Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Mar 07, 2024

Week Ahead Economic Preview: Week of 11 March 2024

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

US CPI, UK monthly output and labour data to watch

US inflation and activity data will be some of the highlights in the week, while the UK also releases monthly output and labour market reports. Additionally, final GDP and inflation data will be due from major developed economies alongside a series of tier-2 data across the globe. S&P Global also releases key findings from their latest Business Outlook surveys for major developed economies, and the US Investment Manager Index on Tuesday. This will be followed by the GEP Global Supply Chain Volatility Index.

The key economic data of the week will be February's US CPI, which will be closely watched to help shape monetary policy and growth expectations. While some stickiness may be anticipated according to consensus expectations, further easing of inflationary pressures should not be ruled out in the coming months given the signals from PMI prices data, which could be supportive of eventual rate cuts. That said, the market caution observed ahead of the prior jobs report may well be seen again ahead of the next US CPI update.

Insights into US investor sentiment will also be provided by the March S&P Global Investment Manager Index due on Tuesday. Indications as to whether the IT sector remains among the most favoured will be especially watched, given increasing uncertainty around the sector following the spectacular run tech so far this year. Key drivers of US equity returns will also be scrutinised after February's survey revealed that central bank policy was perceived to be a drag on equity returns midway into Q1. Any changes to perceptions on US and global macroeconomic environments will also be assessed given the recent improvements observed through the PMI data (see box).

Finally, the UK releases monthly output and employment data. While an intensification of price pressures, according to PMI data, may well be at the top of concerns, the extent to which the ongoing expansion in the UK is lop-sided will be assessed with the official growth and employment figures. A stronger service sector performance, across both business activity and employment gauges, has been highlighted by PMI figures in 2024 so far. This is important as it may further complicate the outlook for monetary policy in the UK.

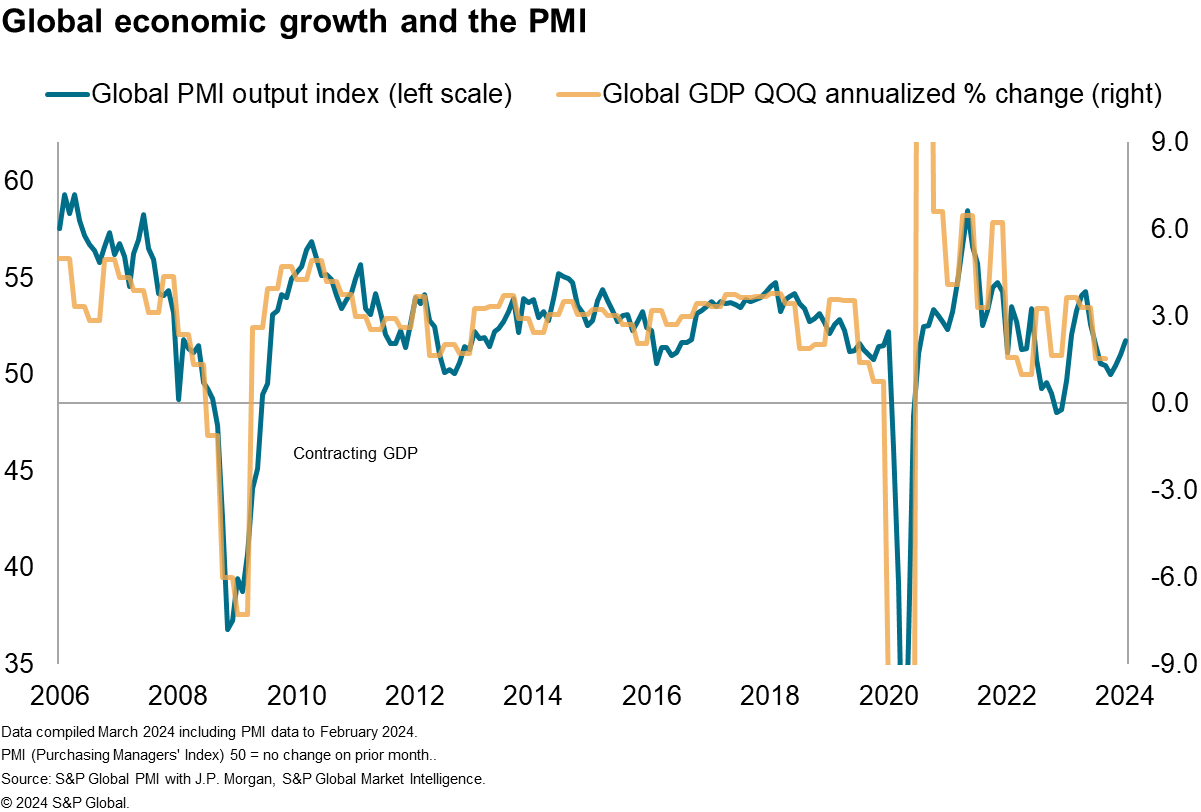

Global growth hits eight-month high in February

Worldwide business activity growth reached an eight-month high in February, according to the latest Global PMI data compiled by S&P Global.

At 52.1, up from 51.8 in January, the headline PMI, covering manufacturing and services across over 40 economies and sponsored by JPMorgan, rose for a fourth consecutive month, signalling accelerating growth.

Although the PMI remains below the survey's long-run average of 53.2 and is broadly consistent with annualized quarterly global GDP growth of approximately 2% (below the pre-pandemic ten-year average of 3.0%), the gathering upturn allays concerns of a global recession after the slowdown seen late last year.

Stronger demand conditions supported the latest acceleration in growth, with a steady upturn in demand for services accompanied by the first rise in new orders for goods in 20 months. Further modest jobs gains were also encouraged by the upturn in orders, though the rate of job creation remained mild.

That said, average prices charged for goods and services globally rose at a faster rate in February. Although the pace of increase remained among the lowest seen since mid-2021 and well down on the strong rates seen in 2022 and early-2023, services price inflation remained especially elevated by pre-pandemic standards. Meanwhile, manufacturing selling prices continued to rise modestly in the latest survey period.

Key diary events

Monday 11 Mar

Indonesia Market Holiday

Japan GDP (Q4, final)

China (mainland) National People's Congress

Turkey Unemployment Rate (Jan)

Switzerland Consumer Confidence (Feb)

United Kingdom KPMG / REC Report on Jobs* (Feb)

Tuesday 12 Mar

Japan PPI (Feb)

Australia Building Permits (Jan, final)

Philippines Trade (Jan)

Malaysia Industrial Production (Jan)

China (mainland) M2, New Yuan Loans, Loan Growth (Feb)

Germany Inflation (Feb, final)

Turkey Industrial Production (Jan)

United Kingdom Labour Market Report (Feb)

Brazil Inflation (Feb)

India Industrial Production (Jan)

India Inflation (Feb)

Mexico Industrial Production (Jan)

United States CPI (Feb)

S&P Global Business Outlook* (Feb)

S&P Global Investment Manager Index* (Mar)

Wednesday 13 Mar

South Korea Unemployment (Feb)

United Kingdom monthly GDP, incl. Manufacturing, Services and

Construction Output (Jan)

United Kingdom Trade (Jan)

Eurozone Industrial Production (Jan)

GEP Global Supply Chain Volatility Index* (Feb)

Thursday 14 Mar

India WPI (Feb)

Spain Inflation (Feb, final)

Hong Kong SAR Industrial Production (Q4)

Brazil Retail Sales (Jan)

Brazil Inflation (Feb)

United States PPI (Feb)

United States Retail Sales (Feb)

United States Initial Jobless Claims

United States Business Inventories (Jan)

Friday 15 Mar

China (mainland) House Price Index (Feb)

Singapore Unemployment (Q4, final)

Indonesia Trade (Feb)

India Trade (Feb)

Germany Wholesale Prices (Feb)

France Inflation (Feb, final)

Italy Inflation (Feb, final)

Italy Retail Sales (Jan)

United States Import and Export Prices (Feb)

United States Industrial Production (Feb)

United States UoM Sentiment (Mar, prelim)

* Access press releases of indices produced by S&P Global and relevant sponsors here.

What to watch in the coming week

Americas: US CPI, retail sales, industrial production data

The highlight of the week will be Tuesday's US CPI data for insights into inflation conditions in the US. Consensus expectations point to some stickiness from January at the time of writing, which should not come as a surprise given leading indications from PMI data. That said, the headline CPI is expected to descend further in the coming months to around the 2% level, according to PMI price indices. Additionally, monthly activity data, including retail sales and industrial production figures, will be due on Thursday and Friday respectively. This comes after the S&P Global US Manufacturing PMI rose to the highest since July 2022 with manufacturing output growth notably reviving in February. Service sector growth was also sustained midway into Q1.

EMEA: UK monthly output, labour market report, eurozone industrial production, trade and inflation data

The UK updates January output data, including manufacturing, services and construction output. The PMI data suggested that the UK economy expanded in January and February. Notably, with growth momentum having accelerated midway into the first quarter, this is indicative of GDP growing at a quarterly rate of just less than 0.3% in Q1.

Additionally, January's UK labour market report will be watched after the latest KPMG and REC UK Report on Jobs survey showed that uncertainty around the economic outlook continued to impact hiring decisions at the start of 2024. A February update of the report will also be due at the start of the week after PMI employment data showed jobs growth slowed in the month.

The eurozone also updates industrial production, trade and final inflation figures in the week.

APAC: Japan GDP, India industrial production, Indonesia trade

In APAC, besides Japan's final Q4 GDP reading, we will also see various tier-2 data released around the region. India's industrial production figures will be a notable release given the outperformance of the manufacturing sector, as seen via the HSBC India Manufacturing PMI.

US Investment Manager Index and supply chain volatility

Risk sentiment changes, key market drivers and sector preferences among US investors will be assessed with the March iteration of the Investment Manager Index, especially after improvements were observed with respect to global and US macroeconomic conditions in the most recent PMI data.

This will be followed by the GEP Global Supply Chain Volatility Index, which will shed light on latest supply chain conditions on Wednesday.

© 2024, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fweek-ahead-economic-preview-week-of-11-march-2024.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fweek-ahead-economic-preview-week-of-11-march-2024.html&text=Week+Ahead+Economic+Preview%3a+Week+of+11+March+2024+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fweek-ahead-economic-preview-week-of-11-march-2024.html","enabled":true},{"name":"email","url":"?subject=Week Ahead Economic Preview: Week of 11 March 2024 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fweek-ahead-economic-preview-week-of-11-march-2024.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Week+Ahead+Economic+Preview%3a+Week+of+11+March+2024+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fweek-ahead-economic-preview-week-of-11-march-2024.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}