Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Nov 13, 2023

Ocean carriers survey changing market and ponder next course of action

SINGAPORE — If there's one question looming above all others as the era of extreme carrier profitability recedes into the past, it is this: What will ocean carriers do next?

Behind that question is a truism often forgotten in container shipping, which is that whatever happens to pricing and service is not the result of outside forces such as recession or consumer spending exerting pressure on the market beyond the ability of the industry to control. Rather, what ultimately happens is entirely in the hands of the carriers, with their decisions determining how an unpromising year such as 2024 actually plays out.

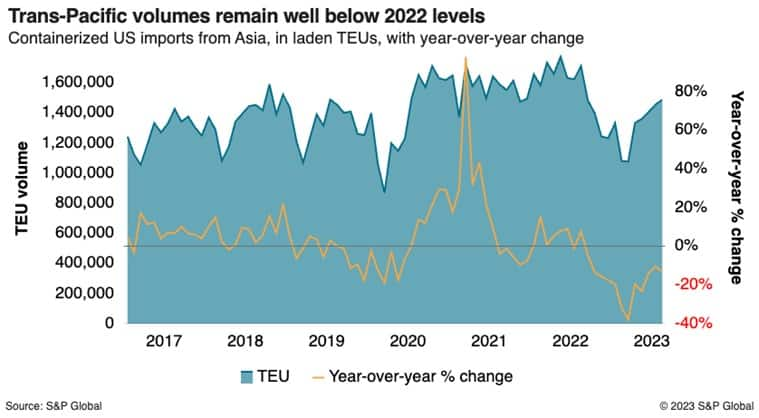

In other words, external conditions are what they are. US containerized imports, which year to date through August were almost exactly at the level of 2019, may or may not bounce back next year due to difficult-to-predict factors as varied as tightening consumer credit, inflation, high mortgage rates or student loans coming due.

But how that translates into pricing and quality of service on the water will be the result of how carriers respond to those market conditions. Flush with cash, it was carriers who splurged on new green tonnage, driving the order book up to nearly 30% of the existing fleet at a time when demand was never going to be sustained at the levels seen in 2021 and 2022 and could remain subdued for another year. And it will be those same carriers who will decide how, and to what extent, to mitigate the impact of overcapacity, including how aggressively to undercut competitors to fill their ships.

That is why as the industry looks toward 2024, when expectations for a recovery are fading fast, the question of how carriers will react is very much a topic of speculation across the industry.

There is a range of possibilities. The opportunity would certainly exist, for example, for the largest carriers to draw down the huge war chests they amassed during the pandemic to wage a ruinous rate war with the goal of driving weaker carriers out of the market. In the annals of container shipping history, such aspirations are hardly unheard of. In an industry with virtually no track record of startup carriers rapidly achieving global scale, taking out a competitor would produce the seemingly not unsatisfying result of further consolidation, strengthening the hand of the surviving liners.

But several Asia-based container shipping sources contacted recently believe that will not happen, at least not soon. Due to consolidation over time, many carriers have fallen out of the top tier and become smaller in their overall share of the market. Therefore, taking them out, if actually achieved, accomplishes little given the costs involved to get the job done.

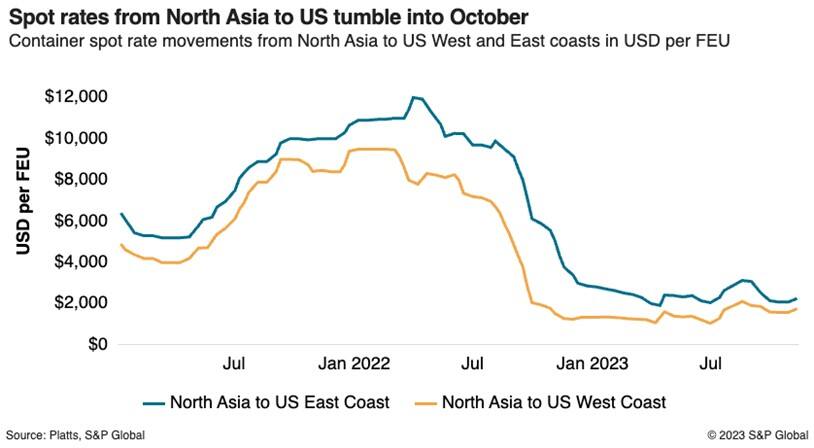

To that point, sources agree that despite hyperventilating headlines proclaiming a rate war earlier this year, it wasn't a rate war in the classic sense that led trans-Pacific spot rates to the West Coast to plummet by more than 80% since early 2022 and about 25% since August, according to Platts, a sister company of the Journal of Commerce within S&P Global.

Rather, it was the market adjusting to the unclogging of ports and a sharp decline in volume — US containerized imports are down 18.7% year to date through August versus 2022 while the vessel backups that idled capacity are gone for the most part. There were few signs of carriers engaging in predatory pricing to fill ships at any price and gain customers and market share at the expense of competitors.

Those are the same factors that will soon wipe out carrier profits and leave the industry in the same, mostly unprofitable, position as it was prior to the pandemic.

"We expect quarterly earnings to continue falling, not only into year-end, but into next year," Jefferies analyst Andrew Lee wrote on Oct. 9.

That informs the prevailing view among Asia-based sources that however inevitably the carriers' pandemic good times might now be fading into history, none has interest in funding the losses that a true predatory rate war would cause. Rather, the carriers still appear to many to be yield-driven, searching for profits however elusive they might be, and reverting to their tried-and-true posture of aggressively controlling costs.

Thus, looking forward to 2024, the market should expect more of the same, namely blank sailings, slow steaming, delayed vessel deliveries where possible and increased scrapping. More aggressive moves — such as parking ships in the Norwegian fjords and diverting Europe-to-Asia ships around the Cape of Good Hope to save Suez Canal fees and absorb capacity — are also possible.

Ocean carriers in the eastbound trans-Pacific say capacity reductions they have implemented on the trade this year are likely to continue at least for the next five months, with US imports expected to remain muted through Chinese New Year in February.

An intense focus on cost, moreover, makes it less likely that certain carriers will go the route of delivering consistent service as that would mean fewer blanked sailings and more capacity that would need to be filled through aggressive rate actions. Bottom line: An all-out war among the carriers is not likely to break out.

*Originally published in the Journal of Commerce on October

12, 2023

Subscribe now or sign up for a free trial to the Journal of Commerce and gain access to breaking industry news, in-depth analysis, and actionable data for container shipping and international supply chain professionals.

Subscribe to our monthly Insights Newsletter

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2focean-carriers-survey-changing-market-and-ponder-next-course-o.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2focean-carriers-survey-changing-market-and-ponder-next-course-o.html&text=Ocean+carriers+survey+changing+market+and+ponder+next+course+of+action+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2focean-carriers-survey-changing-market-and-ponder-next-course-o.html","enabled":true},{"name":"email","url":"?subject=Ocean carriers survey changing market and ponder next course of action | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2focean-carriers-survey-changing-market-and-ponder-next-course-o.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Ocean+carriers+survey+changing+market+and+ponder+next+course+of+action+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2focean-carriers-survey-changing-market-and-ponder-next-course-o.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}