Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

CHEMICAL WEEK

Dec 04, 2020

Daily Global Market Summary - 4 December 2020

European and US equity markets closed higher, while Japan was the only major APAC market to close lower in that region. US and European government bonds closed lower, while European iTraxx and CDX-NA were tighter across IG and high yield. Gold was lower, silver/oil higher, and copper closed higher and broke through another multiyear high again. The US Congress is beginning to accelerate its effort to pass a more modestly sized stimulus package before year end, as a combination of today's weaker than expected US employment report and the rapidly growing number of COVID-19 hospitalizations is reinforcing the sense of urgency to support the economy.

Americas

- US equity markets closed higher and with every major index reaching a new record high close today; Russell 2000 +2.4%, S&P 500 +0.9%, DJIA +0.8%, and Nasdaq +0.7%.

- 10yr US govt bonds closed +6bps/0.97% yield and 30yr bonds +8bps/1.74% yield.

- CDX-NAIG closed flat/50bps and CDX-NAHY -9bps/291bps, which is

-1bp and -16bps week-over-week, respectively.

- DXY US dollar index closed +0.1%/90.81.

- Copper closed $3.52 per pound, which is the highest price since March 2013.

- Gold closed -0.1%/$1,840 per ounce and silver +0.5%/$24.25 per ounce.

- Crude oil closed +1.4%/$46.26 per barrel.

- The United States saw record numbers of newly reported COVID-19 cases yesterday (3 December), with the total reaching 217,664, and deaths, which amounted to 2,879 (based on data compiled by Johns Hopkins University). The independent COVID Tracking Project reports also that 3 December had the largest number of hospitalizations over the course of a day since the beginning of the pandemic, with 100,667; each day of this week has seen new record for hospitalizations, according to this source. Predictions for the coming weeks are gloomy. Dr Jonathan Reiner, a professor of medicine at George Washington University, has been quoted by CNN as saying that he expects the daily new case numbers to be over 3,000 by next week, describing this figure as "9/11 every single day". Associated Press has reported, based on figures from transport analytics provider StreetLight Data, that there was a surge in vehicle travel on the roads around the Thanksgiving holiday; in early November, the volume was 20% below the equivalent period of 2019, but on Thanksgiving day, it was just 5% lower. A similar trend was observed in air travel. There is concern that similar trends will be observed around the upcoming Christmas and New Year celebrations, which is expected to contribute to persistent high infection and death rates. (IHS Markit Life Sciences' Janet Beal and Brendan Melck)

- US nonfarm payroll employment rose 245,000 in November, short

of consensus expectations. Revisions to prior months were mixed.

The unemployment rate declined 0.2 percentage point to 6.7%. (IHS

Markit Economists Ben Herzon and Michael Konidaris)

- The recovery in payroll employment is continuing to lose steam, with the level of employment still well short of the pre-pandemic peak; the count of payrolls in November was roughly 10 million below February.

- The shortfall in payroll employment (relative to February) is largely in private services (still down roughly 8 million), although both government and private goods-sector payrolls are also down considerably (by roughly 1 million each).

- The continued weakness in private services is widespread, with leisure and hospitality still down 3.4 million from February.

- As the rate of spread of COVID-19 cases has risen, and as state and local governments have continued to tighten containment efforts, services employment will continue to struggle heading into winter months.

- Government payrolls declined 99,000 in November, nearly fully accounted for by the continued winding down of temporary Census 2020 employment, which is nearly complete. As of November, the count of these temporary jobs was just 6,000.

- The decline in the unemployment rate in November was driven by a 400,000-person decline in the civilian labor force; civilian employment posted a smaller, 74,000 decline.

- In the months ahead, the trajectory of employment will hinge on the trajectory of new COVID-19 cases and how both consumers and government officials respond.

- Fears of a faltering US recovery have energized talks on a new fiscal stimulus package in Congress, marking a shift in the political dynamic in Washington that could bring some relief to the global economy. Republicans and Democrats on Capitol Hill on Friday signaled their willingness to compromise on a plan to inject hundreds of billions of dollars — and possibly up to $1 trillion — into the world's largest economy with a deal before the end of the year. (FT)

- US manufacturers' orders and shipments each rose 1.0% in

October. After sharp increases over May, June, and July, the pace

of recovery in orders and shipments has slowed considerably. (IHS

Markit Economists Ben Herzon and Lawrence Nelson)

- Orders and shipments of nondefense capital goods excluding aircraft were revised higher through October, while manufacturers' inventories rose 0.2% in October, more than we had assumed.

- The details in this report that bear on our GDP tracking added 0.1 percentage point to our forecast of fourth-quarter GDP growth, which now stands at 6.3%.

- The recovery in manufacturing has come a long way, but remains shy of full recovery. Orders are now 3.2% below the February level and shipments are 1.8% below the February level. In April, both were in the ballpark of 20% down.

- That manufacturing has fared well in the recovery reflects favorable performance in the demand for goods relative to services.

- By our estimates, US GDP of goods has fully reversed the pandemic-induced decline, while GDP of services is still lagging.

- A particularly bright spot in the goods sector is in capital equipment. Both orders and shipments of core capital goods have surpassed their February levels by far, suggesting a robust fourth quarter for equipment spending.

- Such a recovery likely would not be possible were it not for businesses' optimism about the course of the recovery.

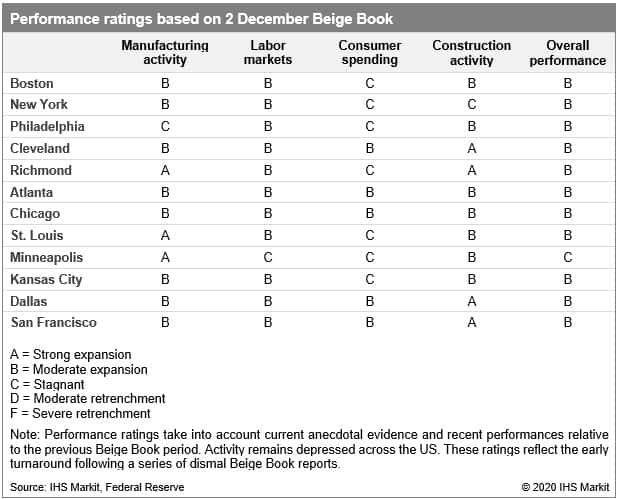

- While the recovery continued in many parts of the country from

October to early November, areas of Pennsylvania and a large swath

of the Midwest saw growth begin to erode according to the US

Federal Reserve's latest Beige Book report, containing anecdotal

information from regional business contacts. Rising COVID-19 cases

and hospitalizations in the Upper Midwest south to Missouri and

Arkansas dented the rebound in consumer spending and restrained

employment gains among hospitality and services businesses. (IHS

Markit Economist James Kelly)

- Consumer spending was "mostly flat" in the Northeast as retail and restaurant sales saw slower growth in the face of rising COVID-19 caseloads and falling temperatures. As more localities in the region reimposed "safer-at-home" orders, consumers scaled back some spending. Hotels and tourism businesses remain locked into weak activity with any pickup in growth not to be seen until 2021.

- Labor markets expanded modestly in much of the country, but only slight growth was felt in the Northeast and areas of the Plains states. As COVID-19 cases began to surge again and many local and state governments reinstituted restrictions on business activity and large gatherings of people, hiring in leisure and hospitality, transportation, and tourism sectors weakened.

- Manufacturing activity continued to make strides in the Southeast and in a large area from the Upper Midwest south to Missouri. New orders and production levels increased at a robust pace in these regions as manufacturers continued to bounce back from the depressed demand and activity from the early stages of the COVID-19 pandemic. While production in the South was restrained somewhat by labor supply concerns and numerous supply chain disruptions, producers of home furnishings, textiles, food, and shipping materials saw robust demand for their products

- Construction activity made strong gains in the West, Midwest, and parts of the South. Low mortgage interest rates and the continuing trend towards remote work have pushed home demand along the West Coast higher and home inventories lower. Similar dynamics occurred in Texas and the Southeast where some builders are raising prices not only to cover rising materials costs but also to slow down sales in some areas.

- This month's Beige Book pointed to a softening of the recovery

in the Midwest and parts of the Northeast as the COVID-19 pandemic

surges on. Employment gains and consumer spending growth,

especially in the heavily impacted leisure and hospitality

industry, remain contingent on the rising or falling prevalence of

the virus in local communities. The reinstitution of business

capacity restraints and surging hospitalizations in the Midwest and

the potential for overwhelmed hospitals in other parts of the

country will limit consumer spending and hiring in the near

term.

- Peer-to-peer car-sharing company Turo is returning to New York (United States), after leaving the state seven year ago. In 2013, Turo suspended its operations in the state over a dispute with the New York Department of Financial Services about insurance laws. Starting in January, Turo will only allow users in its commercial host program, designed for independent rental companies which provide their own insurance, to list on its app in New York. Andre Haddad, CEO of Turo, said, "Frankly this couldn't come at a better time. Subway ridership is down, ride-sharing is down. Many consumers want the safety of a private space of a car and frankly New Yorkers are really saddled with the worst traditional car rental experience in the country." The limited return of Turo in New York is a significant development at a time when the car-sharing business has been battered amid the COVID-19 virus pandemic. The company is looking for partnerships with carmakers to allow dealers to rent their cars using its app. Recently, Bloomberg reported that Turo and Getaround had secured US loans because of the economic effects the COVID-19 virus pandemic on their transportation businesses. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Brazilian light-vehicle registrations declined 7.2% year on

year (y/y) in November, according to initial data from the National

Federation of Motor Vehicle Distributors (Federação Nacional da

Distribuição de Veiculos Automotores: Fenabrave). Fenabrave

reported registrations of 214,265 light vehicles last month,

compared with 230,885 units in November 2019. (IHS Markit

AutoIntelligence's Tarun Thakur)

- Registrations of medium and heavy commercial vehicles (MHCVs) and buses decreased by 5.5% y/y last month, Fenabrave's data show. In November, 10,765 MHCVs were sold, compared with 11,392 units in the same month a year earlier.

- The best-selling automaker in the Brazilian light-vehicle market, Fiat Chrysler Automobiles (FCA), had a market share of 18.4% in November. General Motors (GM) and Volkswagen (VW) claimed second and third places with shares of 18.3% and 16% respectively.

- Fenabrave reported that the GM Onix was the best-selling passenger car in Brazil last month, with 14,292 units registered.

- The Fiat Strada pick-up was the best-selling commercial vehicle, with 9,614 units registered in November.

- While reporting their third-quarter earnings, separately, GM and FCA highlighted these two models as being significant for their respective performances in the region.

- IHS Markit's November forecast shows a decline of 28.3% in Brazilian light-vehicle sales to 1.91 million units in 2020.

- IHS Markit reduced its forecast because of the expected impact that the COVID-19 virus outbreak will have on vehicle demand in 2020.

- Demand for personal vehicles during the pandemic (for safer mobility), accessible vehicle finance, and the low Selic interest rate are some of the factors that are affecting Brazilian vehicle sales positively.

- We expect double-digit percentage growth in the coming years as the Brazilian market recovers and we forecast annual sales of 3.07 million units in 2025.

- Hyosung (Seoul, South Korea) says it will invest $36 million to

almost double existing production capacity at its spandex fiber

plant in Santa Catarina, Brazil. (IHS Markit Chemical Advisory)

- The 10,000-metric tons/year capacity expansion for the facility in southern Brazil will be completed by December 2021, raising the plant's total capacity to 22,000 metric tons/year, it says. The capacity hike will help to meet a "rapid rise" in demand for the synthetic fiber in the Americas, it says.

- "In the Brazilian market, the import tariff rate for spandex is as high as 18%, which is more than double the rate applied in other regions. Therefore, a local production base is essential for maintaining price competitiveness," according to Hyosung. Brazil's location is also advantageous for export to nearby countries, it says. The company first established a production base in Brazil in 2011 and currently holds a market share in Brazil of 65%.

- Hyosung, the world's leading producer of spandex, also says it decided in November to invest 60 billion South Korean won ($55 million) to expand production capacity at its existing 25,000-metric tons/year spandex plant in Turkey to target the market in Europe. The expansion will be completed by the third quarter of 2021 and raise the plant's capacity to 40,000 metric tons/year.

- The company produces approximately 340,000 metric tons/year of spandex fiber, one-third of current global demand.

Europe/Middle East/Africa

- European equity markets closed higher across the region; Spain +1.5%, UK +0.9%, France +0.6%, and Germany +0.4%.

- 10Yr European govt bonds closed lower; UK +3bps, Italy +2bps, and Germany/France/Spain +1bp.

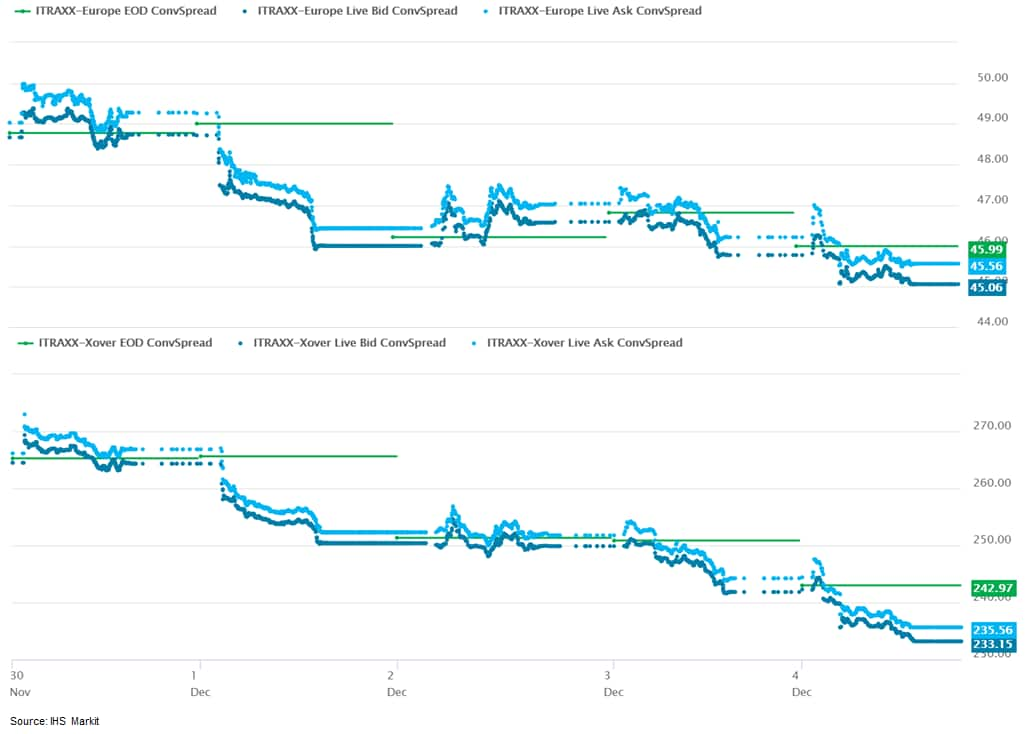

- iTraxx-Europe closed -1bp/45bps and iTraxx-Xover -9bps/234bps,

which is -4bps and -31bp week-over-week, respectively.

- Brent crude closed +1.1%/$49.25 per barrel.

- Members of the European Parliament's Environment Committee have urged EU member states to reduce the use of pesticides and have called for the targets to be incorporated into EU policies on farm subsidies and water protection. The call comes in a resolution on the implementation of water legislation. This was voted through at the same time as the Committee approved draft rules on drinking water that were informally agreed between MEPs and EU Ministers at the end of 2019. The resolution stresses the need to align the Common Agricultural Policy (CAP) with water rules regarding the need for increased water protection measures. In the Committee vote, MEPs amended the original text to strengthen demands for member states to integrate and implement pesticide reduction targets in their CAP strategic plans. There is an "urgent need" to reduce the impact of pesticides on drinking water resources by "fully addressing" water protection in the approval and renewal of active ingredients and products. The resolution also urges the European Commission to improve monitoring systems for collecting data on pesticide residues in water. The draft drinking water rules agreed in 2019 will tighten maximum limits for certain pollutants in water. They still have to be formally approved by the European Parliament and EU Ministers before they can come into force. Under the current system, maximum concentration limits in water are set for "priority substances" and stronger measures to stop releases to water for "priority hazardous substances". Several pesticides are on these lists of substances. However, the operation of the lists and their effectiveness require improvement and the Commission issued a roadmap earlier this year outlining its plan to revise the system. (IHS Markit Crop Science's Jackie Bird)

- The IHS Markit/CIPS UK PMI surveys showed service sector activity falling back into decline in November as a second lockdown to fight a resurgent wave of COVID-19 infections hit many businesses, especially consumer-facing firms in areas such as hospitality. More encouragingly, manufacturing and construction output continued to rise, and growth even accelerated slightly in both cases compared to that seen in October. Moreover, the decline seen in the service sector was far less severe than suffered earlier in the year, at the height of the lockdowns amid the first virus wave. The overall situation was therefore one in which the upturns in manufacturing and construction almost entirely offset the downturn recorded in the services sector, resulting in only a modest overall drop in output. The all-sector IHS Markit/CIPS PMI output index, which is a GDP weighted composite of the indices from the three sectors, merely fell from 52.2 in October to 49.5 in November. With any reading below 50 indicating contraction, the PMI still points to the UK economy having fallen into decline in November, but the impact of the lockdowns appears to have been far less severe than earlier in the year. Note that this index fell to 36.3 in March and slumped as low as 13.4 in April. Some caution is warranted in interpreting what the PMI signals for GDP during lockdowns, not least because the PMI coverage excludes retail. GDP fell far more sharply than indicated by the PMI in the second quarter, and also rebounded more markedly than the PMI signalled in the third quarter. The PMI may therefore potentially once again understate the fall in GDP seen during the November lockdown to some degree. However, the relative resilience of the all-sector PMI in November provides a strong signal that GDP will decline by much less than earlier in the year. (IHS Markit Economist Chris Williamson)

- UK passenger car registrations have dropped by 27.4% y/y during November due to the introduction of coronavirus disease 2019 (COVID-19) virus-related lockdown measures in England through most of the month. According to the Society of Motor Manufacturers and Traders (SMMT), registrations fell to 113,781 units, from 156,621 units in November 2019. There were steep declines across all customers types during the month. Fleet registrations were the least affected with a fall of 22.1% y/y to 67,730 units, while private registrations dropped by 32.2% y/y to 44,180 units. Registrations among business customers tumbled by 58.6% y/y to 1,871 units. (IHS Markit AutoIntelligence's Ian Fletcher)

- The UK competition regulator, the Competition and Markets Authority (CMA), has said that it will investigate the market for battery electric vehicle (BEV) charging points. In a statement, the organization said that its investigation will cover two broad themes. The first will be "how to develop a competitive sector while also attracting private investment to help the sector grow," while the second will be "how to ensure people using electric vehicle chargepoints have confidence that they can get the best out of the service". Andrea Coscelli, the chief executive of the CMA, said, "Making the switch to electric vehicles is key to helping the UK become greener, which is why it's so important that everyone has the confidence to get behind the move. Being able to easily stop off at a petrol station is a standard part of a journey and consumers must trust that electric chargepoints will provide a similarly straight-forward service. By getting involved early as electric vehicles and chargepoints are still developing, the CMA can make sure consumers are treated fairly now and in the future." (IHS Markit AutoIntelligence's Ian Fletcher)

- The German passenger car market posted a 3.0% year-on-year (y/y) decline in registrations in November to a figure of 290,150 units, according to the latest data released by the Federal Motor Transport Authority (KBA). This left the market at 2,606,284 registrations for the first 10 months of the year, which was a decline of 21.6% in the year to date (YTD) after the heavy declines in the first half of the year as a result of the initial impact of the COVID-19 virus pandemic. The most notable issue in November was a very significant disparity between the private registrations, which were up by 22.8% y/y, giving them an unusually high market share of 39.4%. At the same time, commercial registrations fell by 14.7% y/y. This is an interesting development and it has been fueled by private buyers piling into the market to take advantage of the cut in VAT from 19% to 16% and on the generous subsidies on full battery electric vehicles (BEV). Dealers seem to be backing off from registering vehicles over short-and-medium-term uncertainty. There was a massive disparity between private and business registrations in November, with private registrations reaching nearly 40% during the month, which is a nearly unheard of amount. As mentioned above, the VAT rate will have made a positive impact on this, with private buyers seeing a tangible saving from this. The subsidies on battery electric vehicles (BEVs) and plug-in hybrid EVs (PHEVs) will have had an even more positive impact. (IHS Markit AutoIntelligence's Tim Urquhart)

- Bosch has reduced its stake in electric vehicle (EV) company Nikola from 6.9% to 4.9%, according to media reports, citing a US regulatory filing. Bloomberg reports that Bosch's stake in Nikola was reported as 6.9% as of 15 June 2020. The report quotes a Bosch spokesperson as saying, "Our initial investment was primarily meant to support the development of hydrogen technology. The reduction of some of our shares in Nikola took place after a holding period under stock-exchange regulation." Nikola provided no comment on the matter, according to the report. There had been selling restrictions in place, following the expiry of which a block of shares equivalent of 1.9% of the company was traded on the New York Stock Exchange opening at 9:30 Eastern time on 3 December, reports Bloomberg. (IHS Markit AutoIntelligence's Stephanie Brinley)

- The impact on Italy's labor market from the COVID-19 virus

pandemic has been less severe than expected during the crisis. A

major factor has been the Italian government's short-time work or

temporary layoff scheme measures, which have reduced the scale of

job destruction during the pandemic. (IHS Markit Economist Raj

Badiani)

- Total employment was broadly stable at 22.843 million in October (see first chart below). Therefore, cumulative job losses in March to October stood at 424,000, or 1.8% lower when compared with February 2020, the pre-pandemic level.

- The unemployment rate rose slightly to 9.8% in October (from 9.7% in September). The number of unemployed people increased by 11,000 to 2.479 million in October after falling back in the previous two months.

- The labor force was unchanged at 25.3 million in October, with the activity rate stable at 64.5%.

- The inactivity rate increased from 29.7% in September to 30.3% in October. It appears that some laid-off workers stopped their job searching after the Italian government tightened its COVID-19 containment measures from mid-October. They included restaurants closing at midnight, and bars shutting at 6 pm unless they can offer seated service.

- The employment losses have been less severe than expected during the pandemic, with the country's short-time work or temporary layoff schemes helping to shore up employment levels. In addition, the demand for labour probably enjoyed some support from a stronger-than-expected economic rebound during the third quarter, with the national statistical office reporting that GDP increased by 16.1% quarter on quarter (q/q).

- A major support to employment has been the expansion to the Cassa Integrazione Ordinaria, or the Support of Salary Payment by the state. An employer can suspend or reduce work activity for events related to the COVID-19 virus and enjoy social contribution exemption. Importantly, firms have to maintain their workforces to qualify for state aid.

- The European Central Bank estimates that some 8.5 million workers, or 44% of Italian employees, were on these schemes during the lockdown in Italy. In August, the government agreed to extend the short-time work scheme until the end of 2020.

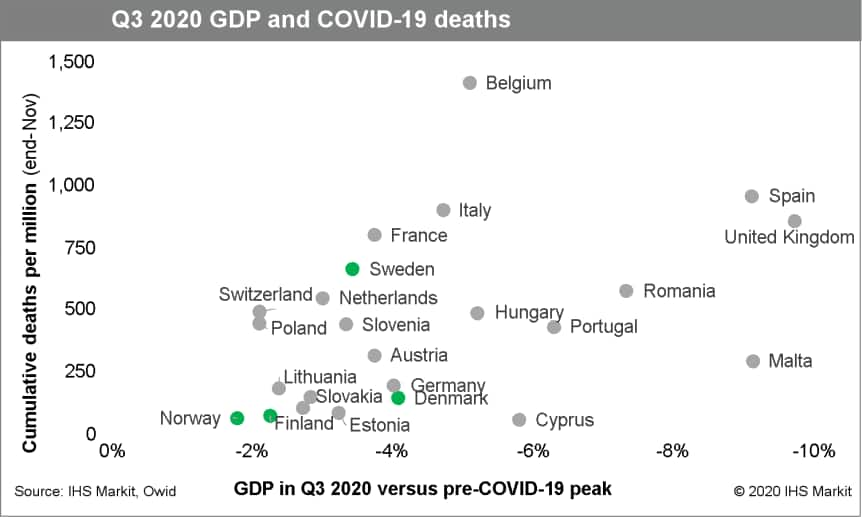

- The Scandinavian economies of Sweden, Denmark, Norway, and

Finland have been less affected by the COVID-19 virus than the rest

of Europe and experienced among the strongest, although still

partial, rebounds in the third quarter. Their GDP declines in the

first half of the year was the lowest in Europe and the subsequent

rebound in the third quarter has put them at or near the top of the

table in output relative to the pre-COVID-19 virus peak. Among the

four, the largest drop in the first half of the year was in Denmark

(-8.5%), followed by Sweden (-7.6%), with the latter being the only

economy in Europe recording positive growth in the first quarter.

By the third quarter, the economies of Norway and Finland were

around 2% smaller than prior to the pandemic, making them the top

performers in Europe along with Switzerland and Poland. (IHS Markit

Economist Daniel Kral)

- On a cumulative basis, which matters most for full-year averages, in the first nine months of 2020 Norway's economy was just 1.5% smaller than in the first nine months of 2019, followed by Poland (-2.6%) and Sweden (-3.1%). Finland (-3.5%) and Denmark (-4.1%) are also among Europe's better performers, recording significantly lower drops than the eurozone (-7.5%). On top of their relative economic outperformance, Norway, Finland, and Denmark recorded among the lowest number of COVID-19 deaths per capita in Europe, indicating strong complementarity between a successful health and economic response. Sweden has pursued a different health strategy, never imposing a lockdown but instead relying on voluntary behavioral changes. This has resulted in significantly more deaths in the country than among its Nordic peers without any noticeable benefit for the economy.

- The key factor in the relative economic outperformance of Denmark, Norway, and Finland has been the early containment of the COVID-19 virus pandemic, allowing a relatively quick lifting of restrictions. For example, Denmark was among the first European countries to impose a national lockdown on 16 March and the first country to start lifting restrictions already in mid-April. The scaling up of testing and generous support for those needing to self-isolate were key components of the national containment strategies. As of early December, Denmark has tested more than 60% of its population for COVID-19 with PCR tests. High levels of trust in the government resulted in compliance with social distancing requirements and restrictions, further limiting the spread of the virus.

- Both the decline in the first half of 2020 and rebounds in the third quarter were broad-based. However, in all four economies, following significant drops in the first half of 2020, private consumption remains significantly lower than overall GDP compared with pre-COVID-19 virus peaks. Other components were the main contributors to the outperformance - fixed investment in Denmark and Sweden, government consumption in Finland, and surprisingly resilient oil output in Norway. Net exports also tended to support the rebound. The unemployment rates appear to have peaked in July with gradual declines since, even as various fiscal support schemes were gradually withdrawn. If sustained, this would present an upside risk for our forecasts of household consumption in the coming quarters.

- The Scandinavian countries have so far successfully contained

the second wave of the pandemic with relatively mild restrictions.

Although the number of positive cases did rise, to a large extent a

reflection of more testing, as test positivity rates have recently

been close to just 3%, it never reached the extremely elevated

levels like elsewhere in Europe. Sweden is an exception, as new

cases and deaths have surged recently and test positivity rates

have been in double digits since mid-November, prompting a

tightening of the limit of the number of people from different

households that can meet. The relatively light restrictions in

Scandinavia are also reflected in lower falls in mobility versus

the baseline than most European countries. The largest drop in

mobility in Scandinavia during the second wave of the pandemic was

in Sweden, as growth in the number of cases accelerated,

reinforcing the complementarity between health and the economy.

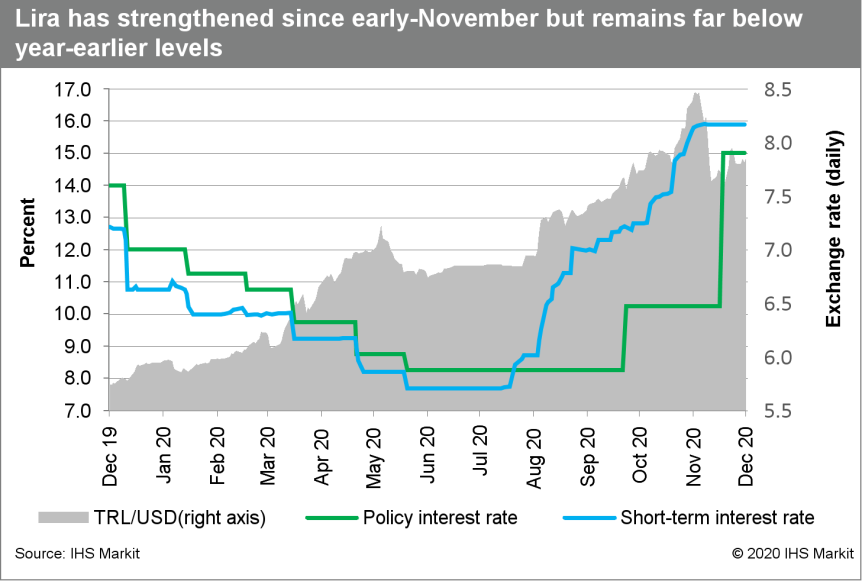

- After relative stability during the first 10 months of 2020,

inflation surged in November. Further interest rate rises may be

needed to keep inflation under control, especially if the lira's

depreciation resumes. (IHS Markit Economist Sharon Fisher)

- Consumer price inflation jumped 2.3% month on month (m/m) in November, pushing year-on-year (y/y) growth to 14.0%, far above the central bank's 3-7% target. Inflation was driven mainly by pressure in the transport and food and beverages categories, both of which reported m/m increases of more than 4%.

- Price pressures were considerably weaker, but still significant in household furnishings and equipment, hotels and restaurants, and housing and utilities, all of which rose 1% m/m or more. Education was the only price category to report a m/m decline.

- November inflation was even higher when excluding administrative prices, at 15.9% y/y. Core inflation (excluding energy, food and beverages, alcohol and tobacco, and gold) reached 13.3% y/y.

- Fueled by soaring manufacturing costs, producer price inflation surged 4.1% m/m in November. The y/y rate jumped to 23.1%, the highest figure since June 2019.

- Turkish inflation was partly driven by a steep depreciation of the lira, which plunged 39% y/y against the US dollar in November and 49% y/y against the euro. The lira has strengthened since its early November lows but nevertheless remains far below year-earlier levels.

- Even with the lira's sharp depreciation, growth in imports has far outpaced exports this year, triggering a significant widening of the external trade gap. According to Turkey's Ministry of Trade, exports fell a preliminary 1.0% y/y in November amid weakening EU demand, while imports surged 16.1% y/y.

- Even with the lira's weakening, November inflation was stronger than we had expected, pushing 12-month moving average inflation to 12.0%. Assuming that inflationary pressures continue in December, our latest projection for average annual inflation (at 12.0%) will be overshot.

- Looking ahead to 2021, IHS Markit is currently forecasting that

average annual inflation will reach 12.4%, but that figure may need

to be revised upward as well. The jump in inflation will hurt

Turkish households, which are already struggling with the impact of

the COVID-19 virus pandemic, with the number of new cases surging

in the past week.

- According to a report by Newsbase Daily News, Ford Otomotiv Sanayi (Ford Otosan), a joint venture (JV) between Ford Motor Company and Koç Holding in Turkey, is constructing an electric vehicle (EV) battery assembly plant in Kocaeli (Turkey). According to the source, Ford Otosan has started work on the facility. Haydar Yenigun, Ford Otosan's general manager, said that the new plant will be the first integrated EV production facility in Turkey. He added, "Ford Otosan ranks as one of the largest investors in the country with EUR2.5 billion [USD3.03 billion] of investments. It has so far committed EUR56 million to electric car production." Ford is aiming to complete construction of the plant in 2022 as it will have a direct impact on production of its Transit EV, which is due to be manufactured at the Kocaeli-Otosan plant. According to IHS Markit light-vehicle production forecasts, Ford Otosan currently manufactures the Transit Custom plug-in hybrid electric vehicle (PHEV) at the Kocaeli-Otosan plant and is forecast to sell 2,932 units of this model in 2020, while it is projected to sell 2,330 units of the Transit EV in 2022. Ford is also forecast to start manufacturing the Transit Custom EV at its Yenikoy plant in Turkey from 2024. (IHS Markit AutoIntelligence's Tarun Thakur)

- Israeli-based autonomous vehicle (AV) sensor manufacturer Innoviz Technologies is reportedly in talks about going public through a merger agreement with Collective Growth Corporation, a special-purpose acquisition company (SPAC). Bloomberg reports that Collective Growth is seeking to raise between USD100 million and USD350 million in new equity to support this deal. If the deal goes through, the new combined entity created through the merger will have a value exceeding USD1 billion. According to the report, the terms of the deal could change, or talks could fall apart if the deal is not finalized. (IHS Markit Automotive Mobility's Surabhi Rajpal)

Asia-Pacific

- Most APAC equity markets closed higher except for Japan -0.2%; South Korea +1.3%, India +1.0%, Hong Kong +0.4%, Australia +0.3%, and Mainland China +0.1%.

- US lawmakers have passed a bill requiring foreign companies trading on US stock exchanges, including the New York Stock Exchange and NASDAQ, to comply with US audit oversight rules. According to media reports, Chinese electric vehicle (EV) manufacturers NIO, Li Auto, and Xpeng might not be compliant currently with the requirement and could face delisting. Financial news outlet Barron's reports that, under the bill, all foreign companies would have to comply with US audit oversight rules within three years, which means that these companies would have some time to become compliant, if they are not currently. Under the bill, the companies would need to be audited by an auditor inspected by the US Public Company Accounting Oversight Board (PCAOB). Barron's report quotes Li Auto's filing with the Securities and Exchange Commission (SEC) on 2 December as saying on the issue, "The audit report included in this prospectus is prepared by an auditor who is not inspected by the PCAOB and, as such, our investors are deprived of the benefits of such inspection. In addition, the adoption of any rules, legislations or other efforts to increase U.S. regulatory access to audit information could cause uncertainty, and we could be delisted if we are unable to meet the PCAOB inspection requirement in time." The requirement under the bill applies to any foreign company, not just the three EV companies or other Chinese companies. Some media reports have focused on the potential impact of the bill's requirements on China's younger EV companies; however, IHS Markit has no information to suggest that any particular company is 'targeted' by the new law. (IHS Markit AutoIntelligence's Stephanie Brinley)

- Japanese automakers Nissan and Honda both reported year-on-year

(y/y) sales gains in the Chinese market during November. (IHS

Markit AutoIntelligence's Nitin Budhiraja)

- Nissan's sales in China increased 5.2% y/y to 156,319 units in November, but are down 6.6% y/y to 1.287 million units in the year to date (YTD; January to November). Sales of Nissan's passenger-vehicle joint venture (JV) with Dongfeng, including sales of the Nissan and Venucia brands, rose by 8.2% y/y to 135,816 units in November, but are down 7.1% y/y to 1.067 million units in the YTD.

- Sales of Nissan's light commercial vehicles (LCVs), comprising sales of Dongfeng Automobile Co (DFAC) and Zhengzhou Nissan (ZNA), declined by 8.2% y/y to 135,816 units in November, but have increased 0.8% y/y to 195,118 units in the YTD.

- In a statement, Honda said that its Chinese sales rose 22.1% y/y to 171,308 units during November and are up 0.5% y/y to 1.418 million units in the YTD.

- Sales of the Guangqi Honda JV were 85,985 units during November, up 24.5% y/y, and 708,536 units in the YTD, up 1.5% y/y. Sales of the Dongfeng Honda JV rose 19.8% y/y to 85,323 units in November and fell 0.5% y/y to 709,588 units in the YTD.

- Honda continues to gain traction in the Chinese market thanks to a strong product line-up. The increasing availability of full-hybrid options in its key model lines, such as the Accord, Crider, and CR-V, is helping the automaker to increase its sales. For Nissan, the Altima and Sylphy were the main drivers of growth in November.

- SAIC-General Motors (GM)-Wuling (SGMW), a joint venture (JV)

between SAIC Motor Corporation, GM, and Wuling Motors, has seen its

sales rise steadily over the past few months thanks largely to its

hot-selling new model, the Wuling Hongguang Mini EV. (IHS Markit

AutoIntelligence's Abby Chun Tu)

- According to the automaker, the budget battery electric vehicle (EV) from SGMW's Hongguang brand is likely to claim the top position in the monthly sales rankings of EVs with a retail volume of 33,094 units in November.

- In October, the Hongguang Mini EV overtook Tesla's Model 3 in the EV sales ranking with a retail volume of 20,631 units. To put this into perspective, the budget BEV model accounted for 23% and 30% of China's EV sales in September and October respectively, contributing to the recent uptick in China's EV sales.

- The surging demand for the Hongguang Mini EV is also helping SGMW to regain its sales momentum in the Chinese market. The automaker has reported sales increases for four consecutive months since July. In the year to date (January to October), SGMW has narrowed the decline in its sales volumes to 9% year on year (y/y).

- This shows a significant improvement compared with a sales decline of 23% y/y recorded for January to July.

- IHS Markit anticipates SGMW to increase its market share in the entry-level vehicle segment to 17% in China by the end of the fourth quarter, improving from 11% in the second quarter.

- Although the Wuling Hongguang Mini EV and the Tesla Model 3 are competing in two different segments and targeting different consumer groups, the two models have been mentioned together in recent news reports as examples showing the divide in EV demand in the Chinese market, and the growing acceptance of EVs in both the budget and the mass-market EV segments.

- Both models have contributed to the sales recovery of China's EV market and fit well with the Chinese government's plan to spur EV demand by widening consumer choice, thus reducing the industry's reliance on subsidies.

- Mini-EVs such as the Hongguang Mini EV are a unique offering in the Chinese market, as most automakers have shifted from smaller electric models to more-popular C- and D-segment products. The success of the Hongguang Mini EV is likely to lure more automakers to the sector with their products.

- The Australian Office of the Gene Technology Regulator (OGTR) has issued a three-year statement of intent on the regulation of genetically modified organisms (GMOs). It says that the aim of the 2020-2023 plan is the safe management of GMO use and public confidence in the Office as regulator. The statement outlines the activities of the Gene Technology Regulator (the regulator) and the OGTR, and should be read in conjunction with the OGTR stakeholder engagement framework, the OGTR science strategy and the OGTR monitoring and compliance framework. The government's vision for the OGTR is that it continue "to be a high-performing organization that supports the regulator to achieve the important object of the Gene Technology Act 2000". The OGTR has set itself four objectives. They are to deliver efficient and effective regulation that protects people and the environment; to provide a safe, respectful and inclusive workplace that is productive and professionally rewarding; to inform and engage effectively with stakeholders so that they understand and respect its decisions; and to ensure that governance arrangements are robust, illustrate best practice and fulfil all legal obligations. (IHS Markit Crop Science's Robert Birkett)

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-4-december-2020.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-4-december-2020.html&text=Daily+Global+Market+Summary+-+4+December+2020+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-4-december-2020.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - 4 December 2020 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-4-december-2020.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+4+December+2020+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-4-december-2020.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}