordination Centre in Ankara and allowed for almost 10 MMT of food exports. GTAS Forecasting expects the deal to continue in the forthcoming months, reducing the threat of further destabilization in the food markets.

The data shows clearly that mainland China is slowing down, due to the global macroeconomic situation as well as strict COVID-19 restrictions and lockdowns from the first half of 2022. Problems of the second largest economy in the World may be considered as an opportunity for other countries in the region as ASEAN or South Asian economies. COVID policies of those countries have been totally different. Opening borders for tourists has already brought stimulus to economic growth for Thailand and Malaysia for instance, both heavily relying on the tourism sector.

There is no doubt that mainland China is still the global exports superpower, but current constraints deriving from the very strict COVID policy as well as Xi Jinping's economic policies to large extent responsible for the slowdown and scaring away foreign investors might impact the global trade patterns in the long-term. ASEAN region as well as South Asian nations, especially Vietnam, Indonesia, Philippines or Bangladesh, are perceived as the largest possible beneficiaries of mainland China slowdown, attracting investors with their friendly policies, young, large workforce, strategic localization on main trade lanes and stabilizing COVID situation with very limited restrictions or even full reopening of economies.

Expectations for international trade in the next

months

The global economic slowdown is more and more visible in the data. Monthly historical data by GTAS clearly shows that in the top 10 economies exports are primarily impacted slowing down in the majority of economies within the group. The picture is slightly more optimistic for imports, yet the situation is expected to deteriorate in the forthcoming months for both exports and imports, which is reflected in the most recent PMI NExO readouts. Among the group of top 10, the most positive prospects are related to India, which seems to not be impacted by the global economic slowdown to a large extent.

At the same time, the global geopolitical framework seems to be stabilizing after a few months of volatility and uncertainty. The impact of the two most important events impacting global trade: the war in Ukraine and the COVID-19 pandemic is now better visible in the data and understood by experts as new trade patterns arise.

The consequences of the global economic slowdown are not that apparent in the monthly data for 2022 as in the first three quarters of the year the dynamics of exports and imports were relatively strong in the top 10 economies. This should translate in still positive growth in 2022 from the yearly perspective, yet in 2023 global trade contraction may be expected. GTAS Forecasting expects trade recovery to start in 2024, returning to the long-term stable growth path.

Leading Economies of the World and Methodological

Issues

The top 10 economies by GDP in 2021 include the US, EU27, mainland China, Japan, the UK, India, Brazil, South Korea, Canada, and Russia.

The top 10 group member states are responsible for approximately four-fifths of the world GDP and three-quarters of global exports, with most trade carried out within the group.

In the monthly Global Trade Monitoring commentary, we present year-on-year changes in the value of exports and imports for available monthly trade data from S&P Global Market Intelligence - Global Trade Atlas (GTA) in percentage.

Data edge differs from state to state depending on a given reporter and its reporting calendar.

For the EU Member States, we consider only EU external trade with non-EU states.

Please note that historical data in the GTA database are being adjusted monthly due to revisions introduced by the reporting states, potentially causing adjustments to the growth rates reported in the commentary provided by the Global Trade Monitoring from prior months (the report reflects the most recent data available).

Subscribe to our monthly newsletter and stay up-to-date with our latest analytics

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-trade-monitor-november-2022.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-trade-monitor-november-2022.html&text=Global+Trade+Monitor+%e2%80%93+November+2022+%7c+S%26P+Global","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-trade-monitor-november-2022.html","enabled":true},{"name":"email","url":"?subject=Global Trade Monitor – November 2022 | S&P Global&body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-trade-monitor-november-2022.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Global+Trade+Monitor+%e2%80%93+November+2022+%7c+S%26P+Global http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-trade-monitor-november-2022.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}