Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Feb 03, 2021

Global Trade Outlook for 2021

Global Trade Outlook for 2021 shaped by the COVID-19 pandemic; more optimism but significant uncertainties remain.

Introduction

After an already sluggish trade in 2019 global recovery was expected in 2020. High hopes and early market optimism were devastated by the outbreak of the COVID-19 pandemic, the largest black swan event since the second WWII. 2020 as a whole and Q2 of 2020 proved to be the worst year and the worst quarter for global trade on record. COVID-19 will be the most significant factor affecting the global economy in 2021, however, a number of additional factors have to be taken into consideration.

The significant impact of COVID-19

The COVID-19 pandemic is the worst health crisis in more than a century and potentially without precedent if we take the globalized nature of the current economy. A simultaneous supply and demand shock that led to the global recession and unprecedented contraction in global trade (affecting both the export potential of nations and their demand for imports).

With 98,280,844 reported cumulative cases (WHO Weekly epidemiological update from 27 January 2021) and 2,112,759 confirmed COVID-19 related deaths globally, affecting all the states of the world, the pandemic has proved its severity already. The worst affected regions from the global perspective are the Americas, Europe, and South-East Asia.

The overall impact of COVID-19 will depend critically on the duration, severity, and spatial pattern of the pandemic.

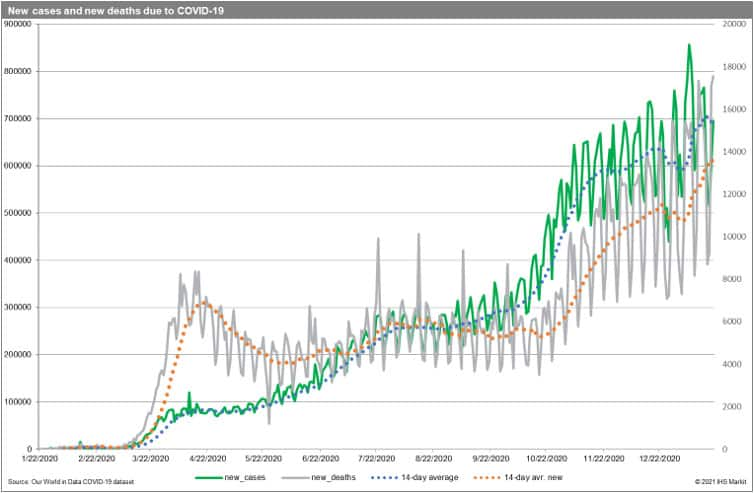

Unfortunately, COVID-19 is not yet under control and far from over. The graphs below indicate that the 2-week averages of new COVID-19 cases, as well as COVID-19 deaths, are still rising and point to a clear second wave and thus the total numbers of cases and deaths globally are still rising fast.

The severity of containment measures introduced by states are correlated (with a certain lag) and thus it is unlikely to predict a major shift in policies implemented. The change critically depends on the pandemic curve itself and in particular on the effectiveness of mass vaccination programs. The effects of them are unlikely to be felt globally before Q3 or Q4 of 2021 (the herd immunity levels of 60 - 70% of the population must be reached).

We obviously should celebrate the development of the vaccines with unprecedented speed, but many uncertainties remain, and thus despite the hike in market confidence in recent weeks we should remain cautious.

Analysis performed by the GTA Forecasting team proves that COVID-19 impacted bilateral trade flows adversely and in a statistically significant manner. This effect on global trade endures from March 2020 onwards.

The reaction in global trade was consistent with the escalating pandemic and steps taken by individual countries/territories in controlling or mitigating it (restrictions on movements, lockdowns, forced production stoppages, as well as monetary and fiscal policy stimuli).

The impact of COVID-19 is significantly larger than the prior recent outbreaks of pandemics including HIV, Ebola, SARS, or MERS in recent years and very much resembles the impact of Spanish Flu 1918-2020. It is worth stressing that the Spanish Flu pandemic lasted three years and had three distinctive pandemic waves.

The direct trade effects of COVID-19 are related to direct supply disruptions hindering production (local/ regional lockdowns & forced production stoppages), increased transport cost due to implementation of stricter rules, supply-chains contagion effect which amplified the direct supply shocks (manufacturing sectors in less-affected nations found it harder and more expensive to acquire the necessary imported inputs from the hard-hit nations) and finally to demand disruptions due to a decrease in the aggregate demand (recession), and precautionary or wait-and-see purchase delays (delayed purchases & investments).

Reporters most adversely affected are the ones struck the most by the pandemic itself as well as economies most dependent on the trade with these nations through export/import linkages (forward/backward linkages in global value chains, GVCs). Increased defragmentation of production chains and certain management principles (just-in-time and lean production with low stockpiles of inputs) increased the susceptibility of the global economy to the shock. The impact is, however, asymmetric due to the nature of the individual (sector-level) value-added chains. Some GVCs dependent on adversely affected regional or global hubs such as China, Italy, Spain, or Germany were more affected (e.g. automotive industry, electronics). Some industries or sectors gained on the crisis (e.g. pharmaceuticals, IT services). Nonetheless, the gradual recovery in global merchandise trade in Q3 and Q4 proved the resilience of global value chains to supply disruptions.

Individual economies and groups of economies took unprecedented steps to mitigate the crisis, which could have negative consequences for public finances and global debt levels similar to the recent global financial crisis. This increases the probability of the W-shape scenario (the initially assumed V-shape with a strong recession followed by sharp recovery is already highly unlikely).

We already understand that the impact of a pandemic won't be limited to the short-run. It is likely to have long-term consequences as well. We are likely to observe more pronounced adjustments to GVC/trade patterns (trade diversion effects) the larger, the longer the pandemic lasts.

Other important qualitative factors that could affect global trade in 2021

The UK-EU trade agreement, negotiated and ratified at the last possible moment, took effect from 23:00 GMT on 31 December 2020. Thus, the potential hard-Brexit did not materialize, nonetheless, the situation in January 2021 proves that Brexit is costly, and Britons are experiencing the first adverse side-effects.

The Regional Comprehensive Economic Partnership (RCEP) Agreement was signed on 15 November 2020. The RCEP is a multilateral, regional agreement extending and deepening the free trade between the member states of the Association of Southeast Asian Nations (ASEAN) and its existing trade partners China, Japan, and South Korea (the so-called ASEAN Plus Three) as well as Australia and New Zealand. RCEP is the first multilateral agreement to include China (mainland) and establishes the first free trade agreement between China and Japan, as well as Japan and South Korea. RCEP will enter into force following ratification by at least six ASEAN countries and three non-ASEAN signatory countries and it will take the effect 60 days after it has been ratified. The process of ratification can be lengthy and take several months, nonetheless, it should be completed in 2021.

Upon entry into force, RCEP will be the world's largest regional trade agreement in terms of GDP & population. RCEP's countries currently account for about 29% (USD 25.8 trillion) of global gross domestic product and approx. 29% (2.3 billion) of the world's population. It is worth stressing that the RCEP countries dealt better with the COVID-19 pandemic than the majority of other regions of the world and the region is already driving the global recovery.

RCEP can thus due to its size and intended scope create significant quantitative and qualitative effects regionally and globally both in the short and the long-run (significant static, as well as dynamic effects, are very likely). It could strengthen the economic position of the region as the main locus of economic activity spurring the growth of the region but also globally which could be a crucial element of recovery from COVID-19. RCEP increases the likelihood of establishment of the world's largest regional value chain with the growing role of intra-regional economic activity.

The cultural, social, economic, and political heterogeneity of the block will be a challenge to its functioning and progress will depend on the balance of costs-and-benefits for all participating states. Realizing the potential benefits of this mega-regional FTA will crucially depend on addressing the major challenges in particular divergent political and economic interests of this diverse group.

It is worth looking at RCEP from a broader perspective though. Over several decades, the global trade system itself is likely to develop into a system of several large RIAs or mega-regional trade agreements (e.g. European, Pan-American & Asian) with a significant role in the global trading system and potentially large tensions between them. The development of RCEP can be considered a significant step in this process. This could speed up the process of emergence of the so-called FTA of Americas and puts extra pressure on the European Union significantly weakened due to Brexit.

It will also be interesting to observe the impact of RCEP and its trade rules on the multilateral system and the potential erosion of the WTO dominance in global trade governance despite the statements made on the complementarity of both systems. The additional factor to be raised in this context is the choice of the new WTO Director-General which can potentially bring the changes to multilateral trade policy to better reflect the global challenges - the post-COVID-19 recovery, resurrection of restrictive trade policies, and increasing trade wars and climatic change.

Recent years in the global trade were affected by rising trade tensions in particular between the US and China due to the policies of the Trump administration (America First). The new Biden administration that took office on 20 January 2021 is likely to modify the course and in general pursue a broader, more multilateral trade policy. Nonetheless, a stronger stance on China will likely remain. However, the incoming administration is likely to repair trade ties with US traditional partners and pursue policy more open policy with international bodies such as the WTO (WHO).

Taking into account the emergence of RCEP, the new US administration's trade agenda is very likely to gravitate towards Asia. We can thus expect a shift in US trade policy towards Asia which is likely to bring effect rather in the mid to long-term.

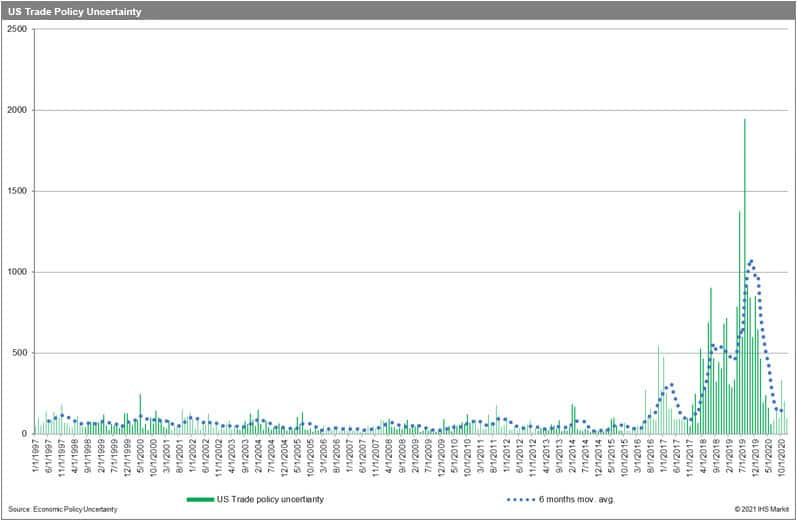

The US trade policy uncertainty is falling, and the trend is likely to be strengthened under the new administration.

Some countries will hold important presidential and parliamentary elections in 2021. From the European perspective, the German federal elections in September 2021 could mark a major change with the declaration of Angela Merkel not to run for the chancellor's office. The shift in power in Germany could have an important impact on Germany's and EU policies.

In addition, several potential hotspots could be named. The unresolved issue of Iran's nuclear program, the unresolved conflicts between Russia & Ukraine, Armenia & Azerbaijan as well as potential terrorist attacks globally and in the Persian Gulf regions are a few factors to be closely observed as they could easily impact the global economy if they escalate.

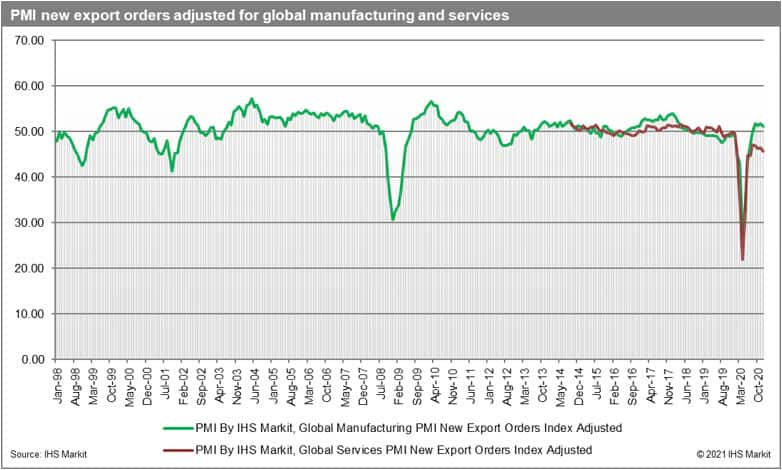

PMI new export orders

PMI New Export Orders (adjusted) by IHS Markit is a very good predictor of the situation in trade over the forthcoming quarter. The 50.0 points is a benchmark value with a value above pointing to recovery and below indicative of contraction.

As can be seen both PMI NExO for manufacturing and services suffered a severe downturn with readouts for March and April 2020 significantly worse than in the 2008-09 global financial crises. Nonetheless, they followed a V-shape recovery in the latter part of 2020. From September onwards, the PMI for global manufacturing trade is above the benchmark value. PMI NExO for trade in services has unfortunately not recovered and shows a downward trend from September onwards. The latest available readouts from December 2020 stood at 51.10 for global exports of manufacturing goods and at 45.66 for global exports of services.

Some estimates have been already provided for January 2021 and the readouts stand at 48.80 for Japan, 46.69 for the UK (it could reflect the disappointment with the results of the UK-EU trade agreement and the firsts adverse impacts of Brexit - the readout for December stood at 55.56) and 54.02 for the US (this, in turn, could reflect the optimism related to the shift of power from Trump's to Biden's administration and hopes for major changes in US trade policy).

IHS Markit growth scenario

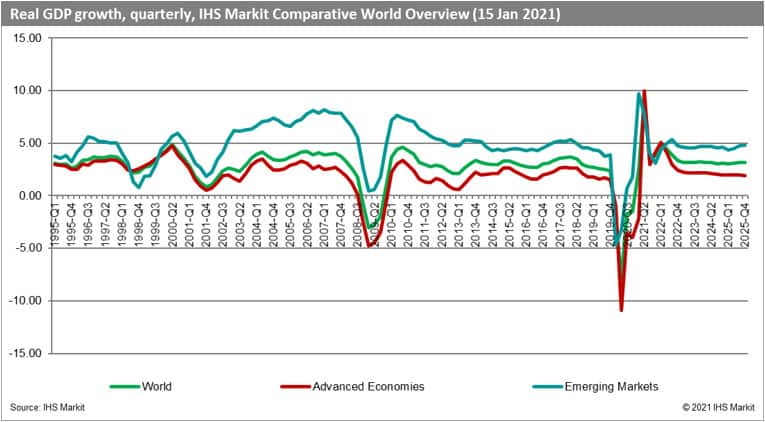

The most recent real GDP growth forecasts from IHS Markit were published on 15 January 2021. The forecast includes the baseline scenario of the impact of COVID-19 on the global economy and individual states.

We now estimate the contraction of global GDP of 4.0% in 2020 varying between -5.0% for advanced, -2.2% for emerging, and -6.6% for developing economies. The recession in 2020 thus was global and significantly more severe than in 2009 (caused by the financial crisis).

We predict growth to recover globally in 2021 with year-on-year global growth rates predicted to reach 4.5% (3.9% in 2021). This would vary between 3.7% for advanced economies (3.4% in 2022), 5.7% (4.7%) for emerging and 5.7% (4.2%) for developing states.

From a quarterly perspective, both Q3 (-1.7%) and Q4 (-1.5%) proved to bring a continuing recession. We predict a recovery already in the Q1 of 2021 (2.5%) with a major boost only in Q2 of 2021 (9.1%). The recovery has already started and is mostly driven by East Asia in particular China and Vietnam. Emerging states are doing better than advanced states.

Growth impulse will be particularly strong in China in Q1 2021 followed by a recovery in other top economies in Q2 2021 which is forecasted to be particularly strong in India, the UK, Canada, and the EU, and the most moderate in South Korea and Russia. China is the only top ten economy to have already recovered in 2020.

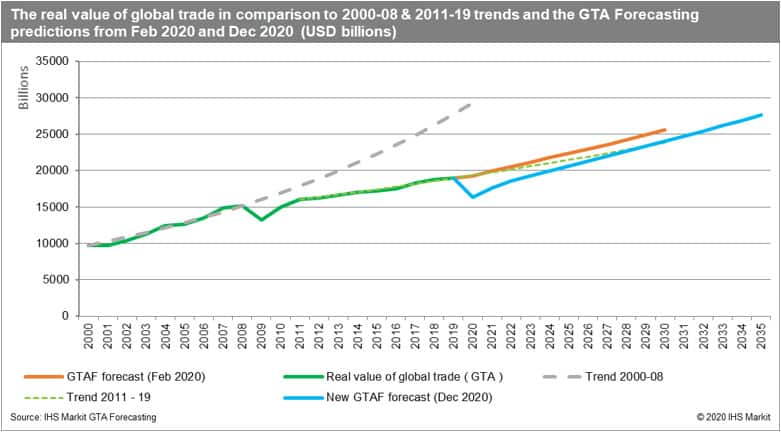

Our trade forecast for 2021 and forward

The new release of the GTA Forecasting model from December 2020 accommodated the most recent macroeconomic forecasts of the IHS Markit Global Link Model, the actual data for the first two quarters of 2020 from the Global Trade Atlas (GTA) for all monthly reporting states, and updated COVID-response factors.

The GTA Forecasting model estimates a contraction of global merchandise trade in 2020 to USD 16,382 billion or -13.5% year-on-year (it represents a slender downward adjustment from the values predicted in the August release).

The estimated contraction is close to the results reported by the OECD and IMF and close to the estimated "optimistic scenario" of the WTO from April 2020.

We predict a year-on-year increase in the real value of global trade of 7.6% in 2021 and 5.2% in 2022. This accommodates the forecasted recovery in global GDP in 2021 and a particularly strong growth impulse expected in Q2. The predicted CAGR for the period 2021-2030 equals 3.5%.

In terms of volumes, we estimate a contraction of global trade in 2020 to 12.7 billion metric tons or by 11.2% year-on-year.

We forecast the volume of global merchandise trade to grow to 13.65 billion metric tons in 2021 and 14.2 billion metric tons in 2022. This points to a recovery in the forthcoming years with year-on-year growth rates of 7.5% in 2021 and 4.1% in 2022.

This will allow the global economy and in particular the transport community to regain momentum and to recoup some of the losses from the trade collapse of 2020.

The forecasted CAGR for global trade volume stands now at 3.2% in the period 2021-30.

For comparison, the CAGR averaged 3.6% in the period 2000-19 and an impressive 5.6% in the period 2000-08 preceding the global financial crisis. The CAGR for the period 2011-19 was 2.1%.

The estimated contraction in global trade volume in 2020 (-11.2%) is higher than the contraction in the global financial crisis (-7.7%) thus the adverse impact of COVID-19 on global trade can be judged significantly larger than the impact of the global financial crisis.

Furthermore, we would like to stress that the forecasted average growth rate for the period 2021-30 is above the average for the period 2011-19 but significantly below the growth path of global trade volume preceding the global financial crisis.

The estimated recovery can be strong enough to bring trade close to its pre-pandemic trend (2011-2019) but only around 2029.

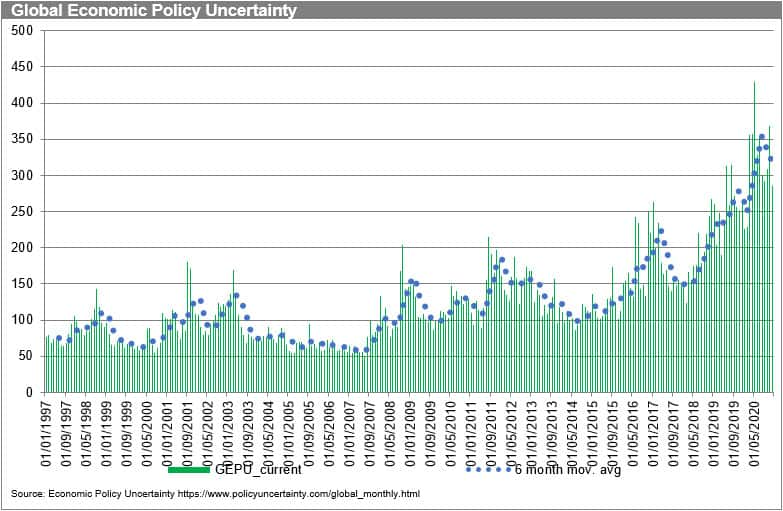

Global uncertainty

The forecasts should be treated with a large degree of caution. Several scenarios are still possible. The index of Global Economic Policy Uncertainty (www.policyuncertainty.com/global_monthly.html) is still at its historically highest levels nonetheless its 6-month average is going down.

Economic developments will critically depend on the shape of the pandemic curve and the severity of containment efforts taken globally and by individual states as well as the effectiveness of vaccination programs globally.

The program has already encountered significant problems in advanced states. Taking into the global variation of quality of institutions and individual health systems this will present a major challenge in particular to weaker developing economies.

The global vaccination program has to be introduced and well-coordinated for the situation to improve and revert to pre-pandemic (or the so-called new normal).

GTAF predictions vis-à-vis the forecasts by other organizations

WTO

In an updated autumn 2020 report, the WTO forecast a 9.2% decline in the volume of world merchandise trade, followed by a 7.2% rise in 2021. Trade volume growth thus would remain clearly below the pre-crisis trend.

The projected decline was less than the 12.9% drop foreseen in the optimistic scenario from the WTO April trade forecast and far away from the potential "adverse" scenario from the same release. The WTO economist stressed several downside risks mostly associated with uncertainty over the evolution of the COVID-19 pandemic. WTO estimated the contraction of global GDP by 4.8% in 2020 followed by a 4.9% increase in 2021.

IMF

IMF projections from October 2020 estimated a decrease of -10.4% in 2020 and a growth of 8.3% in 2021 in the volume of global trade.

According to the IMF's World Economic Outlook Update from January 2021 global trade volumes are forecast to grow approx. 8% in 2021 and by 6% in 2022. This is consistent with predicted global recovery. As could be expected trade in services is forecast to recover more sluggishly mostly due to the impact of travel restrictions on cross-border tourism and business travel.

IMF predicts the global economy (according to its baseline scenario) to grow 5.5% in 2021 and 4.2% in 2022. IMF now estimates global contraction in 2020 to 3.5% (which is 0.9 percentage point higher than projected in its October forecast due to stronger-than-expected recovery across regions in the second half of the year). The 2021 forecast in comparison to the prior release were raised by 0.3 percentage point which reflected according to IMF economist additional policy support in a few large economies (mostly advanced such as the US or Japan) and expectations of a vaccine-powered strengthening of activity coming earlier than priorly expected, which offset the problems related to the next wave of the pandemic.

World Bank

World Bank has published its Global Economic Prospects just recently in January 2021. According to Outlook's baseline scenario, the global GDP is expected to grow by 4% in 2021 and 3.8% in 2022. The World Bank economist stresses the impact of the COVID-19 pandemic on investment and human capital is expected to erode growth prospects particularly in emerging and developing economies. The global recovery, which has been dampened in the near-term by a resurgence of COVID-19 cases, is expected to strengthen over the forecast horizon as confidence, consumption, and trade gradually improve, supported by ongoing vaccination.

World Bank apart from the baseline scenario presented three additional scenarios - optimistic (upside), pessimistic (downside), and significantly pessimistic (adverse downside) depending critically on the future evolution of the pandemic and the success or failure of mass vaccination programs in advanced, emerging and developing states.

The report stresses in particular the downside risks to the baseline scenario. These include, among others, the possibility of a further increase in the spread of the virus (new waves), delays in vaccine procurement and distribution, more severe and longer-lasting effects on potential output from the pandemic, and financial stress triggered by high debt levels and weak growth.

Global trade is estimated by the World Bank to have contracted by 9.5 percent in 2020—comparable to the decline during the 2009 global recession but affecting a significantly larger share of economies. Under the baseline scenario, the trade would recover and show an average growth rate of 5.1 percent in 2021-22.

Under the downside scenario (problems with recovery in advanced states) trade would recover in 2021 but the growth rate would be significantly lower the volumes would be close to 2010 figures only. Under a severe downside scenario (global recession in 2022) global trade growth would contract for a second consecutive year in 2021, followed by a moderate recovery only in 2022. Under the optimistic upside scenario of the World Bank, global trade growth would experience a strong recovery, averaging nearly 7% in 2021-22.

Summary

In contrast to other organizations, we estimate a deeper contraction in the global trade volume of 11.2% in 2020 in comparison to -9.5% by the World Bank, -9.2% by the WTO, and -8% by IMF. As to the growth in 2021, we forecast it at 7.5% (+4.1%) in 2021. WTO forecasts it at 7.2%. IMF has just decreased its forecasts from +8.3% to +6.0% while the baseline scenario of the World Bank predicts it at +5.1% (+5.1%).

Thus, our global trade volume growth forecast for 2021 is more optimistic than by other organizations.

The variance of scenarios by the World Bank indicates that the evolution of the global economic system could go in many directions. For obvious reasons (significant unpredictability of the pandemic) the forecasts should be treated with caution and could be modified by the incorporation of the incoming trade and macroeconomic data.

This column is based on data from IHS Markit Maritime & Trade GTA Forecasting, other resources of IHS Markit (e.g. PMI, Comparative World Overview) as well as external resources.

For more details about GTA Forecasting (GTA) please visit our product page

https://ihsmarkit.com/products/gta-forecasting.html

The full version of this article is available on the Connect platform for IHS Markit clients with subscription to GTA/GTA Forecasting.

Subscribe to our monthly newsletter and stay up-to-date with our latest analytics

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-trade-outlook-for-2021.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-trade-outlook-for-2021.html&text=Global+Trade+Outlook+for+2021++%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-trade-outlook-for-2021.html","enabled":true},{"name":"email","url":"?subject=Global Trade Outlook for 2021 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-trade-outlook-for-2021.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Global+Trade+Outlook+for+2021++%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-trade-outlook-for-2021.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}