Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Dec 03, 2020

Daily Global Market Summary - 3 December 2020

Global equity markets closed mixed for a second consecutive day, while US and European benchmark government bonds closed higher on the day. European iTraxx credit indices closed tighter across IG and high yield, while CDX-NA was close to flat on the day again. The US dollar closed lower and gold, silver, and oil were all higher.

Americas

- Most major US equity indices closed higher except for S&P 500 -0.1%; Russell 2000 +0.6%, DJIA +0.3%, and Nasdaq +0.2%.

- 10yr US govt bonds closed -3bps/0.91% yield and 30yr bonds -3bps/1.66% yield.

- CDX-NAIG closed -1bp/50bps and CDX-NAHY flat/300bps.

- DXY US dollar index closed -0.3%/90.70 and is at its lowest point since April 2018.

- Gold closed +0.6%/$1,841 per ounce, silver +0.2%/$24.14 per ounce, and copper flat/$3.49 per pound.

- Crude oil closed +0.8%/$45.64 per barrel.

- OPEC and a group of Russia-led oil producers agreed to increase their collective output by 500,000 barrels a day next month, signaling the world's biggest producers are betting the worst of a pandemic-inspired shock to demand is behind them. The deal marks a compromise after sharp disagreements earlier in the week among a group of producers that have acted in relative concert for months, agreeing to cut production deeply to stabilize oil markets. (WSJ)

- In a press release, Chevron Corporation announced a 2021

organic and exploratory capital budget of $14 billion. That

compares with the revised 2020 capital budget of $14 billion,

announced in May 2020. (IHS Markit Upstream Companies and

Transactions' Karan Bhagani)

- The company slashed its 2020 capital budget in response to lower commodity prices and reduced demand resulting from the COVID-19 pandemic, down about $6 billion (or ~30%) from its original capital budget of $20 billion, announced in December 2019.

- The 2021 budget allocates $11.5 billion to the upstream, with $5 billion for the US upstream and $6.5 billion for the international upstream.

- The budget allocates $2.1 billion to the downstream, with $1.2 billion for the US downstream and $0.9 billion for the international downstream.

- In the upstream for 2021, $6.5 billion is allocated to currently producing assets, including about $2 billion for Permian unconventional development, the company said.

- A total of $3.5 billion in the upstream is planned for major capital projects underway, of which about 75% is associated with the future growth project and wellhead pressure management project at the Tengiz field in Kazakhstan.

- The remaining $1.5 billion is allocated to exploration, early stage development projects, and midstream activities. The company also lowered its longer-term guidance to $14 to $16 billion annually through 2025, down from its previous guidance of $19 to $22 billion.

- AT&T's Warner Bros will debut its movies online and in cinemas simultaneously next year, the most dramatic move by a studio yet as the pandemic forces Hollywood to tear up its decades-old playbook for releasing blockbusters. In an announcement that sent shares in cinema chains sharply lower on Thursday, Warner Bros said it will make movies available on the group's HBO Max streaming service for one month in the US at the same time as it releases them in cinemas. (FT)

- The seasonally adjusted final IHS Markit US Services PMI

Business Activity Index registered 58.4 in November, up from 56.9

in October. The latest reading was higher than the earlier 'flash'

estimate (57.7) and signaled the sharpest expansion for over

five-and-a-half years. Growth of business activity was often linked

to greater new order inflows and the release of pent-up demand, as

clients became less hesitant to make purchases. (IHS Markit

Economist Chris Williamson)

- Contributing to the marked upturn in output was an accelerated rise in new business at service providers in November. The rate of growth was the fastest since April 2018.

- New export orders increased at only a marginal pace. The latest expansion in foreign demand was the slowest since July and eased once again from August's survey-record high. A number of panelists suggested that ongoing travel restrictions due to the COVID-19 pandemic made international business challenging.

- In line with greater client demand, firms increased their workforce numbers to a greater extent in November. The expansion in employment was the sharpest since data collection began in October 2009. Some firms stated that employees previously let go due to the pandemic had been rehired.

- Business expectations strengthened in November, as service providers were boosted by a faster expansion in new business and hopes of a vaccine. The degree of confidence was the highest since January 2014 and well above the long-run series average.

- California Governor Gavin Newsom warned Thursday that the state would impose a new shelter-at-home order if hospitals start running short of intensive-care capacity, a dire possibility that could happen in some areas as soon as this week. It would take effect once a region's hospitals had only 15% of their intensive care unit beds available, a threshold none have crossed so far. If imposed, the order would last three weeks. (Bloomberg)

- US seasonally adjusted (SA) initial claims for unemployment

insurance fell by 75,000 to 712,000 in the week ended 28 November.

While claims are well below the spring high, initial claims remain

at historically high levels—the high during the Great Recession

was 665,000. The not seasonally adjusted (NSA) tally of initial

claims fell by 122,453 to 713,824. (IHS Markit Economist Akshat

Goel)

- Seasonally adjusted continuing claims (in regular state programs), which lag initial claims by a week, fell by 569,000 to 5,520,000 in the week ended 21 November. Prior to seasonal adjustment, continuing claims fell by 690,170 to 5,240,575. The insured unemployment rate in the week ended 21 November was down 0.4 percentage point to 3.8%.

- There were 288,701 unadjusted initial claims for Pandemic Unemployment Assistance (PUA) in the week ended 28 November. In the week ended 14 November, continuing claims for PUA rose by 339,068 to 8,869,502.

- Pandemic Emergency Unemployment Compensation (PEUC) claims have been steadily rising as claimants are exhausting their regular program benefits. In the week ended 14 November, continuing claims for PEUC rose by 59,732 to 4,569,016.

- The Department of Labor provides the total number of claims for benefits under all its programs with a two-week lag. In the week ended 14 November, the unadjusted total rose by 349,633 to 20,163,477.

- The Government Accountability Office claimed that the Department of Labor's estimates of the number of individuals receiving benefits are flawed. The inaccuracies largely stem from inconsistent reporting from states and while the Labor Department does not anticipate a change in its methodology for counting claims, it expects to add a clarifying statement in future weekly news releases.

- US employers announced 64,797 planned layoffs in November,

according to Challenger, Gray & Christmas—down 19.7% from

October's 80,666. November's total is the second-lowest of the year

and the lowest since February but is still 45.4% higher than the

number of cuts announced in November 2019. (IHS Markit Economist

Juan Turcios)

- November was the ninth month to report job-cut announcements specifically because of the COVID-19 pandemic, which totaled 5,873 for the month. Employers cited other reasons including restructuring, market conditions, and a downturn in demand more frequently than COVID-19 as causes of job-cut announcements in November.

- For the year to date (YTD), 2,227,725 job cuts have been announced, 298% higher than the same period in 2019. The current YTD total has already surpassed the record annual total of 1,956,876 announced job cuts in 2001, with one month remaining in the year (Challenger began tracking job-cut announcements in January 1993).

- Of the total job cuts announced so far this year, 1,105,599 were because of COVID-19, according to employers.

- Unsurprisingly, the hardest-hit sector and recipient of the lion's share of the coronavirus-related cuts this year continues to be the entertainment/leisure sector, which encompasses bars, restaurants, hotels, and amusement parks. Year to date, companies in the entertainment/leisure sector have announced 857,620 cuts, a whopping 843,231 higher than during the same period in 2019. The entertainment/leisure sector announced 11,666 cuts in November, the highest number of announced cuts out of the 30 industries tracked by Challenger.

- Technology companies and transportation companies announced the second- and third-highest job cuts in November with 11,431 and 10,455, respectively.

- Rounding out the top five most adversely affected sectors year to date were retail (182,307 job cuts), transportation (170,129 job cuts), services (156,662), and automotive (86,400 job cuts).

- Only 4 out of the 30 industries that are tracked by Challenger have announced fewer job cuts YTD than during the same period last year: financial, chemical, utility, and pharmaceutical.

- Uber Technologies is reportedly in advanced talks to sell its air taxi business, Uber Elevate, to US-based aerospace startup Joby Aviation, reports Reuters. Uber's air taxi business was designed as an "urban aviation ride-sharing product" to reduce traffic congestion on the ground. Uber is refocusing on its core businesses, including ride-hailing and food delivery, since the COVID-19 virus pandemic. Uber laid off 6,700 employees globally in two phases and has reduced its workforce by 25% since the pandemic began. Uber is concentrating on achieving probability, which may include selling off loss-making divisions. Uber is also reportedly in talks to sell its autonomous vehicle business. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- US-based software-as-a-service (SaaS) solution provider Ridecell has raised USD45 million in a Series C funding round led by venture capital firm Fort Ross Ventures, according to a company statement. New investor Solasta Ventures and existing investors including Activate Capital, Denso, LG Technology Ventures, and Initialized Capital also participated in the round. The startup company will use the capital to automate and digitalize its platform, support larger customers globally, and accelerate its international growth. Aarjav Trivedi, CEO of Ridecell, said, "The leading fleets in the world were already working on digital transformation. COVID-19 created an urgent need for them to accelerate digital access to their fleets, reduce risk by enabling self-service touch-less monetization across B2B and B2C business models, and reduce costs through automation. For Ridecell, it created opportunities to help many customers and partners quickly meet the shifting consumer and enterprise demand for fleet operations automation and contactless commerce." (IHS Markit Automotive Mobility)

- Braskem Idesa said it is taking immediate steps to shut its

Etileno XXI ethylene-polyethylene petrochemical complex at

Coatzacoalcos, Mexico, after Mexico's state-owned operator of gas

pipelines halted gas supplies. Mexico's National Natural Gas

Control Center (Cenagas) said 30 November that it would not renew a

contract for supply of natural gas and blocked the entry of gas to

the site the following day, Braskem Idesa said in a statement. (IHS

Markit Chemical Advisory)

- There are indications that the decision was driven by Mexican President Andrés Manuel López Obrador ("AMLO"), who announced that Pemex would no longer supply natural gas to Braskem Idesa, according to Adrian Calcaneo, senior consultant with IHS Markit.

- According to López Obrador, the supply contract expired and would not be renewed. This coincides with the lack of agreement on the renegotiation of the ethane supply contract that Braskem Idesa has with Mexico's state-owned oil firm Pemex, which the president has called "leonino" ( or unfair or abusive).

- Pemex has struggled to meet ethane supply commitments to the plant, the largest petrochemical investment in Latin America, as Mexico's oil and gas production has significantly decreased over the past few years.

- The Braskem Idesa complex, which comprises a 1.05 million metric ton/year ethylene plant and three polyethylene (PE) units, had a utilization rate of 84% in the third quarter of 2020, according to a recent Braskem presentation. The main grades of PE produced are high-density polyethylene (HDPE) for blow molding and film, and low-density polyethylene (LDPE) for film. Braskem Idesa earlier this year started importing ethane from the US to the plant. Braskem Idesa has spent $4 million on logistics infrastructure and to be able to import up to 12,800 b/d of ethane, 19% of the volume required by the facility.

- Mexico's Instituto Nacional de Estadistica y Geografia (Inegi)

has published brand-level sales data for November 2020, reflecting

total sales 95,485 units. This is a 23.5% year-on-year (y/y)

decline, although ahead of the more than 84,000 units sold in

October 2020. Media reports also point out that this result was the

worst November since 2012, and that the 23.5% decline is the

sharpest decline reported for November sales in 25 years. (IHS

Markit AutoIntelligence's Stephanie Brinley)

- It also broke the streak where month-on-month (m/m) declines eased, as November's decline was higher than the 21.3% y/y decline reported in October.

- The low point in 2020 was in May, with only about 42,000 units sold. Mexican demand is declining during the global COVID-19 virus pandemic and from the country's lockdown and social distancing measures taken in April and May 2020; although lockdown measures have not been as severe, COVID-19 infections were increasing throughout November.

- Despite the decline in sales, top-three brand rankings remain

relatively consistent.

- Nissan maintains its lead in the Mexican market. It sold 18,428 units in November, declining 27.8% (Infiniti sold 71 units, down 39% from November 2019).

- Nissan was followed by General Motors (GM) at 14,115 units (down 30.1% y/y).

- Volkswagen (VW) held third place with 10,365 units sold (down 24.3%). Audi is reported separately from VW and fell by a smaller 5.1% y/y to 1,060 units.

- Kia has remained ahead of Toyota to claim fourth for the month again, though it was close. Kia sold 7,819 units sold (down 8.4% y/y), while Toyota's sales declined 26.2% y/y to 7,757 units.

- Mexico's overall light-vehicle sales declined in 2018 and 2019, and 2020 had started off soft prior to the COVID-19 situation. Prior to the pandemic, IHS Markit had expected a decline of 2.6% y/y in 2020, to 1.280 million units. However, the October 2020 forecast round factoring in COVID-19 disruption as well as ongoing recovery efforts instead puts the country's full-year sales down 29.3% to about 934,498 units, including a drop of about 25% in the fourth quarter.

- Colombia's unemployment rate fell to 14.7% from its COVID-19

peak of 21.4% in May. The recovery has come amid reopening of the

economy (currently in an extended "selective isolation" phase since

1 September) following strict lockdown procedures at the start of

the pandemic, but the rate remains significantly above the October

2019 level of 9.8%. (IHS Markit Economist Lindsay Jagla)

- Notably, the number of employed people improved to 21.3 million from a low of 16.5 million in April, a recovery of 86.7% of the jobs lost since February. Nevertheless, the number of employed people in Colombia remains 6.7% below the number employed in October 2019.

- The greatest negative drivers of Colombia's employment numbers were sales and repairs of auto vehicles, public administration and defense, education, healthcare services, accommodation, and food services.

- Colombia's gradual economic recovery has continued throughout the last few months with indicators such as the manufacturing PMI, retail sales, and industrial production all continuing to show improvements. Colombia's third-quarter GDP data release also reflected the economic recovery, with quarterly GDP improving by 8.7% compared with the second quarter.

- The Central Bank of Paraguay (Banco Central del Paraguay: BCP)

reports that consumer prices increased by 0.7% month on month (m/m)

and 2.2% year on year (y/y) in November. Citing below-target

inflation and lack of upward pressure, the BCP monetary policy

committee has kept the policy rate at the current level of 0.75%.

(IHS Markit Economist Jeremy Smith)

- In year-on-year terms, November was the first month since April that inflation, which fell to as low as 0.48% y/y in June, exceeded 2%, which is the lower end of the BCP's 4% +/- 2% target range.

- Seasonal increases in food prices, recovering internal and external demand following the gradual relaxation of containment measures, and pass-through from depreciation of the guaraní, which has fallen 11.7% y/y against the dollar, account for much of the recent upswing.

- In addition, the price of healthcare products (especially pharmaceuticals) continued to rise (3.7% y/y), as did prices of home repair and construction materials, supported by strength in the construction sector and more expensive raw materials for cement.

- Meanwhile, the tone and substance of the BCP's November meeting varied little from recent months, as the bank's monetary policy committee unanimously opted to hold the policy rate constant for the fifth consecutive month.

- The BCP believes that its expansionary measures will lift inflation to the 4% target rate within the scope of the monetary policy horizon, which it defines as 18 to 24 months. This is consistent with IHS Markit's view of a gradual increase in annual inflation, forecast at just 1.7% for this year, arriving at the target in 2023.

- The consumer confidence subindex for confidence in the current economic situation came in at 23.9 in October, far below the neutral level of 50, and it has hardly moved since plummeting in April. Nonetheless, the subindex for expectations over 2021 is at 63.9, which is perhaps suggestive of deferred expenditures, particularly on durable goods.

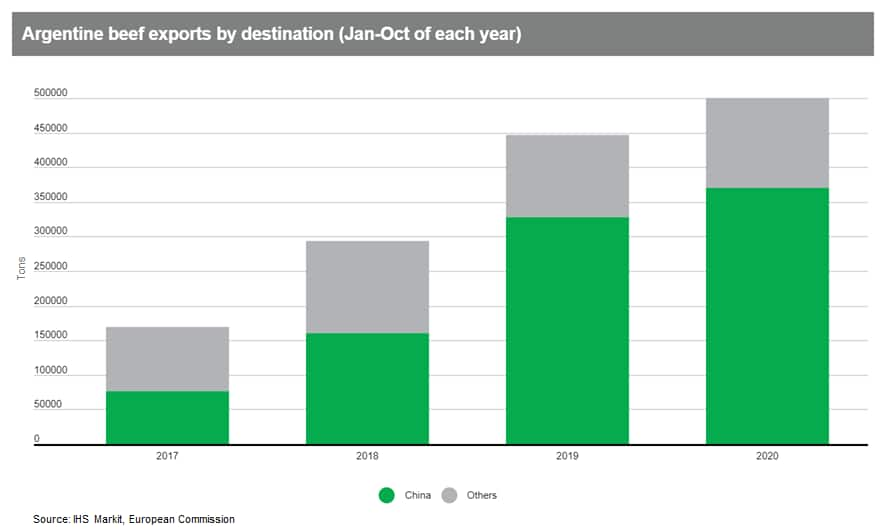

- China has strengthened its position as the biggest buyer of

beef from Argentina and Chile and now absorbs more than 80% of

total shipments from the two countries. Newly released figures show

that Argentina shipped 59,252 tons of unprocessed beef in October -

down 9.2% y/y. The share of this going to mainland China rose to

82% from 76% in the same month last year. Chile is the second most

important buyer of Argentine beef but its share of total volumes

stands at just 4%. Cumulative exports of Argentine beef reached

almost 500,000 tons worth USD2.25 billion in the January-October

period. In volume terms, this was 12% higher y/y but export

earnings were down 6% y/y as a result of sharply lower average

export prices for bone-in beef. A small decline in shipments of

chilled beef has been more than offset by higher volumes of frozen

product, which rose by 15% y/y in the Jan-October period. Within

the frozen segment, shipments of bone-in beef have risen sharply

thanks to strong demand from China. In October alone, exports of

frozen bone-in beef were close to double year-ago levels, with

almost all of this going to mainland China. (IHS Markit Food and

Agricultural Commodities' Ana Andrade and Max Green)

Europe/Middle East/Africa

- European equity markets closed mixed; UK +0.4%, Italy +0.2%, France/Spain -0.2%, and Germany -0.5%

- 10yr European govt bonds closed higher across the region; Italy/Germany -4bps and Spain/France/UK -3bps.

- iTraxx-Europe closed -1bp/46bps and iTraxx-Xover -8bps/243bps.

- Brent crude closed +1.0%/$48.71 per barrel, which is its highest closing price since 5 March.

- The planned mass rollout of an approved COVID-19 vaccine is

positive news for the UK economy and should fuel stronger GDP

growth from mid-2021. The main fillip to activity from mid-2021

should be less draconian social-distancing measures to allow

consumer-facing services to operate under normal trading

conditions. In addition, returning office workers will repopulate

city centers and increase footfall for the hospitality sector and

high-street retailers. (IHS Markit Economist Raj Badiani)

- The United Kingdom has approved the Pfizer/BioNTech COVID-19 vaccine at an accelerated and unprecedented pace, and it is the first country to sanction a mass vaccination program. The Pfizer/BioNTech vaccine is still waiting for approval from the United States and the European Union.

- The UK has ordered 40 million doses, which is enough to vaccinate 20 million people, with each person receiving two doses 21 days apart.

- The government will reach out first to the most vulnerable groups, including healthcare workers. Health Secretary Matt Hancock has announced that hospitals, mass vaccination centers, and GP surgeries are to administer the vaccine to those most in need.

- The rollout of the vaccine could provide further encouragement for the UK government to ease gradually its COVID-19 virus-related regional restrictions from March or April 2021, with a clearer route to economic normality emerging (see United Kingdom: 24 November 2020: UK government announces new three-tier system to replace the temporary lockdown in England from 2 December). The government hopes that the majority of older people, care-home residents, and those with severe conditions will have their jabs by early 2021.

- The planned vaccination program is welcome news after the latest tightening of COVID-19 virus-related containment measures, which will trigger renewed UK GDP losses in the final quarter of 2020. The impact of the shutdown is that the economy is likely to contract by around 10% month on month (m/m) during November, followed by an immediate rebound in December, implying a drop of around 4.0% quarter on quarter (q/q) in the fourth quarter as a whole.

- However, we acknowledge some challenges during the next few months. First, the UK could require stricter restrictions in January or possibly February should new infections rise in the aftermath of less draconian regional lockdowns during the Christmas period. Second, the mass vaccination program in the UK is unprecedented, and some work will be required to persuade everyone to take the vaccine.

- We assume that the European Union and the UK will avoid a disorderly Brexit, reaching a trade agreement or arrangement from 1 January 2021. The rising number of COVID-19 cases in the UK and the rest of Europe will focus the minds of the two negotiating parties to reach an agreement, and to accept collective responsibility to avoid a further economic shock for the region that would arise from failed EU-UK trade negotiations.

- Nevertheless, Brexit costs underpin our cautious assessment of UK growth for 2021 when compared with most other advanced economies. We fear that the likely new EU-UK trading arrangements could be a slimmed-down version, representing a trade shock to the UK economy. First, UK manufacturers could encounter new non-tariff barriers in the face of some regulatory divergence between the UK and the EU, implying new checks and delays to verify compliance with EU rules. Furthermore, some types of UK services will find it more challenging to export to the EU from next January when the UK leaves the Single Market, triggering a raft of new non-tariff barriers.

- October's strong Eurozone overall month-on-month (m/m) rise in

retail sales masks divergence in sales by type of product, while

containment measures will have hit activity hard in November. (IHS

Markit Economist Ken Wattret)

- Eurozone retail sales volumes rose by 1.5% m/m in October, double the market consensus expectation (of 0.8% m/m, according to Reuters' survey). The 4.3% year-on-year (y/y) increase also surpassed consensus expectations (of 2.7% y/y).

- In level terms, retail sales volumes are now more than 3% higher than back in February, prior to the impact of the COVID-19 shock, which saw sales collapse in March and April.

- Although this is an encouraging start to the fourth quarter,

there are reasons for caution:

- First, October's increases came ahead of the implementation of more stringent COVID-19 virus-related containment measures across member states, which will have hindered sales in some areas in November.

- Second, the rebound in retail spending on some items is a substitution for expenditure on services, which are being disrupted by the pandemic. For many member states, retail sales account for less than half of overall consumer expenditure.

- Third, October's breakdown of sales by type of product shows a mixed picture:

- Mail order and internet sales, which have unsurprisingly outperformed during the pandemic, rebounded strongly in October (6.1% m/m) and are up by more than 22% compared with their February level.

- Sales of electrical and household goods are over 8% above their February level.

- In contrast, sales of textiles, clothing, and footwear fell sharply in October (-2.8% m/m) for the second straight month and are over 9% below their February level (see first chart below) despite a strong rebound between May and July.

- With the introduction of a vaccine against COVID-19 now on the horizon, consumer spending prospects for later in 2021 are looking more positive, particularly given the surge in household savings rates since the pandemic struck.

- However, near-term prospects for consumer spending will be hindered by more stringent containment measures, with consumer sentiment having weakened markedly already, indicative of a correction in retail sales growth

- Porsche has signed a development joint venture (JV) with Siemens Energy and a number of other partners to build the world's first integrated, commercial, industrial-scale plant for making synthetic climate-neutral fuels (e-fuels), according to a company statement. The project will be based in Chile and in its pilot phase, around 130,000 liters of e-fuels will be produced as early as 2022. In two further phases, capacity is then to be increased to about 55 million liters of e-fuels a year by 2024, and around 550 million liters of e-fuels by 2026. Porsche will be the primary customer for the green fuel. Other partners in the project are the energy firm AME and the petroleum company ENAP from Chile and Italian energy company Enel. Porsche CEO Oliver Blume said, "Electromobility is a top priority at Porsche. E-fuels for cars are a worthwhile complement to that - if they're produced in parts of the world where a surplus of sustainable energy is available. They are an additional element on the road to decarbonization. Their advantages lie in their ease of application: e-fuels can be used in combustion engines and plug-in hybrids, and can make use of the existing network of filling stations. By using them, we can make a further contribution toward protecting the climate." This is an exciting development; if the consortium can find a way to manufacture e-fuels that are climate-neutral on an industrial scale, such a technology has the potential to be a long-term disruptor to the electrification of the industry, especially in the case with high-performance cars, supercars and hypercars. Despite the plethora of electric hypercars that are being developed such as the Lotus Evija and the Rimac C_Two, these cars have one potentially glaring drawback. If the driver regularly accesses the potential performance and drives the car hard on track or on the road, the range will shrink rapidly, as battery power decreases exponentially the higher the load. So the harder these cars are driven, the shorter the range will be. This is also the case with conventional ICE cars, but not to the same extent. (IHS Markit AutoIntelligence's Tim Urquhart)

- MAN Energy Solutions and Aker Carbon Capture have signed a technology-cooperation agreement to develop energy-efficient compression solutions for carbon capture and storage (CCS) applications with heat recovery. The agreement supports the companies' joint target to reduce the cost of removing CO2 emissions from industrial plants. The cooperation builds on MAN Energy Solutions' experience in compressor technology, the integration of system components and their design and delivery, as well as Aker Carbon Capture's proprietary amine technology and efficient carbon-capture process design. With CCS, captured CO2 is compressed before being liquefied and transported to a permanent-storage location. The two companies aim to develop carbon capture solutions that require less energy. The transfer of heat is key for CO2-capture plants' improved, overall power-consumption with MAN Energy Solutions able to recover heat from its compression systems. Hence, the steam generated will cover nearly 50% of the power demand for Aker Carbon Capture's capture plant. The technology-cooperation agreement will run for seven years and forms the basis for project deliveries to carbon-capture plants. Solutions will be applicable for large facilities, such as the Heidelberg Cement Norcem cement plant in Brevik, Norway where Aker Carbon Capture will deliver a carbon-capture plant using its patented and HSE-friendly CCS technology. The project is subject to parliamentary approval of the funding. (IHS Markit Upstream Costs and Technology's Kamila Langklep)

- The RABus project will operate autonomous buses in regular urban road traffic in the German state of Baden-Württemberg, reports Intelligent Transport. The project, which has received EUR7 million (USD8.5 million) from the State Ministry of Transport, will test these vehicles in public passenger transit in the cities of Mannheim and Friedrichshafen. RABus is a consortium with members including the Research Institute of Automotive Engineering and Vehicle Engines Stuttgart (FKFS), Karlsruhe Institute of Technology (KIT), Rhein-Neckar-Verkehr GmbH, Stadtverkehr Friedrichshafen GmbH with DB ZugBus Regionalverkehr Alb-Bodensee GmbH, and ZF Friedrichshafen AG. The buses are manufactured by 2getthere, a subsidiary of ZF Friedrichshafen AG, and can accommodate up to 22 people and have compact dimensions of 6 × 2.1 × 2.8 m. In Mannheim, the focus of testing will be on mixed inner-city traffic in a new urban quarter, while that in Friedrichshafen will focus on interurban operation. In both cities, a public transport system with electrified and automated vehicles is expected to be established by the end of 2023. These trials will support Germany's efforts to put cars with partial autonomy on roads from 2022. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- France's Agriculture Minister Julien Denormandie said the

country's dependency on protein imports is "too high" and the

10-year strategy is needed to develop alternatives. "It is

imperative that we regain agri-food sovereignty, and this cannot be

done without the development of a French production of plant

proteins," he said. (IHS Markit Food and Agricultural Policy's

Steve Gillman)

- France is one of the EU's largest agri-food exporters, but the country still imports a lot of plant proteins for both animal and human consumption. According to the government, the nation produces only half of the protein-rich materials needed to feed its animals, such as soybeans and rapeseed.

- Over €100 million will be dedicated to the protein plan to help address France's import dependency. The money will be spent across three main objectives - reducing environmental impact, increasing self-sufficiency and creating new market opportunities.

- The ministry's rationale is that the country's imports of soybeans from third countries may be responsible for deforestation while domestic plant protein production could reduce French farmers' environmental footprint and increase the livestock sector's sustainability. The strategy also wants farmers to grow more legumes because it could capture more nitrogen in the ground and enrich soils, making them more productive.

- The French government believes this approach will also create new opportunities for its farmers and enable them to respond to new markets, such as the growing demand for plant-based alternatives, while reducing food producers' exposure to fluctuating world soybean prices.

- There is also a 2030 target to reduce fertilizer use by 20% across the bloc. The Commission hopes to see more rotational crops, such as legumes, grown in member states because it can support this F2F target by preventing excess nutrients, like nitrogen, from polluting the environment.

- Portuguese passenger car registrations suffered a further fall during November. According to data published by the Automobile Trade Association of Portugal (Associação do Comércio Automóvel de Portugal: ACAP), passenger car registrations decreased by 27.9% year on year (y/y) to 11,826 units last month. Passenger car registrations in the year to date (YTD) are down by 36.4% y/y at 131,165 units. The ACAP added that light commercial vehicle (LCV) registrations dipped by 1.4% y/y to 2,801 units in November, with the YTD figure at 23,905 units, down 29.5% y/y. Medium and heavy commercial vehicle (MHCV) registrations dropped by 17.5% y/y to 342 units in November, with the YTD figure at 3,632 units, down 29.4% y/y. Although the Portuguese light-vehicle market had been expected to retreat during 2020 following a period of strong growth, the impact of the COVID-19 virus pandemic and the measures designed to prevent its spread were hugely detrimental to the market in the first half of the year. Furthermore, the market remains sluggish in the second half. The ACAP has previously said that the situation is not being helped by the Portuguese government's decision not to include support measures in the 2021 budget proposals. (IHS Markit AutoIntelligence's Ian Fletcher)

- As expected, the National Bank of Poland's (NBP)'s monetary

policy council kept the policy interest rate unchanged at a

historical low of 0.1% during its session on 2 December, amid a

rebound in third-quarter economic growth and a moderation of

inflation. Although the government had hoped to rebuild the economy

through investment rather than consumption, household demand

rebounded sharply in the third quarter, while fixed investment

remained far below year-earlier levels. (IHS Markit Economist

Sharon Fisher)

- The increase in consumption was also apparent in the real estate market. Although growth in housing loans decelerated to 6.0% year on year (y/y) in the third quarter, residential real estate prices surged by 14.0% y/y, according to Poland's Central Statistical Office.

- Despite low interest rates, short-term risks to both consumption and investment are heightening owing to the second-wave COVID-19 restrictions in Poland and elsewhere in Europe. Services will be hit especially hard, triggering another quarter-on-quarter (q/q) contraction in GDP during the fourth quarter, despite fiscal and monetary measures aimed at boosting the economy.

- According to the NBP, the pace of the recovery may also be reduced by the lack of a more visible and durable exchange-rate adjustment of the zloty. In November, the monthly average exchange rate appreciated to PLN4.50/EUR1.00 but was 4.9% weaker than the year-earlier level.

- The IHS Markit purchasing managers' index (PMI) for manufacturing remained stable at 50.8 points in November; however, the output and new orders indices stood in contractionary territory, with negative implications for short-term growth in industrial production and exports.

- On the inflation front, consumer prices rose a preliminary 3.0% y/y in November (slightly below the October figure), with flat month-on-month (m/m) growth. Food prices fell by 0.1% m/m, while utility and fuel costs increased by 0.1% and 0.2% m/m, respectively.

- Inflation is projected to slow into 2021, although a potential revival of global commodity prices, strengthening economic activity, a weaker zloty, and rising administrative prices present upside risks. A capacity fee will be added to household electricity bills from the start of 2021.

- The International Monetary Fund (IMF)'s first review of

Somalia's three-year staff-monitored program in November suggests

debt relief advancements, while natural disasters and the COVID-19

pandemic contributed to an economic shock in 2020. (IHS Markit

Economist Alisa Strobel)

- The IMF on 30 November announced its approval of an immediate disbursement of USD10 million as part of the Extended Credit Facility (ECF) arrangement with Somalia, following a first review. Following the achievement of the Heavily Indebted Poor Countries (HIPC) initiative decision point, representatives of the Paris Club creditor countries and the government of Somalia agreed to restructure Somalia's external public debt.

- The IMF stated that Somalia's performance under the ECF arrangement has been broadly satisfactory despite the significant challenges the economy faced in 2020. The IMF's official statement highlights that prompt action by the Somalian government and support from the international community has helped mitigate the impact of the latest natural-disaster events and the COVID-19 pandemic. Nevertheless, these shocks have had a significant impact on Somalia's economic activity, exports, and domestic fiscal revenues, leading to a contraction in real GDP.

- IHS Markit projects Somalia's economy to grow at an average 2.8% annually in the near term (2021-23) given the prevailing headwinds, after contracting 2% in 2020. Drought conditions and security concerns have added to the economic and humanitarian hardships in Somalia in the past year and they are expected to continue to hinder growth prospects in the remainder of 2020 and into 2021.

- Furthermore, the COVID-19 pandemic is expected to have impacted Somalia's fiscal revenues negatively, in tandem with a drop in international travel dragging on the transportation sector's revenues, as well as delays in implementing the new licensing and regulatory framework for the telecommunications sector.

- We expect that Somalia's government will strive to align with IMF requirements to strengthen domestic revenue mobilization to create fiscal space for priority spending under the ninth National Development Plan. Fiscal consolidation improved prior to the global outbreak of the COVID-19 virus. Domestic revenue in 2019 reached USD230 million, up from USD183 million in 2018.

Asia-Pacific

- APAC equity markets closed mixed; South Korea +0.8%, Hong Kong +0.7%, Australia +0.4%, India/Japan flat, and Mainland China -0.2%.

- US Customs and Border Patrol at all US points of entry will

detail shipments of cotton and cotton products originating from the

Xinjian Production and Construction Corps (XPCC) via a Withhold

Release Order (WRO) based on information that "reasonably indicates

the use of forced labor, including convict labor," according to a

statement from the Department of Homeland Security (DHS). (IHS

Markit Food and Agricultural Policy's Roger Bernard)

- The agency said the order applies to "all cotton and cotton products produced by the XPCC and its subordinate and affiliated entities as well as any products that are made in whole or in part with or derived from that cotton, such as apparel, garments, and textiles." This marks the sixth action taken by the Trump administration's CBP relative to goods made by forced labor in the Xinjiang Uyghur Autonomous Region, DHS said.

- DHS Acting Deputy Secretary ken Cuccinelli said, the action was to make sure that those who are abuse human rights "are not allowed to manipulate our system in order to profit from slave labor. 'Made in China' is not just a country of origin it is a warning label." He also said that the action could affect "billions of dollars" of imports when the action scales up.

- The administration in early July announced issued a Xinjiang Supply Chain Business Advisory and the Department of Treasury July 11 announced that it had sanctioned XPCC and prohibited doing business directly with XPCC.

- China's Xinjiang produces 85% of China's cotton and DHS said that the actions thus far are not a region-wide blockade on cotton products from Xinjiang. But Cuccinelli said that XPCC is so prevalent in the region's economy that blocking products from the firm will be similar to a region-wide ban. "It is so massive that even though it appears that it's a single company, from our perspective it is equivalent to a regional WRO," Cuccinelli said.

- XPCC employs 12% of the Xinjian population and produces 17% of its cotton products. This is potentially one of the additional actions on China that the administration signaled were being looked at and could be announced yet before the administration leaves office.

- AutoX has started fully driverless vehicle testing in Shenzen, China, reports TechCrunch. The company claims to be the first in the country to conduct autonomous car testing without safety drivers or remote operators on public roads and has deployed a fleet of 25 unmanned vehicles in the city. An unidentified spokesperson of AutoX said, "We have obtained support from the local government. Shenzhen is making a lot of rapid progress on legislation for self-driving cars." AutoX has also received permit to test its autonomous cars without a human safety driver in California. The company recently launched a robotaxi service for the public in Shanghai after conducting trials with signed-up users. It has also set up an 80,000-square-foot facility for autonomous vehicle operations in Shanghai and has partnered with electric vehicle manufacturer NEVS to conduct a large-scale trial of robotaxis in Europe by the end of 2020. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- According to statistics from financial statements for the third

quarter of 2020, released on 1 December, sales for all of Japan's

industrial sectors, excluding finance and insurance, rose by 3.8%

quarter on quarter (q/q) for the first increase in five quarters,

and the year-on-year (y/y) contraction narrowed to 11.5%. (IHS

Markit Economist Harumi Taguchi)

- Sales of real estate and the production, transmission, and distribution of electricity turned positive y/y and decreases of sales in the majority of industry groups softened thanks to the resumption of economic activity.

- Double-digit contractions continued for a broad range of industry groupings, particularly for petroleum and coal products, iron and steel, production and business machinery, and services.

- Ordinary profits also rose by 33.7% q/q and the y/y contraction narrowed to 28.4% from 46.6% y/y in the previous quarter. The softer y/y decline in ordinary profits reflected increases in profits for petroleum and coal products, metal products, real estate, and the production, transmission, and distribution of electricity. However, overall ordinary profits remained sluggish, particularly for transport and postal services, services, and iron and steel.

- While lower sales were the major reason for a sharp drop in ordinary profits, the weakness was partially offset by lower payroll costs, which declined by 5.0% y/y, although the contraction in the number of employees softened to 2.9% y/y from 6.6% y/y in the previous quarter.

- Investment in plant and equipment (including software) fell by 1.2% q/q and 10.6% y/y under the continued difficult business conditions. Although investment continued to increase in the information and communication equipment, construction, and petroleum and coal groupings, eroded cash flows led to continued declines in fixed investment for a broader range of industry groupings, particularly for metal products, general-purpose machinery, electric machinery, and goods leasing.

- The September results suggest that upside for sales and ordinary profits from the resumption of economic activity has bottomed, and that broad areas of the industry continue to struggle with weak demand. The 1.2% q/q drop in investment in plant and equipment signals a slight upward revision of private capital investment in the third quarter (which will be released on 8 December).

- Sluggish cash flows could weigh on the recovery in fixed investment, even though a rebound in manufacturers' shipment in capital goods in October pointed to stronger fixed investment.

- Southeast Asia's ride-hailing companies Grab and Gojek are reportedly in advanced talks on a deal to combine their businesses. The report by Bloomberg cites that the final details of the deal are being worked out among the most senior leaders of both the companies with the participation of Masayoshi Son of SoftBank, a major investor in Grab. The merger would result in Anthony Tan, co-founder of Grab, becoming CEO of the combined company, with Gojek executives handling the combined business in Indonesia. According to the report, the brands may be run separately for an undetermined amount of time and the aim of this merger is at becoming a publicly listed company. The talks are still ongoing and may not result in a transaction as the deal needs to get regulatory approval and address antitrust concerns. The companies have been in a fierce battle for dominance in Southeast Asia for several years. Grab, which is present in eight countries, was valued at more than USD14 billion, while Gojek has a presence in five countries and was valued at USD10 billion. They began initial discussions about a merger in February as investors have been pushing them to join forces in order to reduce cash burn. The merger deal is expected to significantly accelerate both the companies' paths to profitability, as ride-hailing demand has been battered by the COVID-19 virus pandemic. (IHS Markit Automotive Mobility)

- The Australian economy expanded 3.3% in seasonally adjusted

quarter-on-quarter (q/q) terms during the September (third) quarter

thanks to consumers and government stimulus spending, while exports

were a drag on growth. The day prior to the GDP release, the

Reserve Bank of Australia announced that it would keep its

expansionary monetary policy settings unchanged. (IHS Markit

Economist Bree Neff)

- The September-quarter expansion was stronger than market expectations, given that the country's second largest state economy - Victoria - was under lockdown for the entirety of the quarter. But consumers in other states came out of their COVID-19-related lockdown/containment measures with significant pent up demand, which explains why private consumption expanded in real, inflation-adjusted terms at the fastest pace on record and contributed 4.0 percentage points to quarterly GDP during the quarter, according to the Australian Bureau of Statistics (ABS).

- The increases in private consumption spending were broad-based and often achieved double-digit growth in real q/q terms, with consumers only reining in their spending on three categories: cigarettes and tobacco (down 0.9% q/q), alcoholic beverages (down 0.5% q/q), and household furnishings (down 0.9% q/q), with both alcoholic beverages and household furnishing recording robust growth in the June quarter.

- Meanwhile, the increase in public consumption spending arose primarily from the national government's non-defense spending, largely tied to fiscal support measures such as the Jobkeeper program and support for small and medium-sized enterprises (SMEs). Government fixed capital formation spending made no significant contribution to growth during the quarter, because increased investment in national defense and by public corporations were offset by reduced investment spending by state and local governments.

- Private-sector fixed capital formation spending also had little impact on growth during the September quarter. There was a 5.1% q/q surge in dwelling alterations and additions, which pushed dwelling construction up 0.6% q/q - the first quarterly expansion in two years. However, the non-dwelling construction slump worsened, as investment in this category fell by another 4.9% q/q after falling 2.4% during the June quarter. Investment into machinery and equipment also fell for a second consecutive quarter - this time by 3.7% q/q - marking an improvement from the June quarter's 8.2% q/q plunge.

- The net export position was the primary source of drag on the Australian economy in the September quarter, detracting 1.9 percentage points from growth as imports recovered and exports slumped. According to the ABS's balance-of-payments publication, the recovery in real imports was led by consumer goods, including a 48% q/q surge in motor vehicle imports, and double-digit increases for household electrics, toys, and leisure goods, as well as textiles and apparel. Services imports also rose 4.4% q/q in real terms, with indications that some of this was driven by financial services.

- The unwinding of the Victoria state lockdown measures in October will provide some uplift to the current quarter's expansion - as will data indicating continued growth in single-family dwelling building approvals, which according to the ABS reached a 20-year high in October. On the downside, some of this could be mitigated by ongoing tensions between China and Australia that are causing disruptions to Australian exports to its top export market. In any case, the September-quarter result was stronger than IHS Markit's expectations, and we will be upgrading the country's GDP forecast for 2020 closer to the low -3% range from -4.0% previously as part of our December forecast update.

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-3-december-2020.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-3-december-2020.html&text=Daily+Global+Market+Summary+-+3+December+2020+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-3-december-2020.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - 3 December 2020 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-3-december-2020.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+3+December+2020+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-3-december-2020.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}