Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Aug 05, 2020

The worst quarter in trade on record, signs of a weak recovery in China and a positive trend in PMI new export orders readouts for all top economies

Key points:

- China mainland is the only top economy showing signs of recovery in Q2 2020 both in exports and imports

- Overall, the Q2 of 2020 is the worst quarter in global trade on record

- Year-on-year changes in exports in May 2020 were negative for all reporting states including China (-3.3%), Brazil (-14.2%), South Korea (-23.7%), Japan (-26.0%), Russia (-34.8%), United States (-36.3%), UK (-36.6%), EU external trade (-37.7%) and Canada (-41.0%)

- Several countries have already reported trade data for June 2020, Brazilian exports went down by 2.7% year-on-year, the situation is much worse for South Korea (-10.9%) and Japan (-26.1%), Chinese exports went up year-on-year but only by 0.3% which is, however, a clear improvement on the preceding months, taking the whole Q2 2020 Chinese exports are above by 0.1% over the result

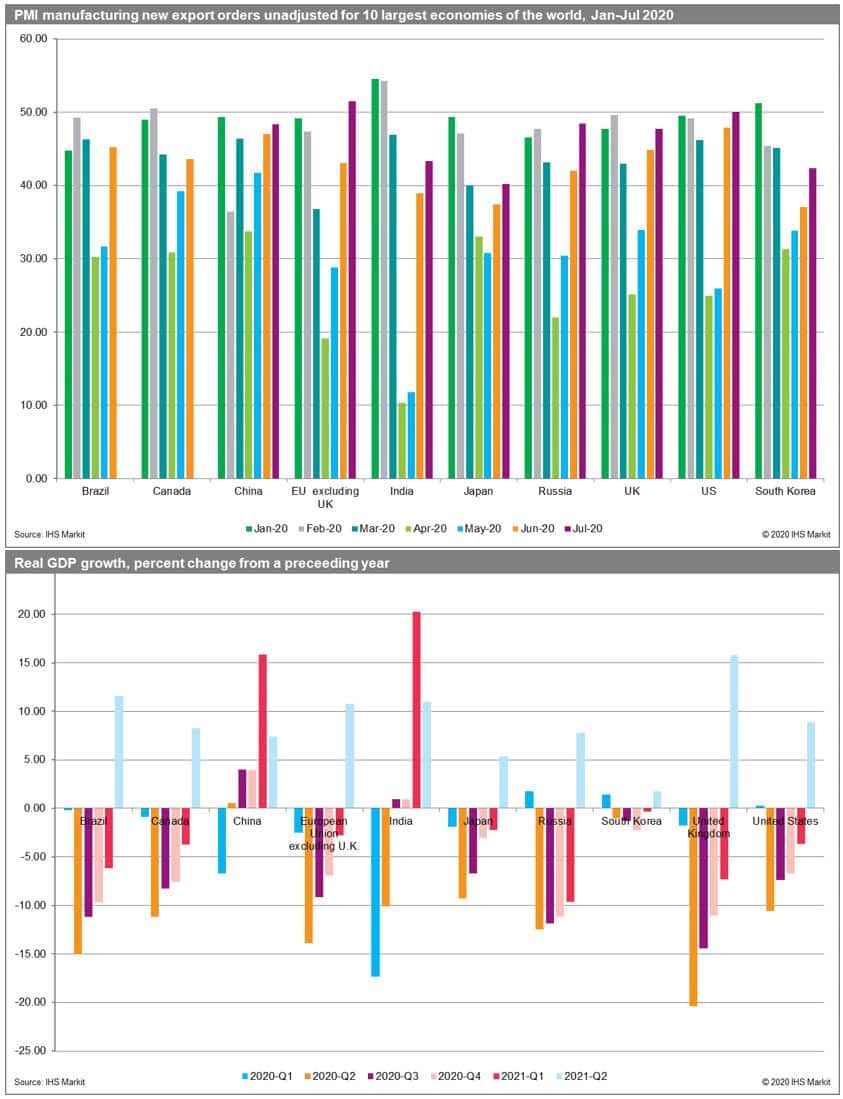

- PMI new export orders for manufacturing is above 50.0 points for the US and the EU excluding the UK providing some optimism for Q3

Key developments in trade in Q2 2020

- China mainland is the only top economy showing signs of recovery in Q2 2020 (with positive changes both in exports and imports)

- Year-on-year changes in exports in May 2020 were negative for all reporting states including China (-3.3%), Brazil (-14.2%), South Korea (-23.7%), Japan (-26.0%), Russia (-34.8%), United States (-36.3%), UK (-36.6%), EU external trade (-37.7%) and Canada (-41.0%)

- May 2020 brought about a deterioration of the situation from April 2020 for all the states apart from South Korea with the most adverse shifts in the US, Japan, and the EU as well as China

- Year-on-year changes in imports in May 2020, similarly to exports, are negative for all reporting states and range from -10.5% in Brazil, -15.7% in Russia and - 16.4% in China to -25.7% in the US, -32.0% in the EU external imports, -33.9% in the UK, and a massive -39.2% contraction in the case of Canada; in comparison to April 2020 the situation deteriorated in all the states apart from Brazil, Russia, and the UK with Japan being affected the most

- Four out of top ten world economies, have already reported data for June 2020, Brazilian exports went down by 2.7% year-on-year, the situation is much worse for South Korea (-10.9%) and Japan (-26.1%), Chinese export went up year-on-year but only by 0.3% which is, however, a clear improvement on May results

- From quarterly perspective exports of all the top ten countries decreased year-on-year in Q1 2020 ranging from -1.8% for South Korea and Canada to -12.8% in India and -13.4% in China, the Q2 results are worse for most of the states that have already reported the complete data (Japan -23.7%, South Korea -20.3%, Brazil -8.6%) apart from China (+0.1%) with the level of exports more or less the same as in the preceding year indicating an ongoing recovery

- India has only now reported the trade data for March 2020, as could have been expected due to lockdowns implemented the exports collapsed by more than 1/3 (-34.6%) year-on-year - it was the most adverse effect reported in March by all the top 10 economies

Prospects for the forthcoming months

- The reaction in trade so-far is consistent with the escalating global COVID-19 pandemic and steps taken by individual countries (or group of countries) in controlling or mitigating it

- On 3 August 2020 WHO reported 17,918,582 cases globally and 686,703 deaths so far, the number of new cases reported globally is now close to 260,000 and is not showing signs of deceleration

- The impact on global trade and global economy will depend on the duration, severity and the spatial distribution of the pandemic, with several scenarios of recovery still possible, and critically depends on the development of a successful vaccine

- Unfortunately, the threat of the second wave of the pandemic is increasing with some states already re-imposing strict overall or partial (regional) lockdowns upon the signs of the second-wave and some countries are still unable to deal efficiently with the first wave; the potential second wave in autumn 2020 can have drastic consequences for the global economy postponing the expected recovery to next year, some economist are pointing to a potential change in the shape of the crisis from the V to W pattern with OECD speaking of additional decline on top of the existing one in the double-hit scenario, having at this stage the same likelihood as the single-hit scenario

- PMI new export orders is a very good predictor of the changes in trade flows in the forthcoming months, the manufacturing PMI new exports orders readouts (unadjusted) by IHS Markit for July 2020 are above of 50.0 points for EU and the United States, and values close to 50.0 points for China, Russia, and the UK, the lowest level has been recorded for Japan (40.2 points);

- The trend in the PMI is clear and consistent within the Q2 of 2020 showing a gradual improvement in market confidence, which allows being more optimistic for the third quarter of this year unless a second wave of the pandemic will adversely affect in the months to come

- The most recent GDP growth forecasts from IHS Markit Comparative World Overview (published on 15 July 2020) point to a recession in most of the states throughout 2020 and Q1 of 2021, apart from China mainland (recovery already in Q2 2020) and India (recovery in Q3 2020). The worst affected countries (regions) in Q2 2020 are forecasted to be the UK, EU, and the US

- The recession is forecasted to last throughout Q1 2021 in most of the states with a significant upturn in the case of China and India only (consistently with the forecasts for the remainder of this year), a stronger recovery in real GDP growth rates is expected to spread to other economies only later in 2021, the forecast, unfortunately, depends critically on the ability to deal with the potential second/third waves of the pandemic, uncertainty levels are still high

- Taking into account the multiplier effect between GDP growth and trade growth in times of crisis exceeding the value of 3.0 we can expect the contraction of trade in most of the top economies to last through 2020 and Q1 2021 and to take more than two-digit values year-on-year

The background

- The COVID-19 pandemic is the worst global health crisis in a century and potentially without precedent if we take the globalized nature of the current economy. The pandemic has already triggered a severe economic recession, the first months of 2020 brought about a collapse in trade (year-on-year) due to the spread of the pandemic and resulting lockdowns and disruption in global value chains

- The first top economy adversely affected was China followed by Japan and other East Asian countries and India, the situation deteriorated in most of the top economies in March or in April in line with the spreading pandemic

- The contraction in trade continues well into Q2 with most countries reporting massive declines, without any doubt it will be the worst year on record for global trade and potentially the worst quarter on record as well

- The outbreak of COVID-19 proves to be the largest black-swan in a century with an extreme impact on the global economy; we are dealing with the largest contraction of global trade since the Second World War, far larger than the effects of the global financial crisis in 2008-09 or any other recent outbreak (e.g. SARS, Ebola or MERS)

This column is based on data from Maritime & Trade Global Trade Atlas data and other resources of IHS Markit.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fthe-worst-quarter-in-trade-on-record.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fthe-worst-quarter-in-trade-on-record.html&text=The+worst+quarter+in+trade+on+record%2c+signs+of+a+weak+recovery+in+China+and+a+positive+trend+in+PMI+new+export+orders+readouts+for+all+top+economies++%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fthe-worst-quarter-in-trade-on-record.html","enabled":true},{"name":"email","url":"?subject=The worst quarter in trade on record, signs of a weak recovery in China and a positive trend in PMI new export orders readouts for all top economies | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fthe-worst-quarter-in-trade-on-record.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=The+worst+quarter+in+trade+on+record%2c+signs+of+a+weak+recovery+in+China+and+a+positive+trend+in+PMI+new+export+orders+readouts+for+all+top+economies++%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fthe-worst-quarter-in-trade-on-record.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}