Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Jul 10, 2023

US Weekly Economic Commentary: Resilience, stubborn inflation, more rate hikes

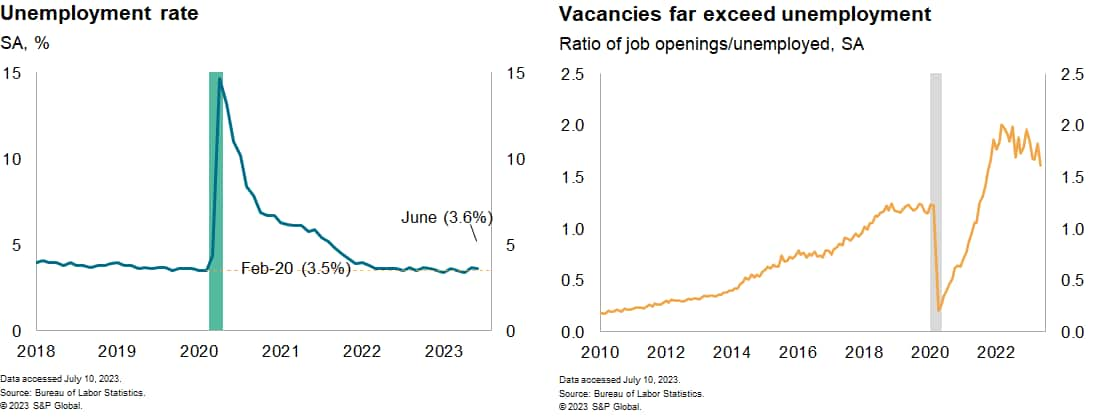

Labor market indicators, including Friday's employment report for June, the Job Openings and Labor Turnover Survey (JOLTS), and initial claims for unemployment insurance, on balance show a labor market that remains very tight — with a significant excess of demand over supply — and only hints that conditions are loosening.

Employment at nonfarm establishments rose 209 thousand in June, leaving the average gain in payrolls over the most recent three months at a robust 244 thousand. This is well above the roughly 100 thousand monthly gain that would be consistent with no material change in labor-market tightness, assuming no change in the labor force participation rate. The unemployment rate ticked back down to 3.6%.

The JOLTS data did show a roughly 600 thousand decline in private-sector job openings in May from an elevated April reading. Still, the job openings rate (job openings as a percent of employment plus openings) remains quite elevated, near 6% compared to 4.2% in 2019, suggestive of continued labor-market tightness.

Average hourly earnings (AHE) have recently accelerated, particularly sharply in manufacturing. The three-month annualized change in manufacturing AHE in June rose to 6.4%, continuing an uneven climb from a 3.7% rise over the 12 months of 2022. Overall AHE growth is also showing signs of turning upward again after a year-long slide.

This, of course, is going in exactly the opposite direction from what would be required to see core price inflation decline sustainably to the Fed's 2% target, i.e. increases in the range of 3%-3½%. We continue to expect that a material loosening of labor-market tightness, including a rise in the unemployment rate to over 4.5%, will be needed to get wage and price inflation back under control. That will likely require some additional tightening of financial conditions to slow aggregate spending and to ease demand relative to supply across product and labor markets.

The rise in interest rates over the last several weeks and in the last few days suggest that financial markets are getting the message. The minutes from the June policy meeting of the Federal Open Market Committee had a hawkish tilt, supporting our forecast and market expectations that the Fed will raise the policy rate 25 basis points (one-quarter percentage point) at its July meeting. We expect another rate hike in November.

This week's economic releases:

- Consumer price index (July 12): We estimate that the overall CPI rose 0.3% in June, as did the core CPI, which excludes the direct effects of food and energy prices. The estimated June increases would leave the overall CPI up 3.2% over the twelve months ending in June and the core CPI up 5.0% over the same period. The latter would be the lowest reading since late 2021 but still intolerably high from the perspective of the Federal Reserve.

- The University of Michigan Consumer Sentiment Index (July 14): We estimate the index rose 0.9 point to 65.3 in the preliminary July reading as inflation continues to ease.

- Producer price index (July 13): We estimate that the PPI for final demand was unchanged in June, while the core PPI, which excludes the direct effects of changes in prices for food and energy, rose 0.1%.

Learn more about our economic data and insights

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fus-weekly-economic-commentary-resilience-more-rate-hikes.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fus-weekly-economic-commentary-resilience-more-rate-hikes.html&text=US+Weekly+Economic+Commentary%3a+Resilience%2c+stubborn+inflation%2c+more+rate+hikes+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fus-weekly-economic-commentary-resilience-more-rate-hikes.html","enabled":true},{"name":"email","url":"?subject=US Weekly Economic Commentary: Resilience, stubborn inflation, more rate hikes | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fus-weekly-economic-commentary-resilience-more-rate-hikes.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=US+Weekly+Economic+Commentary%3a+Resilience%2c+stubborn+inflation%2c+more+rate+hikes+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fus-weekly-economic-commentary-resilience-more-rate-hikes.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}