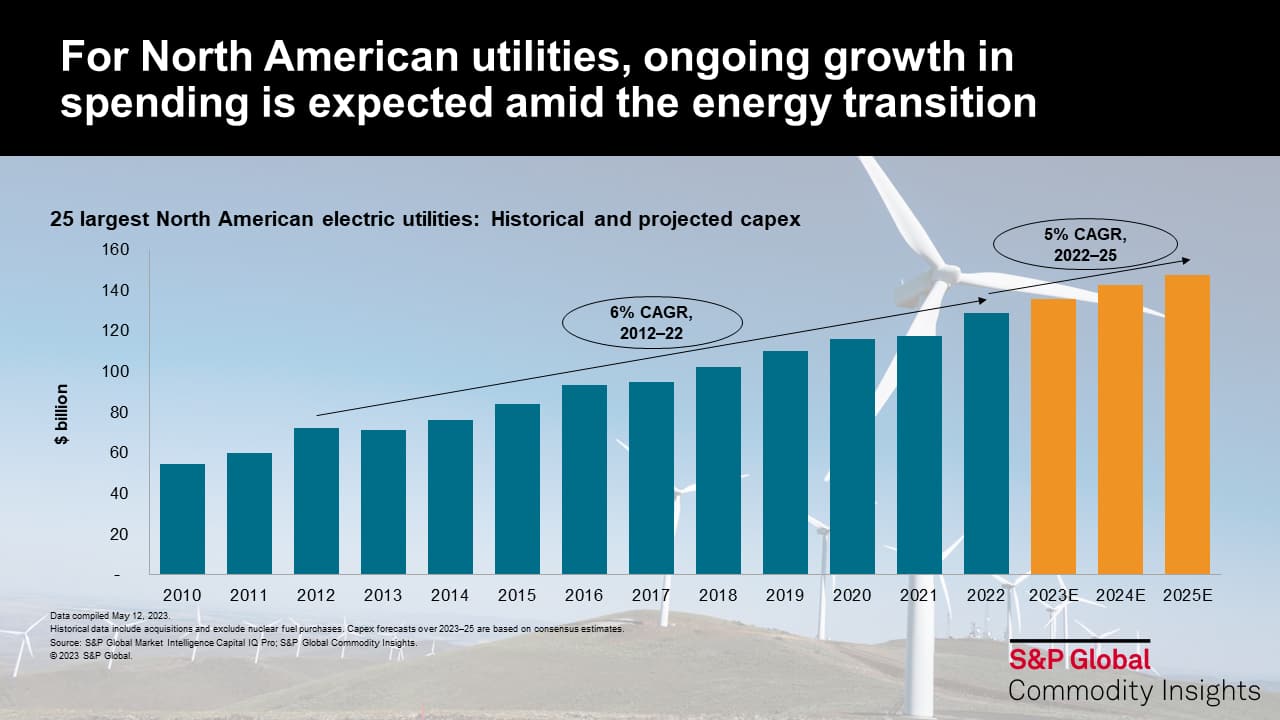

North American power: Following a decade of steady spending increases, further capex growth is expected in the medium term

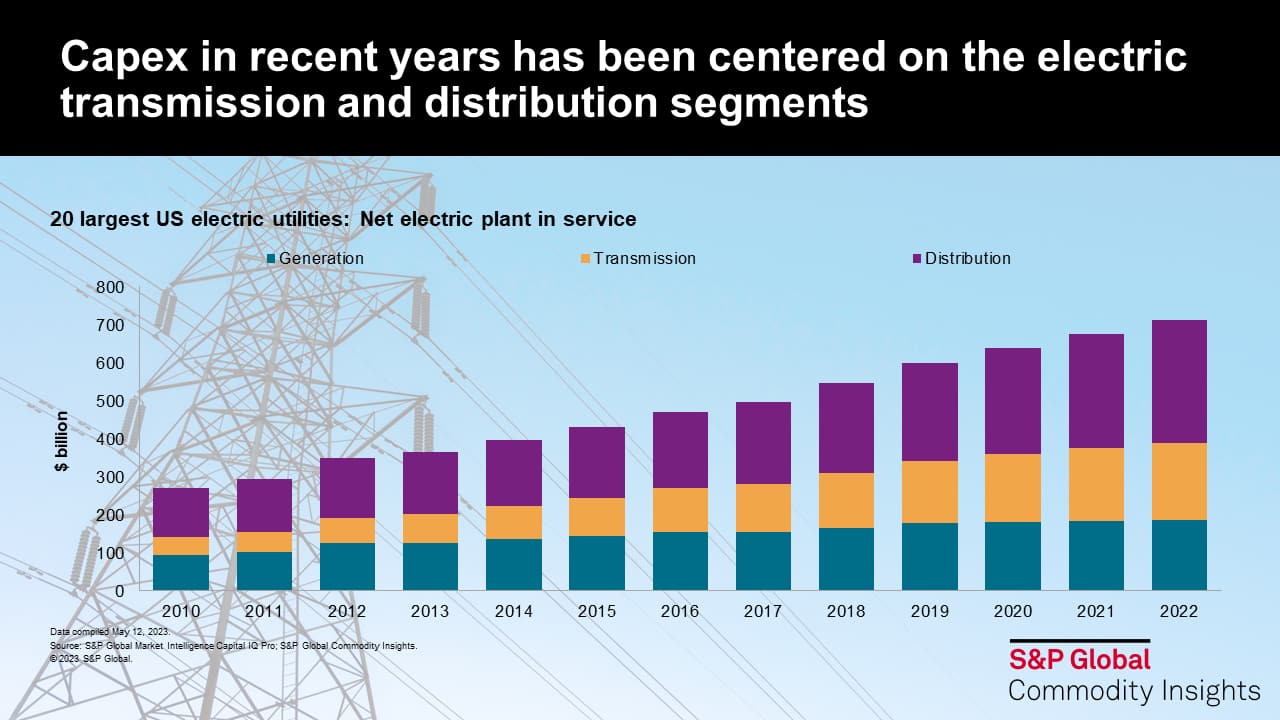

Spending from this peer group remains centered on electric transmission and distribution, amid efforts to increase grid reliability, resilience, and efficiency, and incorporate new sources of supply

An examination of the growth in asset bases for these companies highlights where this spending has been focused. In aggregate for the 20 US-based utilities, net electric plant in service (total plant in service, less accumulated depreciation) has increased at a 7% CAGR since 2012. Transmission and distribution have accounted for the bulk of this increase, rising at CAGRs of 12% and 7%, respectively, during that time. In addition to responding to customer growth, investment in these areas has been focused on enhanced reliability and resilience (including through replacement and upgrading of aging assets, as well as infrastructure hardening), integrating growing renewable sources of supply, and grid modernization. Meanwhile, net generation plant in service from this group of companies has increased at a slower 4% CAGR during the same time.

Looking ahead, this spending is expected to grow further. Current consensus estimates (per data from S&P Global Market Intelligence Capital IQ Pro) point to overall capex from this group of companies rising at a 5% CAGR over 2022-25. Consistent with the recent trend, company guidance points to the majority of this spending being allocated to electric transmission and distribution, with much of the remaining spending centered on generation—including renewables additions, as several of these companies target further decarbonization of their portfolios. In line with this rising capex, these companies are generally targeting medium-term rate base growth at a 6-8% compound annual rate, with the objective of supporting ongoing earnings growth—an attribute which currently represents a core driver of equity market valuations.

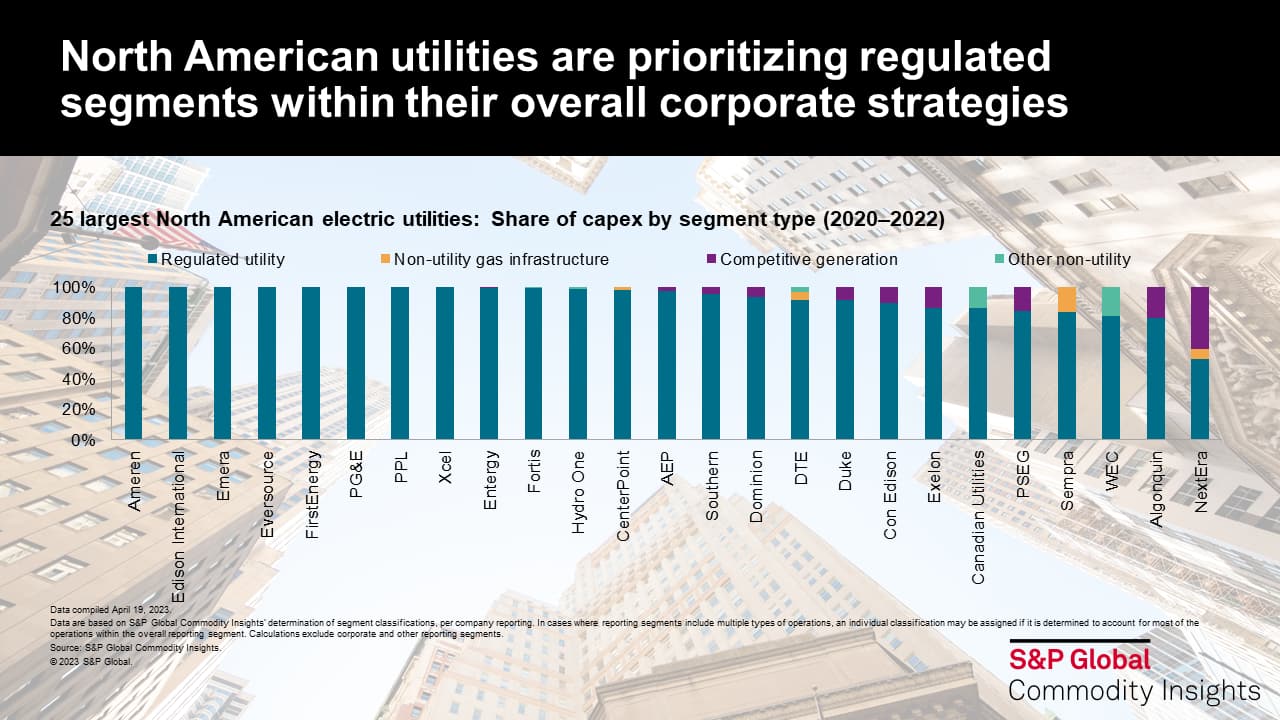

The ongoing industry shift toward regulated segments can support stability of performance, but reduces the opportunity for strategic differentiation

While the trend toward higher capex has been consistent over the past decade, the composition of this spending has shifted. In particular, investment from North American electric utilities has become increasingly centered on regulated opportunities, as companies increase their emphasis on more stable business lines. This approach is aimed at generating greater stability and predictability of earnings and returns-consistent with the traditional capital markets view of utilities as a defensive sector. Accordingly, for the peer group of 25 companies, almost 90% of capex over the past three years has been centered on regulated segments. Looking ahead, this share is expected to rise further, driven by recently announced (including divestitures by Consolidated Edison and AEP of their nonregulated renewables portfolios) or proposed (such as Duke Energy, which expects to complete the sale of its Commercial Renewables portfolio in the second half of 2023) sales or separations of nonregulated portfolios. Meanwhile, other companies (such as Dominion Energy) have indicated plans to reduce or eliminate investment within their nonregulated renewables segments. The result of this trend has been greater uniformity of portfolios across the peer group, which in turn has reduced the ability for companies to differentiate themselves with investors via portfolio strategies—leading them instead to increasingly compete on the basis of financial and operational performance.

Learn more about our Global Power and Renewables service.

Chris DeLucia is a director at S&P Global Commodity Insights with the Global Power and Renewables team, where he focuses on company strategies and competitive dynamics within the power and renewables segment.

Posted on 16 May 2023

This article was published by S&P Global Commodity Insights and not by S&P Global Ratings, which is a separately managed division of S&P Global.