Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Oct 24, 2023

Rising recession risks as eurozone flash PMI falls in October, price pressures ease further

The eurozone economic downturn accelerated at the start of the fourth quarter, according to provisional PMI survey data for October, with private sector output declining at the steepest rate for over a decade if pandemic affected months are excluded. New orders also fell at an accelerating rate, pointing to a worsening demand environment for both goods and services. Companies cut employment as a result, representing the first drop in headcounts since the lockdowns of early 2021, and remained focused on cost-cutting inventory management.

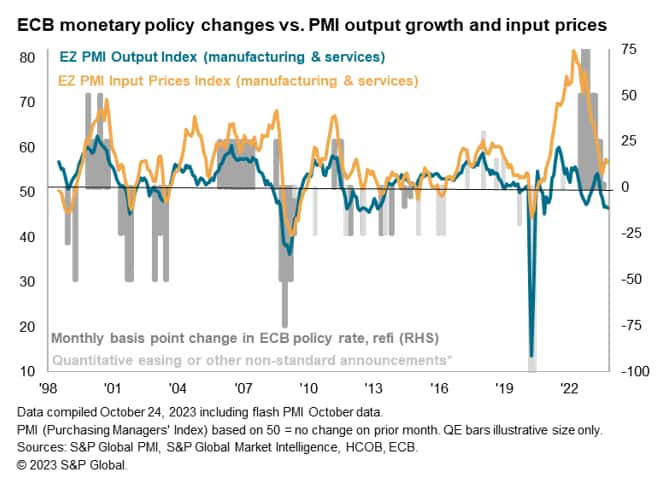

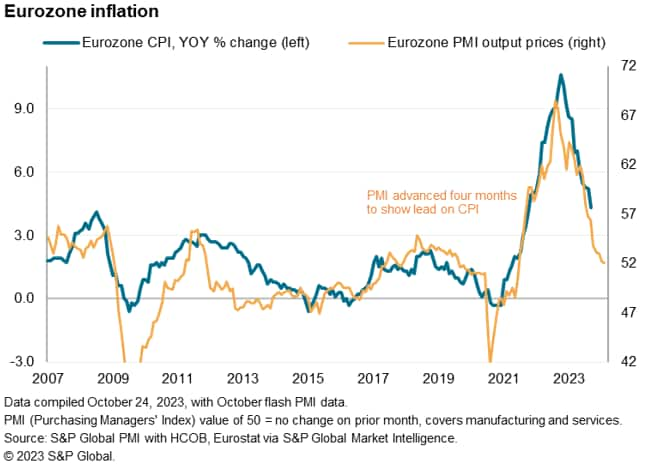

Despite some upward pressure on costs from higher oil prices, the rate of inflation for goods and services moderated slightly in October, down to its lowest since February 2021. An ongoing sharp fall in manufacturing selling prices was accompanied by a moderation in service sector selling price inflation. Overall, the PMI signals a cooling of headline CPI inflation below the ECB's target by early 2024. However, high oil prices pose some upside risks to inflation in the months ahead.

Output and demand

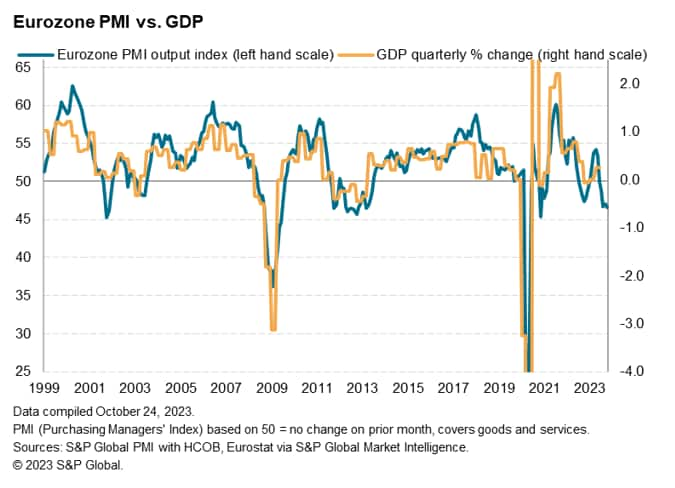

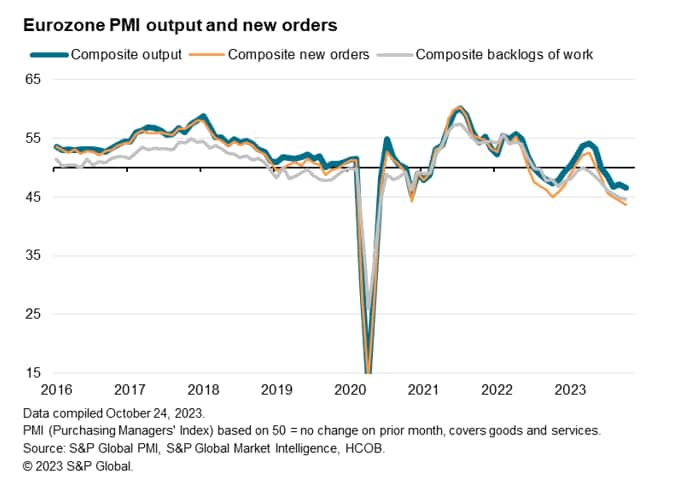

The headline HCOB Flash Eurozone Composite PMI Output Index, compiled by S&P Global and based on approximately 85% of usual survey responses, fell from 47.2 in September to 46.5 in October, signalling a fifth consecutive month of falling business activity and the steepest decline since November 2020. Excluding pandemic months, the fall in activity was the sharpest since March 2013.

Historical comparisons indicate that the current level of the PMI is broadly consistent with eurozone GDP falling at a quarterly rate of approximately 0.4% at the start of the fourth quarter, having signalled a 0.3% contraction in the third quarter.

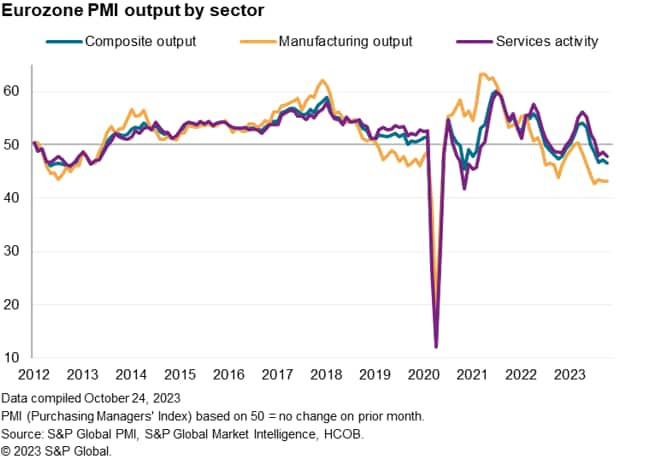

A broad-based downturn was again evident, as a seventh successive month of falling output in the manufacturing sector was accompanied by a third month of contracting service sector activity.

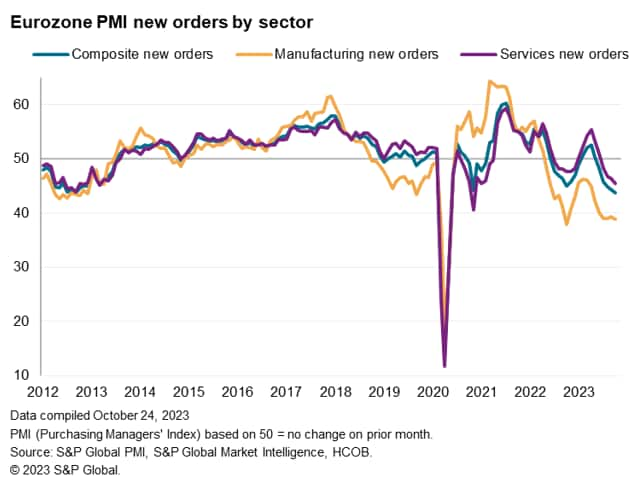

The goods-producing sector continued to report the steeper rate of contraction, the pace of output decline unchanged on the marked pace seen in September to indicate that factories remain in the deepest downturn since 2009 barring the early pandemic lockdowns. With the exception of a brief period of growth during the opening quarter of 2023, euro area manufacturing output has decreased continuously since the middle of 2022, reflecting 18 months of continuously falling inflows of new orders into the sector. New orders received by manufacturers fell sharply again in October, dropping at a slightly faster rate than September to sustain one of the sector's steepest downturns in demand since 2009.

Service sector activity meanwhile contracted at an accelerating rate in October, dropping at a rate not seen since early-2021 and since May 2013 if the height of the pandemic is excluded. Recent months have seen the service sector's performance alter markedly, as a strong resurgence of activity earlier in the year has moved into reverse, in part reflecting a cooling of a post-pandemic surge in spending on travel and recreation. Measured overall, new business received by service providers fell for a fourth straight month in October, the rate of decline accelerating to the fastest since January 2021.

Measured across goods and services, the resulting drop in new orders was the largest since May 2020 and, if early pandemic months are excluded, since May 2009. The drop in orders was also steeper than the reported decline in output, meaning companies once again relied on backlogs of previously-placed orders to help sustain activity levels. Backlogs of orders were consequently depleted at a rate not seen since June 2020, dropping at slightly faster rates in both manufacturing and services.

Employment, inventories and purchasing

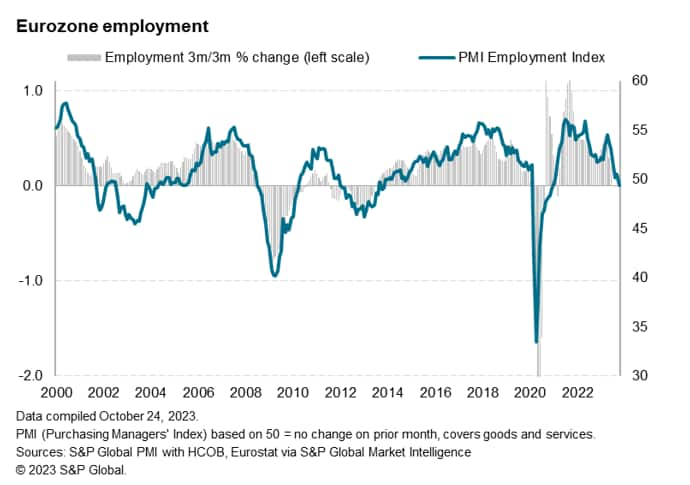

The downturn in new orders and the accelerated depletion of backlogs of orders prompted firms to reduce employment for the first time since January 2021. A fifth consecutive month of job losses in the factory sector saw manufacturing headcounts drop at the sharpest rate since August 2020, while hiring came close to stalling in the service sector.

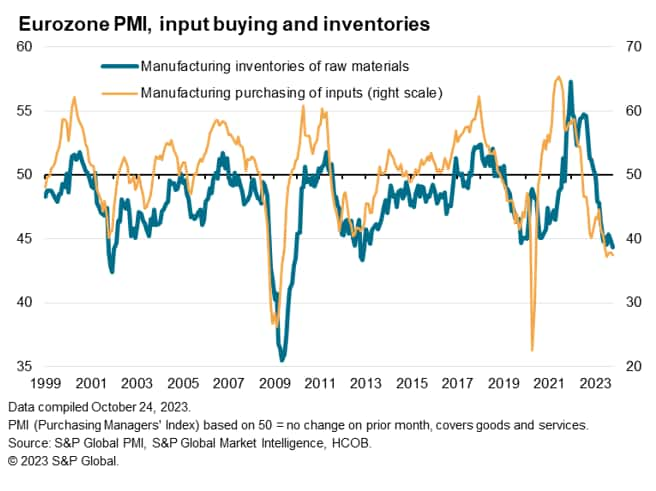

Input buying by manufacturers was likewise further pared back, dropping at one of the sharpest rates since April 2009 if the early COVID-19 lockdown months are excluded. The cut to buying activity resulted in the steepest fall in inventories of purchases since December 2012. A growing focus on costs meant stocks of finished goods were also lowered further in October, dropping at the sharpest pace since August 2021.

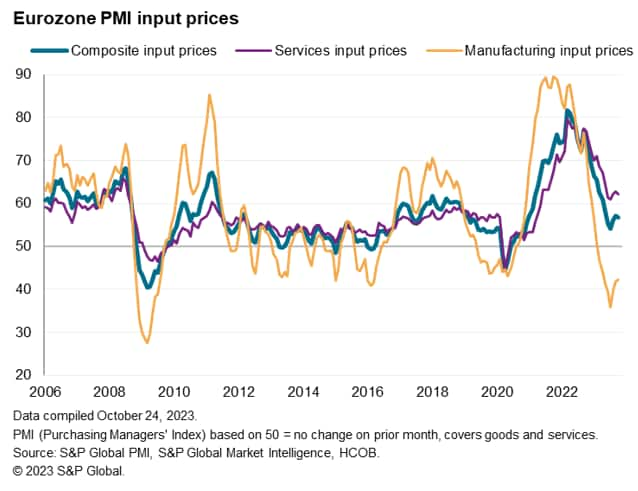

Prices continue to cool

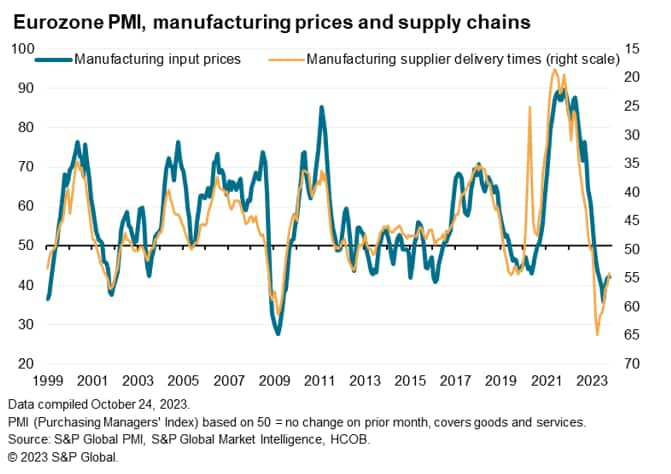

Reduced demand for inputs meant vendor lead times improved for a ninth consecutive month, with faster deliveries accompanied by a further cooling of supply chain price pressures. Despite reports of higher oil prices having added to firms' costs over the month, the average cost of inputs into factories fell sharply in October amid discounting as supply exceeded demand. Manufacturing input prices were down for an eighth consecutive month, although the rate of decline eased for a third month in a row.

Service sector input costs were also buoyed by higher fuel prices, though nonetheless rose at a slightly reduced rate compared to September. The overall rate of increase remained elevated, however, often linked to higher wage rates amid the rising cost of living. Although service sector cost inflation has fallen sharply compared to a year ago, the rate of inflation remains higher than at any time in the pre-pandemic period since 2008.

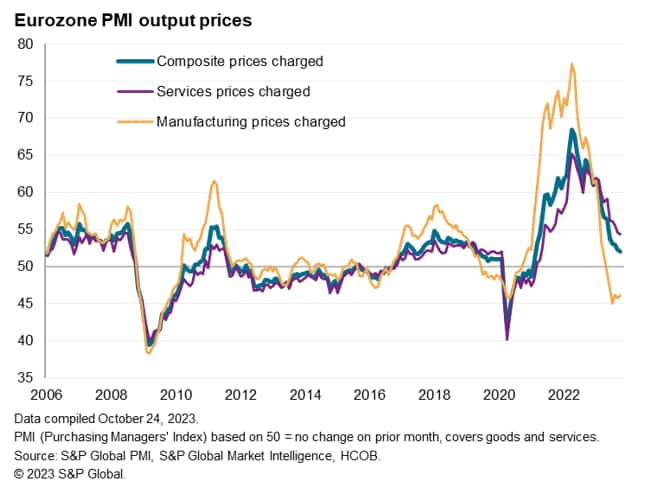

Encouragingly, average prices charged for goods and services rose at a marginally weaker rate in October, the rate of inflation edging down to its lowest since February 2021 and notably continued to run below the average seen in the three years preceding the pandemic. A further marked fall in manufacturing selling prices was accompanied by a cooling of service sector inflation to the lowest since May 2021.

Looking at the inference for inflation, the overall signal from the PMI selling price gauge is for CPI inflation to continue to moderate in the coming months, dropping from its current 4.3% pace (as per September) to below the ECB's target of 2% in early 2024. One caveat is that rising tensions in the Middle East pose an upside risk to oil prices and the possibility of higher inflation if elevated high oil prices are sustained.

Access the full press release here.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Tel: +44 207 260 2329

© 2023, S&P Global. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2frising-recession-risks-as-eurozone-flash-pmi-falls-in-october-price-pressures-ease-oct23.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2frising-recession-risks-as-eurozone-flash-pmi-falls-in-october-price-pressures-ease-oct23.html&text=Rising+recession+risks+as+eurozone+flash+PMI+falls+in+October%2c+price+pressures+ease+further+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2frising-recession-risks-as-eurozone-flash-pmi-falls-in-october-price-pressures-ease-oct23.html","enabled":true},{"name":"email","url":"?subject=Rising recession risks as eurozone flash PMI falls in October, price pressures ease further | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2frising-recession-risks-as-eurozone-flash-pmi-falls-in-october-price-pressures-ease-oct23.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Rising+recession+risks+as+eurozone+flash+PMI+falls+in+October%2c+price+pressures+ease+further+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2frising-recession-risks-as-eurozone-flash-pmi-falls-in-october-price-pressures-ease-oct23.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}