Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Oct 02, 2020

Daily Global Market Summary - 2 October 2020

President Trump's Twitter announcement that he and the first lady tested positive for COVID-19 triggered an uptick in volatility across global markets within seconds of the tweet. Several APAC equity markets were closed for market holidays, but the major markets that were open closed lower on the day. Both European and US equity markets closed mixed, with US small caps ending the day higher and tech sharply lower. US government bonds ended the day lower, despite being higher on the day until the US equity market opened. iTraxx and CDX indices were both close to unchanged on the day, while oil closed sharply lower for the third time this week. The US non-farm payroll headline number came in below consensus, but still reported an encouraging 661K jobs were added and unemployment declined to 7.9% in September.

Americas

- US President Donald Trump announced on 1 October that he has tested positive for COVID-19, along with his wife Melania Trump, and that he will be self-isolating for an unspecified amount of time. The statement comes only 32 days prior to the 3 November election date, which is extremely unlikely to be moved because of existing congressional statutes. According to the White House, the president will continue working throughout his illness, but Vice-President Mike Pence will step in as his surrogate for scheduled appearances. According to government statements, the president is not currently experiencing adverse symptoms. However, because of his weight and age, he remains in a high-risk category for a severe reaction. The immediate political impact will be to force the president to cancel his campaign rallies (at least temporarily) and, depending upon his condition, his ability to participate in the next presidential debate on 15 October may be affected. The national discussion will also move away from the president's 29 September debate performance back to the COVID-19 virus, with the public largely viewing his handling of the pandemic negatively, and this will undermine the health arguments that Trump has used against former vice-president Joe Biden's competence to hold office and his claims that the nation has "rounded the corner" on handling the pandemic. Conversely, as seen in other countries where leaders have contracted the illness, some members of the public are likely to sympathize with Trump's condition. Recent polling suggests that approximately 85% to 90% of the US public are already sure of their voting choice. Consequently, if the president recovers quickly, the overall implication of his illness for the outcome of the election race is likely to be limited. With respect to governance, Trump's illness is likely to stall some Republican governors from fully reopening their economies. If the virus spreads throughout the West Wing, ongoing international negotiations or policy enactment will be delayed. If the president were to die or become completely incapacitated, the Republicans would almost certainly quickly nominate Vice President Mike Pence to replace him as the party nominee. A semi-incapacitated state would present more problems as it would require Trump to temporarily relinquish power or for a majority of the cabinet and the vice-president to vote to remove him. It would also raise questions among the public as to the president's state of health prior to the election. (IHS Markit Country Risk's John Raines)

- S&P futures sold-off sharply on the 12:54am EST twitter announcement of President Trump testing positive for COVID-19, but the index did retrace most of the losses after the US markets opened.

- Most US equity markets closed lower except for the Russell 2000 +0.5%; Nasdaq -2.2%, S&P 500 -1.0%, and DJIA -0.5%.

- 10yr US govt bonds closed +2bps/0.70% yield and 30yr bonds +3bps/1.49% yield, despite rallying to intraday highs of -3bps and -4bps, respectively, before the US equity markets opened.

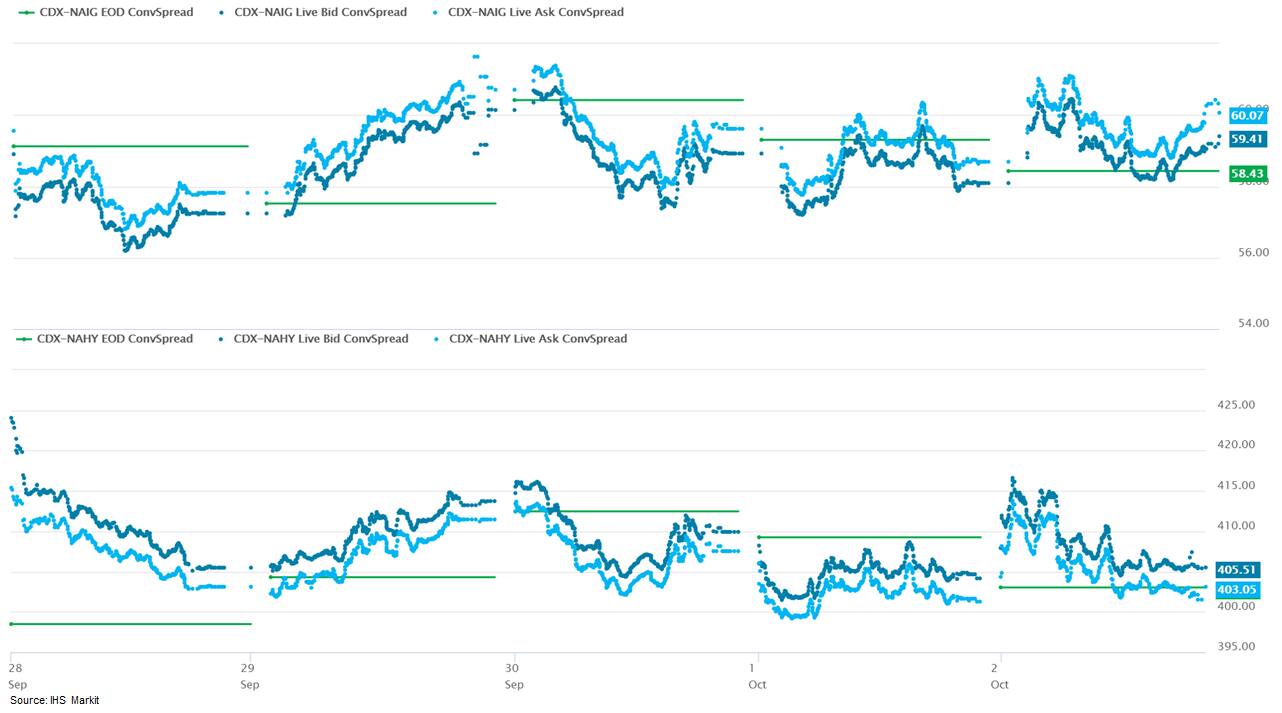

- CDX-NAIG closed +1bp/58bps and CDX-NAHY +1bp/404bps.

- DXY US dollar index closed +0.1%/93.81.

- Gold closed -0.5%/$1,908 per ounce and silver -0.9%/$24.03 per ounce.

- Crude oil closed -4.3%/$37.05 per barrel.

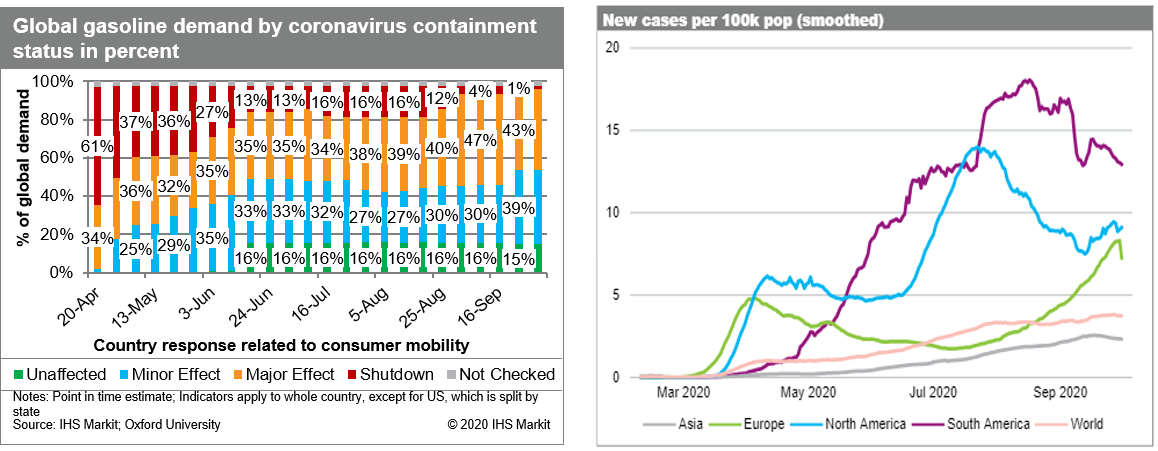

- As of 1 October, IHS Markit estimates that under half of global

gasoline demand was in countries or regions with major restrictions

on activity for the first time since March 2020, although barely.

The worldwide rate of new infection has been relatively flat since

August and the majority of large countries are seeing falling new

case rates. However, overall rates remain elevated in most

countries, and a few large countries are bucking the improvement

trend, including Iraq, Argentina, and much of Europe. Countries

with the harshest restrictions have slowly reduced them as new case

rates fall. However most countries never reduced below moderate

restrictions and these have remained steady on a regional

demand-weighted basis. After months of reducing restrictions, large

countries in Europe have started to reimpose restrictions as of

this week. Global mobility data does not show any signs of

improvement, although Google's decision to temporarily halt

publication of some of the key indices does hamper our ability to

get more granular. Workplace mobility, which has been flat in most

countries since June or July, has been flat or falling over the

last few weeks, with the exception of Brazil and Pakistan, which

appear to be trending upwards, uniquely among large gasoline

consumers. In the US, estimates of consumer spending and highway

VMT have been trending upward, suggesting greater activity, but

this trend has so far failed to be reflected in the OPIS data on

gasoline sales or EIA data on gasoline supplied to market, which

have been flat since July at around -10% y-o-y for the EIA or -17%

for OPIS. (IHS Markit Energy Advisory's Roger Diwan, Karim Fawaz,

Justin Jacobs, Edward Moe, and Sean Karst)

- US nonfarm payroll employment rose 661,000 in September, while

the unemployment rate declined 0.5 percentage point to 7.9%. The

gain in payrolls followed larger increases in prior months of the

recovery, and the level of payroll employment was still 10.7

million below the February peak. (IHS Markit Economists Ben Herzon

and Michael Konidaris)

- The slowing profile of payroll gains mirrors a slowing profile of monthly GDP, which decelerated to growth of 0.6% (monthly rate) in August and is expected to be roughly flat in September.

- Gains in overall payroll employment since April have reversed about one-half of the sharp drop in employment in the spring, with some industries faring better than others.

- Employment in accommodation and food services, hit hard by the pandemic, has reversed about 56% of its decline, and retail has reversed about 80% of its decline.

- Examples of industries where the recovery has lagged include professional and business services (reversed only 40% of the spring decline) and financial activities (reversed only 42% of its decline).

- The unemployment rate continues to trend lower, as the participation rate has essentially stalled over the last four months near 61.4%, well shy of 63.4% over January and February.

- Both average hourly earnings and the private workweek were above IHS Markit's assumptions, implying stronger momentum for private wages and salaries heading into the fourth quarter.

- US manufacturers' orders rose only 0.7% in August following

substantially larger increases over the prior three months.

Manufacturers' shipments rose 0.3% in August, down from increases

over the prior three months averaging 5.9% per month. (IHS Markit

Economists Ben Herzon and Lawrence Nelson)

- Both orders and shipments stalled in August shy of their pre-pandemic (February) levels, with orders still 5.3% below February and shipments still 3.3% below February.

- The slowing profile of orders and shipments mirrors slowing patterns in other aggregate data, including industrial production, payroll employment, and monthly GDP. The pattern across these data show robust, albeit only partial, recovery (of varying degrees) from the spring contraction.

- Orders and shipments of core capital goods, by contrast, are faring quite well. Both have surpassed their pre-pandemic levels (and were revised somewhat higher through August), indicating a robust recovery in equipment spending.

- Manufacturers' inventories were flat in August; we had expected a 0.4% decline. This led us to raise our estimate of real nonfarm inventory investment in the third quarter by about $19 billion.

- The University of Michigan US Consumer Sentiment Index rose 6.3

points (8.5%) to 80.4 in the final September reading, the highest

since March. The index has recovered just under one-third of its

decline from February to April, and is consistent with our

expectation for sharply slower growth of consumer spending in the

fourth quarter. (IHS Markit Economists David Deull and James

Bohnaker)

- The final September Consumer Sentiment reading was 1.5 points higher than the preliminary reading, suggesting that sentiment improved slightly over the course of the month.

- The expectations index rose 7.1 points to 75.6. The current conditions index increased 4.9 points to 87.8.

- Consumer sentiment rose 5.4 points to 77.2 among households earning less than $75,000 a year and rose 8.2 points to 83.6 among households with earnings above that threshold.

- Perceptions of buying conditions mostly improved in September. The index of buying conditions for large household durable goods rose 8 points to 114, while that for vehicles rose 2 points to 127. The index of buying conditions for homes slipped 1 point to 132, just shy of the 2019 average.

- The expected one-year inflation rate dipped sharply by 0.5 percentage point to 2.6% as some pandemic-induced price fluctuations have begun to normalize. Expected five-year inflation was unchanged at 2.7%.

- The University of Michigan's Consumer Sentiment Index and the Conference Board's Consumer Confidence Index moved back into sync in September, with each posting an improvement that left it about 20% beneath its respective February level.

- The recovery in consumer sentiment has thus far lagged that of other economic data such as consumer spending and payroll employment. This implies elevated caution on the part of consumers that may last until the threat of the COVID-19 pandemic has receded.

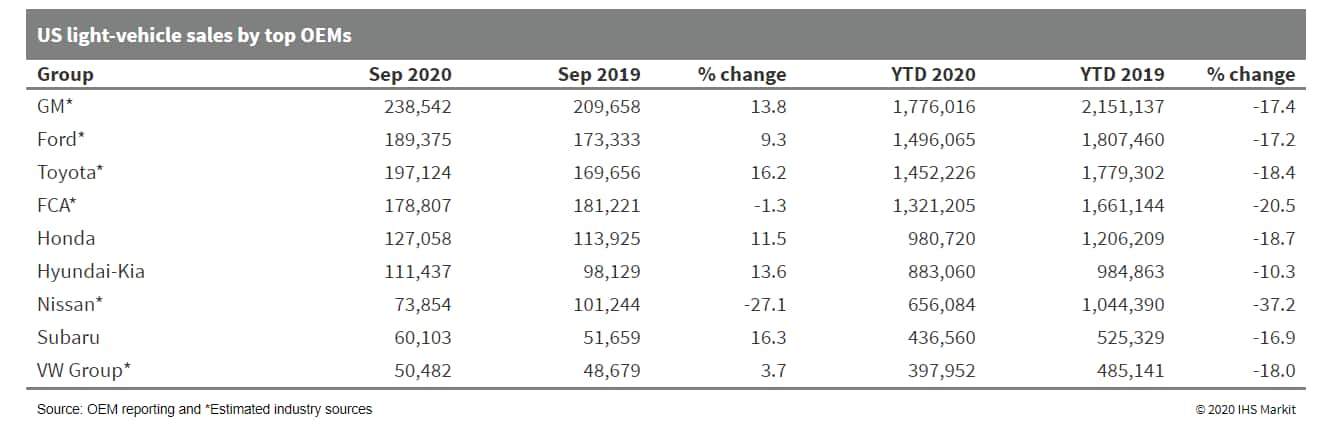

- US auto sales motor along with a seasonally adjusted selling

rate estimate of 15.9-16.3 million units at time of publishing, the

pace of light-vehicle sales continues to improve from the April

2020 low reading of 8.7 million units. (IHS Markit Economist Chris

Hopson)

- September 2020 sales benefited from two extra sales days, and the Labor Day holiday weekend, which fell in August for 2019 results. Incoming monthly sales figures from reporting automakers are reflecting year-on-year (y/y) improvements. On an unadjusted volume level, the sales tally for the month is expected to be up 2-5% y/y, the first time since February 2020 the market will realize monthly y/y growth.

- The outlook for the last quarter of the year remains blurred by political (election, stimulus policies) and economic uncertainty, but the sequential rise in auto demand levels from April reflects that consumers who are willing, ready, and able to enter a new car purchase are doing so.

- There were 25 selling days this September, two more than the year-earlier period.

- On a unit volume level, September sales are estimated to have climbed to approximately 1.30-1.33 million units, which would be above the year-earlier level, and bring the year-to-date light-vehicle sales volume figure through the third quarter to approximately 19% below the year-earlier level.

- We do not expect the pace of sales to advance much further than the September result, but the ongoing recovery in auto sales lends upside bias in expectations for the remainder of the year.

- Month-end September inventory levels as reported by AutoData at time of publishing were estimated to be up mildly from the previous month. Compared with month-end August, September 2020 industry inventory was up approximately 105,000 units. The days' supply reading at the end of September came down to a reading of 49 days' supply, down from a 50 days' supply level at the end of August and a 65 days' supply a year earlier.

- Please note: All industry-level numbers in this report are

estimates, owing to the absence of official monthly reports from

General Motors (GM), Ford, Fiat Chrysler Automobiles (FCA), and

others.

- Global securities lending returns declined by 28% YoY in

September, however as noted in the August snapshot the YoY

comparison is substantially affected by North American equity

specials for the latter portion of Q3 2019. In the context of 2020,

September was remarkable in its similarity to August, with global

returns increasing by 0.2% MoM. US equities were the largest

contributor to the YoY shortfall, as revenue from specials

continued to decline from the YTD peak in June and was well below

2019 returns. September was the fifth month of 2020 to deliver less

revenue than the 2019 comparable, the others were the months from

March to May, along with August. The total Q3 revenue was $2.2bn, a

16% YoY decline. In this note, we review some of the drivers of

global lending income in September. Varta Ag delivered $14 million

in September securities lending revenue, the firm's 2nd consecutive

month atop the global most revenue generator table. Borrow demand,

and fees, for the German battery maker have trended higher since a

January 8th report from an activist short seller suggested

increased Chinese competition in a category where the firm had been

viewed as an exclusive provider. (IHS Markit Securities Finance's

Sam Pierson)

- LyondellBasell and Sasol have agreed to form a joint venture (JV), under which LyondellBasell will pay $2 billion to acquire 50% of Sasol's new 1.5-million metric tons/year steam cracker, and low-density polyethylene (LDPE) and linear low-density polyethylene (LLDPE) plants with combined capacity for 900,000 metric tons/year, as well as associated infrastructure, at Lake Charles, Louisiana. The agreement includes customary rights for each partner regarding the potential future sale of its ownership interest, the companies say in a joint statement. The JV will operate under the name Louisiana Integrated PolyEthylene JV LLC. LyondellBasell and Sasol will each provide pro-rata shares of ethane feedstock to the cracker and offtake pro-rata shares of cracker and polyethylene (PE) products at cost, they say. LyondellBasell will operate the assets on behalf of the JV. Sasol will retain full ownership and operational control of its existing 454,000-metric tons/year Lake Charles East Plant ethane cracker, an R&D complex, and its performance chemicals assets at Lake Charles producing Ziegler alcohols and alumina, ethoxylates, Guerbet alcohols, paraffins, comonomers, linear alkylbenzene, ethylene oxide, and ethylene glycol, it says. Sasol said in August that it had received "strong global interest" for its Lake Charles Chemicals Project (LCCP) base chemicals assets and that a deal was expected to close by the end of the year. The overall current forecast cost of the LCCP is $12.8 billion, a cost that has soared from its original estimate of $8.9 billion. Sasol also reported a net loss of $5.3 billion for its full financial year ended 30 June. The last remaining unit to come online at the LCCP complex is the 420,000-metric tons/year LDPE facility, damaged in a fire earlier this year. It is still expected to achieve beneficial operations by the end of this month, according to Grobler.

- Electric vehicle (EV) startup Nikola has released an overview of its company plan, in the wake of the departure of founder Trevor Milton. Nikola also postponed indefinitely its planned Nikola World in-person event. The company describes itself as a "disruptor and integrator". Nikola says that it intends to integrate the next-generation truck technology, hydrogen fuelling infrastructure and maintenance to create a zero-emissions transportation ecosystem for its customers. Nikola said, "We assemble, integrate, and commission our vehicles in collaboration with support from business partners and suppliers that bring decades of experience in manufacturing, and that have invested billions of dollars in industrializing and scaling production. Nikola designs and engineers its vehicles and works with business partners and suppliers to manufacture a majority of the vehicle components." This plan is designed to give the company the "quickest, least capital-intensive path to market, in combination with our own intellectual property", it says. Nikola says its business comprises three units: Truck - battery electric vehicle (BEV) and fuel-cell EV (FCEV) Class 8 trucks; Energy - hydrogen fueling station network; and Powersports - outdoor recreational vehicles (ORVs). On the Tre BEV joint venture (JV) truck with CNH, being built at a JV factory in Ulm, Germany, Nikola said that the first batch of five prototypes will be completed in the next few weeks, and that the company remains confident it will begin full production and deliveries in the fourth quarter of 2021. Regarding the Tre, Nikola says its engineers have taken the lead on the human machine interface, infotainment, battery pack engineering and integration into the e-propulsion architecture, vehicle thermal management, and the e-axles. Nikola expects to begin testing production-engineered fuel-cell semi-truck prototypes by the end of 2021, and beta prototypes in the first half of 2022. Nikola has been working with Bosch on integration of the heavy-duty fuel-cell power modules, the company said. Although Nikola's plan also includes a hydrogen fueling station network, the company has the furthest way to go on this element. The company also confirmed that construction of its greenfield assembly plant in Coolidge, Arizona, United States, is on schedule for phase 1 to be completed by the end of 2021 and to be fully completed by mid-2023. This facility is due to have a production capacity of 35,000 Class 8 commercial semi-trucks annually. Nikola laid out the timeline of its company plan to calm investors after a scathing report was published by a research company. (IHS Markit AutoIntelligence's Stephanie Brinley)

- On 30 September, the International Monetary Fund (IMF)

Executive Board approved a new Extended Fund Facility for Ecuador

that replaces the March 2019 one, which was cancelled in May 2020

because of missed targets. (IHS Markit Economist Claudia Wehbe)

- Amid a severe financing squeeze and health crisis caused by the COVID-19 virus pandemic, Ecuador completed a distressed debt exchange (DDE) on 31 August after initiating a consent solicitation process that the government started in April. The DDE includes the exchange of 10 sovereign bonds for four new ones, postpones amortization payments to 2026, reduces interest payments to 6.9%, includes a 10% principal haircut and a USD1-billion zero coupon bond for past-due interest.

- Ecuador's government was in the process of negotiating a new Extended Fund Facility (EFF) with the IMF's Executive Board following the May 2020 cancellation of the prior EFF - approved in March 2019 - due to missed targets. In May 2020, the IMF had disbursed emergency funds totaling USD0.643 billion that offered short-term relief to support the health-system crisis triggered by the pandemic.

- Under the 27-month USD6.5-billion EFF approved on 30 September, Ecuador's government will receive a USD2-billion disbursement to support its budget immediately. The overall program's goal is to assist the government's continued effort to support macroeconomic stabilization and the foundation for strong growth, expand social assistance programs, ensure fiscal and debt sustainability, and strengthen the dollarization regime. Other objectives include improving transparency in public procurement, promoting debt transparency, and adopting robust cash management practices.

- According to Finance Minister Richard Martinez, more than 60% of the loan - USD4 billion - will be received in 2020, and two remaining disbursements totalling USD1.5 billion and USD1 billion will be received in 2021 and 2022, respectively.

- Uncertainty regarding the February 2021 election, fiscal commitments and reforms under the new agreement with the IMF remains high, although it is likely that any elected presidential candidate would honor the debt deal as the debt restructuring offers substantial relief.

- The deeper short-term liquidity squeeze has been averted and the government will be able to stay up to date with past due payments with suppliers, the social security, retirees, states and municipalities. Uncertainty about the length and depth of the pandemic add risks to the downside.

- IHS Markit projects the economy to remain in a severe recession in 2020 on the back of the external crisis, expecting negative GDP growth at close to -9.0% in 2020, while the government continues to work on its fiscal adjustment strategy. However, the decline could be larger than expected in the coming quarters, assuming weak oil prices in 2021-22 to remain below 2019 prices.

Europe/Middle East/Africa

- Most European equity markets closed higher except for Germany -0.3%; Spain/UK +0.4% and Italy/France flat.

- 10yr European govt bonds closed mixed; Italy -4bps, France -2bps, Spain -1bp, Germany flat, and UK +1bp.

- iTraxx-Europe closed -1bp/59bps and iTraxx-Xover

-1bp/342bps.

- Brent crude closed -4.1%/$39.27 per barrel.

- A new British standard for biodegradable plastic means that plastic claiming to be biodegradable will have to pass a test to prove it breaks down into a harmless wax which contains no microplastics or nanoplastics. To meet the PAS 9017 standard, the polymer has to pass tests which show it will biodegrade to a harmless state in real-world situations. The new standard was sponsored by Polymateria, based at Imperial College, London and agreed after independent review and discussions with stakeholders in the industry, the waste and recycling group Wrap, the Department for Environment, Food and Rural Affairs and the Department for Business, Energy and Industrial Strategy. The British Standards Institution's (BSI) specification has been met by Polymateria, a British company which has created a formula to transform plastic items such as bottles, cups and film into a sludge at a specific moment in the product's life. Once the breakdown of the product begins, most items, triggered by sunlight, air and water, will have decomposed to carbon dioxide, water and sludge within two years. Polymateria adds bio-transformation chemicals to the plastic when the packaging type is being made. The formulation differs from one type of plastic or pack to another. The biodegradable packaging will bear a clear recycle-by date, to inform consumers that they have a timeframe to dispose of them responsibly in the recycling system before they start breaking down. According to Niall Dunne, chief executive of Polymateria, in tests polyethylene film fully broke down in 226 days and plastic cups in 336 days. (IHS Markit Food and Agricultural Commodities' Neil Murray)

- Mobile network operator O2 has opened a commercial lab in Oxfordshire (UK) to help companies test connected and autonomous vehicles (CAVs). The facility, called Darwin SatCom Lab, has been launched as part of Project Darwin, a four-year pilot program based at the Harwell Science & Innovation Campus. The lab is backed by government funding from the UK Space Agency, which uses 5G and satellite technologies to trial ways of keeping vehicles connected. At the lab, O2 has already converted two Renault TWIZY electric cars into driverless cars, deployed with LiDAR sensors. This will allow these vehicles to be controlled from the lab and driven around the Harwell campus. Derek McManus, CEO at O2, said, "We're delighted to announce that the Darwin SatCom Lab is now open for business at Harwell Campus, allowing companies to put theory into practice and test innovative ideas using our connected and autonomous vehicles". (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Swedish passenger car registrations recorded an improvement

during September, according to data published by trade association

Bilindustrieföreningen (BIL Sweden). Sales increased by 7.3% year

on year (y/y) to 28,719 units. (IHS Markit AutoIntelligence's Ian

Fletcher)

- During the month, Volvo was the biggest selling brand with 7.9% y/y to 4,606 units, while Volkswagen (VW) in second slipped back by 13% y/y to 3,575 units.

- In third, Toyota registered 2,948 units, a leap of 54% y/y. The Swedish passenger car market has now fallen by 18.2% y/y to 202,644 units in the year to date (YTD).

- In the commercial vehicle categories, registrations of light commercial vehicles (LCVs) with a gross vehicle weight (GVW) of less than 3.5 tons slid by 2.2% y/y to 3,596 units during the month, although in the YTD, they remain down by 41.1% y/y at 20,592 units.

- Sales of heavy commercial vehicles (HCVs) with a GVW of more than 16 tons recorded a further modest improvement in September, gaining by 0.7% y/y to 452 units last month. Nevertheless, in the YTD, sales are down by 28.2% y/y at 3,568 units.

- Einride, a startup that specializes in electric and autonomous vehicles, has raised USD10 million in venture capital funding, reports VentureBeat. The funding for the latest round is secured from existing investors, including Norrsken VC, EQT Ventures, Nordic Ninja VC, and Ericsson Ventures. The company will use the capital to accelerate the official launch of its Einride Pod, an electric truck that can be remotely controlled by drivers and does not have a cabin. Robert Falck, Einride founder and CEO, said, "There is both a lot of excitement and a lot of uncertainty about autonomous trucking, but the fact remains: This is one of the largest business opportunities in the history of mankind We have a unique opportunity to make transport both exponentially safer and more sustainable. It's something the vast majority of us want, but many are unsure of how to get there and resort to half-measures." (IHS Markit Automotive Mobility's Surabhi Rajpal)

- The Russian city of Moscow has launched an autonomous car project to record parking violations, reports Intelligent Transport. The autonomous car is developed by the MosTransProekt Research Institute and deploys vehicle-to-everything (V2X) technology to communicate with traffic lights and detectors throughout its route. In this process, the vehicle can transmit and receive data through LTE communication channels and radio frequency interaction. Alexander Polyakov, director of the MosTransProekt Research Institute, said, "The vehicle's route goes along the inside of the Garden ring. The vehicle is equipped with a high-precision electronic map - a so-called 'digital twin' of the road. The map contains information about road boundaries, turning, speed limits, stops, markings and traffic lights. We are testing an innovative solution in the center of a metropolis - a merge of new mobility and city control over parking areas." This project is a first of its kind, deploying autonomous cars for parking enforcement trials. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Expectations of a return to fiscal consolidation and debt

reduction from 2021 after the temporary economic shock of the

spread of COVID-19 virus has prompted Moody's to revise its outlook

for Hungary to Positive. (IHS Markit Economist Dragana Ignjatovic)

- Moody's Investor Service (Moody's) has revised its outlook on Hungary's long-term sovereign debt rating to Positive from Stable. It maintained its sovereign rating for Hungary at BBB- on the generic scale (equivalent to 40 on the IHS Markit scale), the same level that IHS Markit currently has for the country's medium-term rating.

- The Positive outlook signifies that Moody's are likely to alter Hungary's rating in the near term. The revision reflects Moody's belief that, while the COVID-19 virus pandemic has had a substantial impact on Hungary, the effects are temporary and that the country's history of fiscal consolidation and debt reduction from 2015-19 will resume from 2021 onwards.

- Hungary's rating would be upgraded should the economic recovery forecast for 2021 materialize, with the government taking policy action to reverse the rising debt from 2020. The outlook would be returned to Stable should government commitment to fiscal consolidation waver or the country's debt trajectory continues to accelerate.

- IHS Markit's and Moody's current rating at investment grade is one notch below S&P Global Ratings (S&P) and Fitch Ratings at one notch higher.

- Hungary's economy (alongside most in Europe and the world) is facing significant downside risks for 2020 as the country struggles to deal with the COVID-19 virus pandemic. IHS Markit is currently forecasting a contraction of 7.8% in 2020, reflecting the historic fall in economic activity in the second quarter. The fiscal deficit is forecast to rise to 6.4% of GDP as the government attempts to support households and businesses in the aftermath of the severe lockdowns implemented in the second quarter. Public debt is also forecast to rise to 69% of GDP, the first increase in debt levels since 2009.

- Although a statistical rebound in the third quarter of 2020

from the historical low recorded in April-June is forecast, the

latest trade data combined with the collapse of summer tourism

revenues and rising infection numbers across Europe will result in

Albania's economy continuing to underperform through the second

half of 2020. (IHS Markit Economist Dragana Ignjatovic)

- According to detailed data released by the Albanian Institute of Statistics (INSTAT), real GDP growth fell 11% year on year (y/y) in the second quarter of 2020. This is the third consecutive quarter of declining economic activity, although the second-quarter print is the largest real GDP fall since records began. The contraction in real GDP in the first half of 2020 averaged 6.7% y/y.

- The decline has been led by the foreign trade sector, with exports down 50% y/y in the second quarter and imports dropping 36% y/y. The sharp deterioration in foreign trade reflects the spread of COVID-19 virus throughout Europe and national lockdowns which resulted in a collapse in demand. The uneven decline has resulted in exports only accounting for around 52% of imports, down from more than 70% in the first quarter of 2020.

- Domestic demand was another key component of the second quarter collapse, with the fall in fixed investment (-11% y/y) compounded by the 7.6% y/y drop in private consumption. Investment has been falling since the second quarter of 2019, with the pace of decline steadily gaining speed, reflecting the completion of several large infrastructure projects in the country as well as the increased risk aversion following the November 2019 earthquake and the spread of COVID-19 through Europe in the first quarter of 2020. Meanwhile, government spending held up relatively well, falling by only 0.7% y/y as the state stepped in to support households and business suffering from the economic impact of the pandemic and associated lockdowns.

- Across value added, the only segment to post growth was agriculture. Retail trade recorded the largest fall (-27% y/y) reflecting the closure of non-essential shops as part of the country's response to COVID-19. Meanwhile, industry contracted by 13.8% y/y, with manufacturing down by close to 20% y/y as factories suffered from supply chain disruption and social distancing requirements as well as a lack of domestic and external demand. The construction sector, also contracted although the pace of decline in the second quarter eased to 12.4% y/y.

- In a separate INSTAT release, Albania's unemployment rate ticked up to 11.9% in the second quarter of 2020, up 0.7 percentage points from the historic low 11.2% in the fourth quarter of 2019.

- Although the historic fall in economic activity in the second quarter is likely to result in a statistical bounce back in July-September, the outlook for Albania's economy remains challenging. Despite the easing of the social distancing measures in late May, the Albanian economy continues to feel the impact of the spread of the COVID-19 virus through Europe. Albania's overreliance on Italy in its foreign trade and remittance inflows, could present a problem should a second wave of infections prompt renewed lockdowns.

- Equatorial Guinea's 2020 second-quarter real GDP declined by

4.9% year on year (y/y), driven by a sharp decline in oil

production because of measures put in place to contain the spread

of the COVID-19 virus and low output from maturing oil fields. (IHS

Markit Economist Archbold Macheka)

- Oil GDP, which anchors Equatorial Guinea's national output, fell by 4.1% y/y, reflecting an 11.7% y/y contraction in hydrocarbon production. Oil production dropped from 28.7 million barrels during the second quarter of 2019 to 25.3 million barrels during the second quarter of 2020. This is because of COVID-19-virus containment measures, which forced oil companies to reduce the workforce working on their oil facilities. Declining oil output from maturing oil fields was also a significant contributor to the low production level.

- Non-oil GDP shrunk by 6.0% y/y, owing to public spending contracting by 1.5% y/y, thanks to weakness in investment spending and current spending, which fell 2.7% y/y and 1.0% y/y, respectively. Non-Oil GDP was also constrained by the fall in money supply of 5.5% y/y, on the back of private companies reducing their deposits in most commercial banks. Inflation, which ticked up to 3.0% y/y largely because of COVID-19-virus-related supply-chain disruption, is also another contributor to the decline in non-oil GDP.

Asia-Pacific

- Most major APAC equity markets were closed for market holidays today, with the two that were open closing lower on the day; Australia -1.4% and Japan -0.7%. Please note that equity closes published 1 October for Mainland China, Hong Kong, and South Korea were incorrect, as all those markets were actually closed, and the performance was a repeat of the previous close.

- China began its eight-day Golden Week holiday on 1 October, which incorporates the National Day and Mid-Autumn Festival, and means many market players are now on leave until next Friday. Limited thermal import activity was seen before the holiday, amid uncertainties over policies and demand changes after the long break. However, domestic prices moved into the government designated "red zone," reaching RMB608/t ($89.28/t) FOB Qinhuangdao, basis 5,500 kc NAR, on Wednesday amid persistent supply strains, prompting expectations of possible price cooling measures after the holiday. Daily consumption at Zhejiang Electricity Power, the only major coastal power reporting consumption data at present, was 0.12 mt/d on Tuesday, the last reported figure before the break, and inventory at its plants was 4.37 mt, enough for 38 days of consumption. Inventory at the domestic loading port Qinhuangdao (QHD) was 5.02 mt on 30 September, dropping from 5.04 mt in the week before and inventory at discharging port Guangzhou stood at 2.37 mt on Wednesday, down from 2.46 mt reported last Friday. (IHS Markit Global Coal)

- Tesla's China-made Model 3 is now available with lithium iron phosphate (LFP) batteries. According to Tesla's Chinese website, the price of the standard-range Model 3 was adjusted from CNY271,550 (USD39,977) to CNY249,900 after government subsidies on 1 October. The price of the long-range Model 3 is CNY309,900, down from CNY344,050. Both models are currently produced at Tesla's Gigafactory Shanghai in Pudong district. The price of the performance version of the Model 3 remained unchanged as of 1 October. Tesla did not disclose details of the new batteries in the Model 3. However, specifications-wise, the standard-range Model 3 with LFP batteries can now deliver a range of 468 km, an increase of 23 km compared with the same vehicle powered by nickel-manganese-cobalt (NMC) cells. Reuters first reported Tesla's intention to introduce LFP batteries to the Model 3 in February. The model gained approval from Chinese regulators in June. Compared with lithium-ion (Li-ion) batteries equipped in Tesla's current models, LFP batteries are less expensive as they do not contain cobalt - one of the most expensive materials in Li-ion batteries. (IHS Markit AutoIntelligence's Abby Chun Tu)

- Hongqi, the premium brand of FAW Group, has announced the pre-sales pricing of the E-HS9 electric sport utility vehicle (SUV). Two versions of the model are available for reservation now, with pre-sales prices starting from CNY550,000 (USD80,990). With a body length of 5,200 meters, the E-HS9 represents the largest model from the Hongqi family and it is designed to showcase Hongqi's capacity to build a luxury SUV that delivers both the performance and the top-notch quality that customers in this segment expect. Based on the FAW's FME platform, the E-HS9 will provide several battery options including an 85-kWh battery pack, a 99-kWh battery pack, and a 120-kWh battery pack. The battery cells are supplied by Chinese battery-maker CATL. The top-of-range model will feature four-wheel drive with two electric motors to deliver a combined output of 405 kW and a peak torque of 750 Nm. According to Hongqi, the E-HS9 with a 120-kWh battery pack can deliver a range of up to 650 kilometers. To cater for the needs of business customers, the E-HS9 will provide three seating configurations: a two-row four-seater, a three-row six-seater, and a three-row seven-seater. The E-HS9's suspension system also features continuous damping control, which continuously adjusts the damping force on each wheel based on road conditions and driving style. The E-HS9 from Hongqi represents one of most important launches from Chinese automakers this year. As a full-size luxury SUV, the E-HS9 is designed to present a flagship Hongqi model transformed by the brand's newest design language and brand philosophy. (IHS Markit AutoIntelligence's Abby Chun Tu)

- China's dairy imports (including infant formula) grew 6.3% in volume and 5% in value, driven by a strong recovery in whey imports as the African Swine Fever (ASF) situation eases, according to customs data. China imported a total of 2.15 million tons of dairy products (including IMF), with import value reaching USD8.3 billion in the first eight months of the year (January-August). The most drastic volume surge was seen in whey, growing by 35% in volume to 395,000 tons, with supplies hitting at least a 10-year maximum. Due to a rapid decline in international whey prices, import value in the period totaled USD408.7 million, or 2.4% lower. This recovery could be attributed to the improving situation with the ASF outbreak in Chinese industrial farms, that has been lasting for the last two years, which is one of the main industries in China importing whey for animal feed purposes. Butter's imports have also rebounded, seeing a 40.5% surge in import volume to 85,000 tons. On the other hand, milk powders' performance lagged behind volumes imported in the same period last year. While largest import category WMP held up fairly flat (1.2%) at 478,400 tons, SMP experienced a 10.1% plunge to 219,600 tons. In addition, imports of IMF have seen a decline for the first time in the same period in the last five years. China imported almost 3% less IMF in January-August, a volume of 231,900 tons. (IHS Markit Food and Agricultural Commodities' Jana Sutenko)

- Japan's unemployment rate rose in August for the second

consecutive month. The modest pace of Japan's economic recovery

could continue to increase unemployment. (IHS Markit Economist

Harumi Taguchi)

- Japan's unemployment rate rose by one notch to 3.0% in August, largely reflecting an increase in labor participation, as the number of employees rose by 11,000 from the previous month while the labor force rose by 23,000 from a month earlier. This suggests people who left the labor market because of containment measures came back to seek jobs in line with the resumption of economic activity.

- That said, the reason behind the increase in the number of unemployed was also due largely to jobs losses because of the circumstances of employers or businesses. The rise in employment was largely due to increases in the number of self-employed and a softer decline in the number of part-timers while year-on-year (y/y) growth for full-timers weakened.

- Job opportunities were also more severe for job seekers. The ratio of active job openings to active job applications continued to fall in August 2020, moving down to 1.04, the lowest level since January 2014, reflecting a faster increase in active job applications despite the second consecutive month of rise in effective job openings. A rise in the ratio of new openings to new applications signaled marginal improvement for job opportunities, but new openings remained weak (27.8% below the year-earlier level) and new job openings for full-time positions declined at a faster pace.

- The September results suggest employment conditions remain weak and severely affected by persistent soft economic activity. Sluggish recovery could increase the unemployment rate by pushing up bankruptcies and business closures and turning furloughs into unemployment. While the government's measures have helped support employment, the number of furloughs rose by 30,000 in August from the end of 2019 on a non-seasonally adjusted basis.

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-2-october-2020.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-2-october-2020.html&text=Daily+Global+Market+Summary+-+2+October+2020+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-2-october-2020.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - 2 October 2020 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-2-october-2020.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+2+October+2020+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-2-october-2020.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}