Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Nov 03, 2020

Daily Global Market Summary - November 3, 2020

All major global equity indices closed higher today, with CDX and iTraxx credit indices tighter across IG and high yield. US government bonds closed sharply lower and the curve steepened further, while benchmark European government bonds closed mixed. The US dollar was lower on the day and oil, gold, and silver all closed higher. The early US election results appear to already be spurring some volatility in US equity futures and government bonds, as both presidential candidates appear to be in a tight race in several key states.

Americas

- The NY Times has US Presidential Candidate Joe Biden ahead of President Trump with 131 vs 92 electoral votes as of 9:49pm ET (need 270 electoral votes to win), with key contests in Florida, Georgia, and North Carolina still too close to call (NY Times).

- US equity markets closed higher, with all major indices trading higher the entire day; Russell 2000 +2.9%, DJIA +2.1%, Nasdaq +1.9%, and S&P 500 1.8%. S&P futures began to fall at approximately 7:30pm ET and were -0.4% as of 9:32pm ET, as preliminary US election results are continuing to trickle in.

- 10yr US govt bonds closed +4bps/0.90% yield and 30yr bonds +7bps/1.69% yield. 10yr US govt bond yields were as high as 0.93% at 7:16pm ET and are 0.82% as of 9:44pm ET.

- CDX-NAIG closed -3bps/60bps and CDX-NAHY -17bps/401bps.

- DXY US dollar index -0.7%/93.48 as of 8:04pm ET.

- Gold closed +0.9%/$1,910 per ounce and silver +1.2%/$24.33 per ounce.

- Crude oil closed +2.3%/$37.66 per barrel.

- In a press release, WPX Energy reported a third-quarter 2020 net loss of $148 million, compared with a net income of $122 million in the year-ago period, primarily due to a $110 million net loss on derivatives resulting from non-cash forward mark-to-market changes in the company's hedge book and a loss on the extinguishment of debt, the company said. The adjusted net income was $60 million, compared with an adjusted net income of $38 million a year ago. Adjusted EBITDAX was $389 million, compared with $361 million a year ago. Total product revenues were $491 million, including oil sales of $436 million, compared with $581 million, including oil sales of $539 million, a year ago. Production totaled 207,700 boe/d (78% liquids), up 20% from 173,400 boe/d a year ago. Oil volumes were 122,300 b/d, up 13% from 108,600 b/d a year ago, led by a 51% increase in the Delaware Basin. The realized oil price was $38.72/bbl, compared with $53.92/bbl a year ago; the realized gas price was $0.57/Mcf, versus $0.77/Mcf a year ago; the realized NGL price was $11.22/bbl, versus $10.73/bbl. In September 2020, Devon Energy signed an agreement to acquire WPX Energy Inc. in an all-stock transaction valued at $6.34 billion. The transaction is expected to close in the first quarter of 2021. (IHS Markit Upstream Companies and Transactions' Karan Bhagani)

- US manufacturers' orders rose 1.1% in September, while

shipments rose 0.3%. After sharp increases over May, June, and

July, the pace of recovery in orders and shipments has slowed

considerably. (IHS Markit Economists Ben Herzon and Lawrence

Nelson)

- In response to these and other details in the report that bear on our GDP tracking, we lowered our estimate of third-quarter annualized GDP growth by 0.2 percentage point to 32.8% and raised our forecast of fourth-quarter growth by 0.1 percentage point to 5.2%.

- While recovery in manufacturing has come a long way, orders remain 4.3% below the February level and shipments remain 3.0% below the February level.

- These data are consistent with severalother indicators pointing to a material slowing in the pace of recovery, including slowing profiles in employment, industrial production, and monthly GDP.

- Orders and shipments of core capital goods, by contrast, have been robust in recent months. Both have surged past their pre-pandemic levels, and both were revised somewhat higher through September in today's (3 November) report.

- Manufacturers' inventories were flat in September. We had assumed a 0.3% increase (the reading implicit in the advance estimate of the National Income and Product Accounts [NIPA]).

- The unexpected weakness in inventories lowered our estimate of third-quarter inventory investment by roughly $9 billion and raised our forecast of the change in inventory investment in the fourth quarter by about $5 billion.

- With a seasonally adjusted selling rate (SAAR) estimated to be

in the range of 16.2-16.5 million units at time of publishing, the

pace of light-vehicle sales continues to improve from the April

2020 low reading of 8.7 million units. And if it manages to improve

from the 16.34 million unit reading of September, would mark the

sixth consecutive month that the pace of sales has advanced from

the month-prior result. (IHS Markit Economist Chris Hopson)

- On an unadjusted volume level, the sales tally for the month is expected to be up 1-3% year-on-year (y/y). While we do not expect the monthly SAAR to diverge meaningfully from the average pace of the past three months (an average of approximately 16.0 million units), even before any possible election outcome is factored in, we anticipate that the upcoming monthly volume results in November and December will reflect some y/y volatility.

- Compared with their respective year-ago periods, there will be three fewer selling days in November, while December will have three more selling days. The sequential rise in auto demand levels from April reflects that consumers who are willing, ready, and able to enter a new car purchase are doing so.

- There were 28 selling days this October, one more than the year-earlier period. On a unit volume level, October sales are estimated to have climbed to approximately 1.35-1.37 million units, which would be above the year-earlier level, and bring the year-to-date light-vehicle sales volume figure through October to approximately 17% below the year-earlier level. We do not expect the pace of sales to advance much further than the results of the past two months, but the ongoing recovery in auto sales lends upside bias in expectations for the remainder of the year.

- Stock management will continue to be an important variable moving through the immediate forecast horizon, but the all-out vehicle production schedules now should help improve the situation as we progress into the new year. Month-end October inventory levels as reported by AutoData at time of publishing were estimated to be up from the previous month. Compared with month-end September, October 2020 industry inventory was up approximately 85,000 units. The days' supply reading at the end of October rose to a reading of 56 days' supply, up from a 48 days' supply level at the end of September and but still down meaningfully from the 72 days' supply a year earlier.

- Please note: All industry-level numbers in this report are estimates, owing to the absence of official monthly reports from General Motors (GM), Ford, Fiat Chrysler Automobiles (FCA), and others.

- Ford plans to offer a hands-free driving feature, Active Drive Assist, first on the redesigned F-150 pick-up and the new Mustang Mach-E electric crossover. The hands-free feature will be included as standard on certain car models or as a relatively affordable option on others, with both the redesigned F-150 and the Mustang Mach-E expected to go on sale later this year. Ford expects to sell 100,000 units of these vehicles equipped with the hands-free technology hardware in their first year. Initially, the vehicles will be equipped with the hardware system only and the software technology will become available in the third quarter of 2021. Ford says that, once the software is launched, the system will activate the hands-free feature through a wireless over-the-air (OTA) update. Hau Thai-Tang, chief product platform and operations officer at Ford Motor Company, said, "Active Drive Assist can help improve the driving experience while ensuring people remain aware and fully in control, all for a price unmatched by our competitors - a commitment to affordable innovations that has driven us since Henry Ford put the world on wheels." Ford's new Active Driving Assist is not designed to be a semi-autonomous driving system, although it advances Ford's technology significantly. Ford is also the first mainstream brand to launch a hands-free system, as other examples have been introduced by luxury vehicle brands. Ford is also replicating a strategy used by Tesla: the system's hardware will be available to order ahead of the software being deployed via OTA. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Autonomous vehicle (AV) startup Pony.ai has reportedly completed a new round of financing, raising over USD300 million. This will bring the company's market value to USD6 billion, reports Pandaily. The latest funding round was led by Ontario Teachers' Pension Plan (OTTP), contributing nearly USD200 million, and involved the participation of Chinese automaker FAW Group. Pony.ai was founded in 2016 and develops Level 4 AV technology. The company has launched the PonyPilot, a test project for driverless cars within a geo-fenced area in Guangzhou's Nansha district (China), which is available to Pony.ai employees and selected affiliates. In California (United States), the company has launched an autonomous delivery service in Irvine and a last-mile robotaxi service in the city of Fremont. Recently, the Beijing government allowed the company to test its AVs by carrying passengers in the city's Haidian district and Yizhuang town. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Autonomous vehicle (AV) sensor manufacturer Aeva Inc is planning to go public through a merger agreement with InterPrivate Acquisition Corp, a special-purpose acquisition company (SPAC). This will bring the market value of LiDAR startup company Aeva to USD2.1 billion, reports Reuters. The deal with InterPrivate, which is led by private equity investor Ahmed Fattouh, will give Aeva a cash injection of more than USD300 million to expand its sensor development to consumer electronics. Soroush Salehian, co-founder and CEO at Aeva, said, "We want Aeva [to be] not just highly assisted on autonomous vehicles, but across a number of applications." The deal is due to be closed in the first quarter of 2021, after which Aeva will trade on the New York Stock Exchange under the ticker 'AEVA'. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Neogen has launched a new DNA sorting tool that aids producers in ranking and managing feeder cattle according to their genetic potential for carcass traits. The Igenity Feeder is designed to assist cattle producers in the stocker and backgrounder phase of beef cattle rearing. The tool is a next-generation version of the Igenity Terminal Index, which is a tool specialized for identifying animals for terminal crossbreeding that measures the genetic potential for economically relevant carcass traits. Neogen said: "Igenity Feeder leverages the ITI and growth profiling information from thousands of commercial fed cattle into an accurate genomic tool to help producers' sort lots of cattle and enhance profitability. Using Igenity Feeder, combined with an animal's enrollment weight and sex, provides a new opportunity for grouping of animals into outcome groups." Neogen claims Igenity Feeder enables producers to ship or sell load lots of cattle with increased uniformity, distinguish their cattle on sale day, and accurately and rapidly sort calves based on their ability to excel to end point. President and chief executive of the firm John Adent said: "With Igenity Feeder we are reaching a critical audience in the beef supply chain by offering a DNA tool they can utilize to make better decisions in the care, nutrition and marketing of their feeder calves. By extension, producers will use the genomic information to tell the story of their calves to the feedlot level." With a tissue sampling unit taken at enrollment, Igenity Feeder will also work in unison with Igenity Branded, which is the company's free feeder calf marketing program. Dr Jamie Courter, Neogen beef product manager, commented: "Igenity Feeder provides producers the ability to sort and rank feeder cattle according to their genetic predisposition to perform within the feedlot. Driven by many economically relevant traits such as hot carcass weight, rib eye area and marbling, the ITI is proven to help differentiate profitability in a feedlot setting. Earlier this year, Neogen launched updated content to Angus GS - the first genomic profiler designed specifically for Angus cattle - alongside Angus Genetics. The two companies introduced the Angus GS DNA diagnostic on the US beef market in 2017. More recently, Neogen closed a deal for Elanco's StandGuard Pour-on insecticide, which saw it gain US rights to the horn fly and lice control product for beef cattle. (IHS Markit Animal Health's Daniel Willis)

- Seasonally adjusted data from the flash GDP release show the

Mexican economy jumped by 12.0% quarter on quarter (q/q) after

plunging by 17.12% in the previous quarter. Although third-quarter

real GDP growth was very strong due to forcible "carryover"

effects, high-frequency indicators including the monthly index of

economic activity (MIEA) show that the recovery is ebbing. (IHS

Markit Economist Rafael Amiel)

- After plummeting in April and May because of the lockdowns, the MIEA increased by 8.9% month on month (m/m) and 5.7% m/m in June and July, respectively; it expanded by only 1.1% in August and slowed down further to 0.7% in September.

- Mexico's industry posted the strongest rebound in the third quarter compared with the second quarter of 2020, followed by services and the always-volatile agricultural sector (see table below). Most manufacturing plants were fully closed in April and May because of the coronavirus disease 2019 (COVID-19) virus and reopened to almost full capacity in June; the largest positive impact of the reopening is captured by quarter-three figures.

- On the annual comparison, GDP fell by 8.6% - this is using

unadjusted data and comparing with July-September 2019. This gives

a better perspective on how far the Mexican economy is in terms of

recovery.

The labor market, which is usually a lagging indicator, shows that there is still a long way to full recovery; 12 million people left the labour force in April, but by September, 8.4 million had returned, but not all have found a job, with 6.2 million jobs still missing. - The recovery in Mexico has lost its momentum, with the initial "mechanical" rebound caused by the lifting of social-distancing measures and the reopening of economic activity throughout the country.

- Growth in the third quarter was somewhat better than anticipated by IHS Markit (we called for a 10.2% q/q expansion) and this may lead us to revise upwards our 2020 forecast by two-three tenths of a percentage point.

- According to the National Institute of Statistics and

Information (Instituto Nacional de Estadística e Informática),

Peru's consumer price index increased by 0.02% month on month (m/m)

in October and by 1.72% year on year (y/y). (IHS Markit Economist

Jeremy Smith)

- The largest contributor to inflation in October was an increase in prices across the recreation, leisure, and cultural and educational services category (0.12% m/m), principally owing to fast-growing demand for online educational services. Rising prices in the housing rental, petrol, and electricity category (0.16% m/m) as well as in the furniture, equipment, and home maintenance category (0.17% m/m) also added to the marginal increase in inflation.

- Meanwhile, the food and beverages category dropped by 0.08% m/m as a large increase in seafood supply drove down prices, more than compensating for rising fruit prices. In addition, prices in the transportation and communications category fell by 0.08% m/m.

- Core inflation, which excludes more volatile food and energy products, registered a similarly modest annual rate of 1.68% y/y.

- Neither pent-up demand nor a 200-basis-point reduction in the policy interest rate since March seems to have produced significant inflationary pressure to this point. Flat price growth in October is in line with the substantial slowing in employment and production recovery observed in recent months.

- October marked the 14th consecutive month in which annual inflation registered below the Central Reserve Bank of Peru (Banco Central de Reserva del Perú: BCRP)'s target of 2%. While expectations remain anchored to the target in the medium term, IHS Markit currently does not anticipate annual inflation to reach 2% until 2022.

Europe/Middle East/Africa

- European equity markets closed sharply higher across the region; Italy +3.2%, Germany +2.6%, Spain +2.5%, and France +2.4%.

- 10yr European govt bonds closed mixed; UK +6bps, Germany +2bps, and Italy/Spain -2bps.

- iTraxx-Europe closed -2bps/61bps and iTraxx-Xover -9bps/349bps.

- Italy's total employment was broadly stable at 22.953 million

in September. Therefore, cumulative job losses in March to

September stood at 329,000, or 1.4% lower when compared with

February 2020, the pre-COVID-19-virus level. (IHS Markit Economist

Raj Badiani)

- The unemployment rate retreated for the third straight month to 9.6% in September (from 9.7% in August). Meanwhile, the number of unemployed shrunk for a second successive month to 2.43 million in September, in line with 2.4 million in February.

- Meanwhile, the labor force fell by 0.1% month on month to 25.4 million in September, with the activity rate stable at 64.5%.

- The inactivity rate fell from 31.4% in August to 29.7% in September. It appears that more laid-off workers are now looking for jobs after failing to do so during the height of the COVID-19-virus lockdown.

- The employment losses have been less severe than expected during the COVID-19-virus shock, with the country's short-time work or temporary layoff schemes helping to shore up employment levels. In addition, the demand for labor probably enjoyed some support from a stronger-than-expected economic rebound during the third quarter, with the national statistical office reporting that GDP increased by 16.1% quarter on quarter.

- A major support to employment has been the expansion to the Cassa Integrazione Ordinaria, or the Support of Salary Payment by the state. An employer can suspend or reduce work activity for events related to the COVID-19 virus and enjoy social contribution exemption. Importantly, firms have to maintain their workforces to qualify for state aid.

- The European Central Bank estimates that some 8.5 million workers, or 44% of Italian employees, were on these schemes during the lockdown in Italy. In August, the government agreed to extend the short-term work scheme until the end of 2020.

- Italy's passenger car registrations in October were almost level with those recorded during the same month in 2019. According to the latest data published by the National Association of Foreign Vehicle Makers' Representatives (Unione Nazionale Rappresentanti Autoveicoli Esteri: UNRAE), demand slid by just 0.2% year on year (y/y) during the month to 156,978 units. However, the significant impact of the COVID-19 virus in the earlier months of 2020 remains in evidence in the year to date (YTD), with demand dropping by 30.9% y/y to 1,123,194 units. The Italian passenger car market has performed solidly again in October, partly because of the Decreto Agosto measures that came into force at the beginning of September. The funding for this was split into three tranches and the size of the benefit is dependent on the carbon dioxide (CO2) emissions of the vehicle in question. (IHS Markit AutoIntelligence's Ian Fletcher)

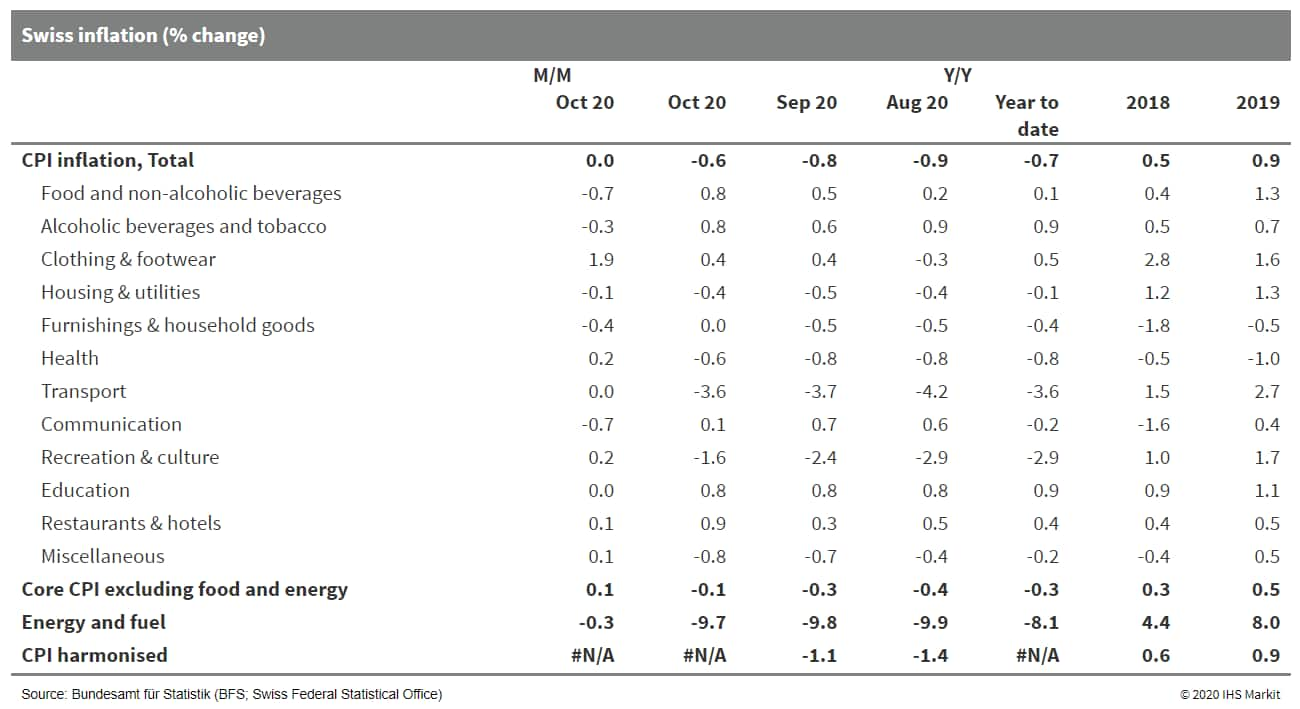

- According to the Swiss Federal Statistical Office (FSO),

Switzerland's consumer prices again remained flat month on month

(m/m) in October, as in May, June, August, and September. The

unchanged outcome in October is in line with the long-term average

for the month, but the annual rate of the consumer price index

(CPI) increased from -0.8% to -0.6% because of a base effect. This

compares with a cyclical low of -1.3% year on year (y/y) in May and

June. (IHS Markit Economist Timo Klein)

- The EU-harmonized measure with its somewhat different composition was also flat m/m, with its y/y rate thus rising from -1.1% to -0.9%.

- Eight of the twelve main Classification of Individual Consumption According to Purpose (COICOP) categories of goods and services of the national data posted a higher annual rate than in September and only two categories posted a lower one, with the two remaining groups - clothing and footwear and education - keeping steady (see table below). The main upward influences, in this order and taking relative weights into account, came from recreation and culture, hotels and restaurants, food, and healthcare. The only two categories that had another dampening effect were communication and "miscellaneous goods and services". Energy prices slipped only slightly (-0.3% m/m), leaving their annual rate almost unchanged compared with September at -9.7% y/y.

- The split between goods (0.0% m/m and -1.2% y/y, the latter up from -1.4% y/y in September) and services (0.0% m/m and -0.2% y/y, the latter up from -0.4% in September) reveals that there was a little difference with regards to data-edge developments between the two categories.

- The prices of domestic goods were also flat m/m, while those of imported goods increased by 0.1% m/m, leading to modest increases of their respective annual rates in both cases - from -0.1% to 0.2% for domestic inflation and from -3.0% to -2.8% for imported inflation. The latter's trend in particular should continue in early 2021 as boosting base effects come into play.

- Core consumer prices, a measure that excludes the impact from volatile components such as food and energy, increased by 0.1% m/m - firmer than the (national) headline measure - and its annual rate rose further from -0.3% to -0.1%. This extends the recovery from June's interim (four-year) low at -0.8% y/y and compares with a 10-year high of 0.7% in June 2019.

- Finally, the gap between headline inflation and core inflation, which had been positive between late 2016 and May 2019 before turning negative during the remainder of 2019, stayed at -0.5%.

- Switzerland's deflation pressure is letting up, although it

probably will take until April 2021 before the y/y rate shifts from

negative to positive territory again. It is noteworthy that the

recent stabilization occurred despite the halt and partial reversal

to the Swiss franc's temporary (June-September) weakening tendency

during October.

- Bioplastics made from plant-based and other 'natural' materials are touted as the eco-friendly alternative to conventional plastics, but a German study has found that they are at least equally toxic as conventional plastics, and some may be more so. "Bioplastics and plant-based materials are marketed as sustainable alternatives to conventional plastics. However, little is known with regard to the chemicals they contain and the safety of these compounds," noted the abstract to the Zimmerman et al study "Are bioplastics and plant-based materials safer than conventional plastics? In vitro toxicity and chemical composition" in explaining the reason for launching the study. For their work on the study the researchers extracted 43 everyday bio-based or biodegradable products as well as their precursors, covering mostly food contact materials made of nine material types. Then the team characterized these extracts using in vitro bioassays and non-target high-resolution mass spectrometry. Overall, the study found that compared to conventional plastics "bioplastics and plant-based materials are similarly toxic." The study concluded that "the majority (67%) of bioplastics and plant-based products contain toxic chemicals." More specifically, the researchers found: "Two-third (67%) of the samples induced baseline toxicity, 42% oxidative stress, 23% antiandrogenicity and one sample estrogenicity." They also saw: "Extracts from cellulose- and starch-based materials generally triggered a strong in vitro toxicity and contained most chemical features." noted. However, the study observed that the toxicological and chemical signatures of polyethylene (Bio-PE), polyethylene terephthalate (Bio-PET), polybutylene adipate terephthalate (PBAT), polybutylene succinate (PBS), polylactic acid (PLA), polyhydroxyalkanoates (PHA) and bamboo-based materials "varied with the respective product rather than the material. Toxicity was less prevalent and potent in raw materials than in final products." Based on the findings, the study recommends that migration studies with food simulants are needed to identify the toxicity of any bioplastic and measure the level of chemicals migrating under real-world conditions as well as estimate human exposure to them. (IHS Markit Food and Agricultural Policy's Sara Lewis)

- Bayer swung to a third-quarter net loss of €2.74 billion ($3.21

billion) from a net profit of €1.04 billion a year earlier on sales

of €8.51 billion, down 5.1% on a currency- and portfolio-adjusted

basis. The net loss includes non-cash impairment charges on

intangible assets, and provisions, totaling €10.18 billion. They

are mainly in Bayer's agricultural division, crop science, in

connection with potential future litigation in the US related to

the company's glyphosate-based herbicide Roundup™. Other special

charges are from an ongoing restructuring program and litigation at

Bayer's pharmaceuticals business.

- Bayer's EBITDA before special items decreased by 21.4% year on year (YOY) in the third quarter to €1.79 billion, including a negative currency effect of €205 million, missing analysts' consensus estimate by 12.7%. Crop science was the main driver of the miss with a big decline in third-quarter sales and earnings due partly to seasonal factors. Bayer has nevertheless confirmed its outlook for full year 2020.

- Sales at the crop science business dropped 11.6% YOY, foreign exchange and portfolio adjusted, in the third quarter, to €3.03 billion. Business was down in North America in particular, and sales increased in APAC. EBITDA before special items swung to a negative €34 million from a positive €500 million in the year-earlier period, mainly due to the decrease in sales in North America. There was also a negative currency effect of €123 million, Bayer says.

- Worldwide sales at the corn seed and traits segment fell by 39.9%, adjusted, with substantial declines in North America in particular due to higher product returns and lower license revenue arising from lower-than-anticipated planted acreages for corn this year. At the herbicides segment, sales declined by 12.7%, adjusted, against a strong prior-year quarter. Business was primarily down in North America, where sales in 2019 had shifted into the third quarter due to extreme weather conditions in the first half of that year.

- Sales of Bayer's pharmaceuticals business declined 1.8%, on a foreign-exchange and portfolio adjusted basis in the third quarter, to €4.23 billion with EBITDA before special items edging up 0.9% to €1.51 billion. "Thanks to stringent cost management, the division was able to grow its earnings and margin despite the decline in sales due to the negative overall impact of COVID-19 as well as negative currency effects of €48 million that additionally weighed on earnings," Bayer says.

- Sales of Bayer's consumer health business increased 6.2%, adjusted, to €1.20 billion putting the division's growth well ahead of industry market growth, the company says. The growth trend was driven by the nutritionals segment, with sales rising 21.4% due to the greater focus on health and prevention in connection with the COVID-19 pandemic as well as the launch of new products, Bayer says. EBITDA before special items at consumer health increased by 12.3% to €301 million, primarily due to the substantial increase in sales and positive contributions from an efficiency program launched in late 2018.

- Passenger car registrations in Spain dropped even further during October. According to the latest data published by the Spanish Association of Passenger Car and Truck Manufacturers (Asociación Española de Fabricantes de Automóviles y Camiones: ANFAC), demand fell by 21% y/y to 74,228 units. The YTD figures now stand at 669,662 units, a decline of 36.8% y/y. The decline in the Spanish passenger car market was despite support, introduced in mid-June, for parc replacement and those looking to purchase alternative powertrain vehicles. Although there was some initial uplift in July, interest has since waned. Underlining the thinking that these measures are not generous enough to lure uncertain consumers to the market is the 22.7% y/y fall in private customers during October. (IHS Markit AutoIntelligence's Ian Fletcher)

- Norwegian passenger car registrations have jumped by 23.6% year on year (y/y) in October, according to the latest data published by the country's Road Traffic Information Council (Opplysningsrådet for Veitrafikken: OFV). Demand in this market grew from 10,479 units to 12,948 units. The leading brand during the month was Volkswagen (VW), with 2,889 units, as its registrations leapt by 87.2% y/y. Toyota also had a strong month, recording a gain of 19.9% y/y to 1,576 units. However, BMW in third contracted by 19.3% y/y to 734 units. The performance this month has meant that the year-to-date (YTD) passenger car market is now down by 10.6% y/y at 108,298 units, owing in part to the impact of the coronavirus disease 2019 (COVID-19) virus earlier in the year. Elsewhere in the market, registrations of light commercial vehicles (LCVs) of up to 3.5 tons gained by 5.1% y/y to 2,866 units during October, meaning that their YTD total is now down by 20.4% y/y at 25,713 units. At the same time, medium and heavy commercial vehicle (MHCV) registrations retreated by 26.7% y/y to 553 units in October, resulting in their YTD registrations falling by 19.7% y/y to 5,234 units. The Norwegian passenger car market has experienced some significant swings so far this year caused by the COVID-19 virus pandemic. However, the jump in October was partly driven by ongoing demand for battery electric vehicles (BEVs) thanks to generous incentives. BEV registrations leapt by 110.4% y/y to 7,873 units in October, meaning that they made up a 60.8% share of the entire passenger car market in that month. (IHS Markit AutoIntelligence's Ian Fletcher)

- In a press release, Saudi Aramco reported third-quarter 2020 net income of $11.8 billion (44.2 billion Saudi riyals), down 45% from $21.3 billion in the third quarter of 2019. The decrease in the earnings was primarily due to the impact of lower crude oil prices and volumes sold, and weaker refining and chemicals margins, partly offset by a decrease in crude oil production royalties resulting from lower prices and volumes sold as well as a decrease in the royalty rate from 20% to 15%, and higher other income related to sales for gas products, the company said. Net cash provided operating activities was $18.8 billion, down about 35% from $28.7 billion in the third quarter of 2019. Third-quarter 2020 capital expenditure was $6.4 billion, down about 21% from $8.1 billion a year ago. Averaged realized crude oil price was $43.6/bbl, down about 30% from $62.4/bbl a year-ago period. Upstream segment's EBIT (earnings before interest, income taxes and zakat) for the third quarter of 2020 was $27.6 billion, down 38% from $44.7 billion a year ago. The decrease in earnings was primarily due to lower realized crude oil prices and lower crude oil volumes sold, partly offset by lower crude oil production royalties following lower prices and volumes sold, along with a decrease in the royalty rate, and higher other income related to sales for gas products, the company said. Downstream EBIT for the third quarter of 2020 was a loss of $795 million, down from an EBIT of $801 million a year ago. The decline reflects a challenging market environment that continues to weaken refining and chemicals margins. Total hydrocarbon production for the first nine months of 2020 was 12.4 MMboe/d (74% oil). Gross refining capacity was maintained at 6.4 MMb/d as at 30 September 2020. The company maintained a dividend of $18.75 billion for the third quarter of 2020. (IHS Markit Upstream Companies and Transactions' Karan Bhagani)

- South Africa's October Medium Term Budget Policy Statement

shows the budget deficit for fiscal year (FY) 2020/21 increasing

slightly to 15.7% of GDP and the public-sector debt trajectory

worsening significantly, compared with the supplementary emergency

budget's projections presented on 24 June. (IHS Markit Economist

Thea Fourie)

- The South African government's medium-term fiscal trajectory, released in the 2020 Medium Term Budget Policy Statement (MTBPS) on 28 October, involves a combination of public-sector spending cuts and revenue-raising measures to stabilize public-sector debt levels. However, the low-growth environment, large primary budget deficits, and high yields on South African government bonds continue to complicate the authorities' debt stabilization efforts.

- In the MTBPS, the main budget deficit for FY 2020/21 increases to 15.7% of GDP, coming down slowly to 10.1% of GDP in FY 2021/22, 8.6% of GDP in FY 2022/23, and 7.3% of GDP in FY 2023/24. Gross public-sector debt continues to edge up, reaching 92.9% of GDP in FY 2023/24, from 81.8% of GDP in FY 2020/21.

- The MTBPS's estimates rest on the introduction of ZAR300 billion (USD18.5 billion) of spending cuts over the medium term, stretching from FY 2021/22 to FY 2023/24, primarily through a reduction of the public-sector wage bill. "The Budget Guidelines propose a wage freeze for the next three years to support fiscal consolidation. Additional options to be explored include harmonizing the allowances and benefits available to public servants, reconsidering pay progression rules and reviewing occupation-specific dispensations. The next round of wage negotiations is due to start soon and work is under way to formulate government's position," the MTBPS reports. The fiscal plan also allows for a cumulative ZAR25 billion upward revision in government income, although no details about the tax adjustments to be implemented were released. The details are due to be presented during the February 2021 national budget.

- The MTBPS allows for an additional ZAR10.5 billion allocation to embattled state airline South African Airways (SAA), which will permit the implementation of the business rescue program. No additional transfers to other embattled state-owned entities (SOEs), such as Eskom, Denel, and Land Bank, beyond the original budget allocations have been penciled in, at this stage. In the MTBPS, the extension of the COVID-19 pandemic-related special social-relief-of-distress grant will cost the government an additional ZAR6.7 billion. The SAA allocation and additional social grants are budget neutral and are to be financed through reallocations from other government spending programs.

- Debt servicing costs continue to edge up, reaching 5.9% of GDP or 23.7% of government revenue by FY 2023/24, in the MTBPS.

- The budget estimates rest on an expected GDP contraction of 7.8% in 2020, rebounding to 3.3% growth in 2021, before slowing to 1.7% and 1.5% in 2022 and 2023, respectively. In the MTBPS, headline inflation remains close to the mid-point of the South African Reserve Bank's inflation target range of 3-6% over the forecast horizon.

- Reaching debt sustainability over the five-year horizon, which is beyond the MTBPS timeframe, hinges primarily on the ability of the South African government to contain the public-sector wage bill through the introduction of public-sector wage freezes. Furthermore, any GDP growth surprises on the upside could improve the South African government's public debt trajectory over the medium term.

- The Democratic Republic of the Congo (DRC)'s international

reserves accumulation was particularly strong in September,

following a slump in March, according to latest data published by

the DRC's central bank, the Banque Centrale du Congo (BCC). (IHS

Markit Economist Alisa Strobel)

- The BCC released its latest data on the DRC's economic performance on 2 October, showing that international reserves, including foreign bank deposits, amounted to 4.89 months of import cover (equivalent to 21 weeks) during the last week of September, after peaking at 4.97 months of import cover during the last week of August. The DRC's import cover fell to 3.67 months during the week ending 27 March, the lowest registered number so far in 2020.

- Further data analysis of the DRC's key exports shows that copper production continued to accelerate through the first eight months of 2020. Although volatile in nature, production levels during April to August 2020 were generally higher than seen during July 2019 to March 2020. Cobalt production remained at similar levels in 2020 to those seen in 2019, while zinc production continued gaining pace in 2020 following a slump in 2018.

- IHS Markit forecasts a contraction of 2.4% in the DRC's real GDP in 2020. However, improved activity in the extractive sector in the third quarter of 2020 could smooth our prediction to around the government's estimate of a contraction of around 1.7-2%. A slow recovery in growth is expected during the second half of 2021. Downside risks are increasing as we expect to see depressed business sentiment at the start of 2021 amid the global uncertainty over the commodity price recovery and return of foreign direct investment.

- Congolese exports to China represent around 30% of exports,

mainly mineral products. Exports of mineral products, mainly ores

and metals, represent more than 80% of the DRC's total exports,

dictating the growth of foreign-exchange reserves. With mainland

China being the largest importer of Congolese minerals, any shock

affecting its economy would impact on the Congolese economy.

Therefore, a strong rebound in mainland China's demand is essential

for the Congolese economy to pick up in 2021.

Asia-Pacific

- APAC equity markets closed higher across the region; Hong Kong +2.0%, Australia/South Korea +1.9%, Japan/Mainland China +1.4%, and India +1.3%.

- Mainland China's provincial government of Hainan issued a batch

of supportive policies on 28 October, aiming to promote the

development of high-tech enterprises. These policies will be valid

through the end of 2022. (IHS Markit Economist Lei Yi)

- To encourage R&D investment, high-tech firms will receive subsidies worth 30% of their annual incremental R&D expenses, with an upper limit set at CNY2 million for large enterprises and CNY1 million for others.

- Enterprises first recognized as high-tech firms could be granted awards no less than CNY200,000. For high-tech firms newly moved to Hainan, incentives will be offered at 5% of first-year fixed-asset investment or 10% of R&D expenses, with an upper limit of CNY5 million.

- Additionally, the government will ensure enough land allocation for high-tech development, offer property and land-use tax alleviation for enterprises making large losses, and stepping up financial support for the high-tech sector.

- Newly unveiled supportive measures could bring an extra boost for the local high-tech sector, on top of the preferential tax arrangements introduced by the central government.

- China's State Council has signed off on the 2021-35 development plan for the country's new energy vehicle (NEV) industry. The development plan, proposed by Ministry of Industry and Information Technology (MIIT), outlines key targets for China to become a leader in the global NEV market. By 2025, the Chinese central government expects NEVs to account for 20% of new vehicle sales and, by 2035, regulators expect battery electric vehicles (BEVs) to become a main type of NEVs. China also aims to gain technology know-how in key areas of NEV development, including electric motors, batteries, and vehicle operating systems. By 2035, China aims to replace all the ICE models in the public sector with BEVs. The country also aims to speed up EV charging infrastructure development. Battery-swapping stations, for instance, have been included in the development plan as a supplementary charging infrastructure to fast chargers. (IHS Markit AutoIntelligence's Abby Chun Tu)

- Chinese electric vehicle (EV) startups NIO and Xpeng Motor have announced their deliveries in October. NIO's deliveries increased 100.1% year on year (y/y) to 5,055 vehicles last month, comprising 2,695 ES6, 1,477 ES8, and 883 EC6 vehicles. From January to October, NIO delivered 31,430 vehicles, up 111.4% y/y. As of 30 October, NIO had delivered a total of 63,343 vehicles. In a separate statement, Xpeng Motor said it delivered 3,040 vehicles in October, of which 2,104 units were P7 vehicles. Thanks to the improved sales results in October, Xpeng's combined deliveries of its two models, the G3 electric sport utility vehicle (SUV) and the P7 electric sedan, totaled 17,117 units from January to October, up 64% y/y. (IHS Markit AutoIntelligence's Abby Chun Tu)

- AutoX plans to expand its robotaxi testing operations in Beijing, western Chongqing, and two other unnamed cities in China. Xiao Jianxiong, chief executive of Pony.ai, said, "Chongqing brings new challenges as a hilly city." The company also revealed that it is in talks with potential investors to fund fleet expansion and development. In addition, AutoX will soon test its full-stack autonomous vehicle (AV) technology fitted in Fiat Chrysler Automobiles' Chrysler Pacifica minivans and will begin driverless testing in China, reports Reuters. AutoX has recently opened a robotaxi service for the public in Shanghai, after conducting trials with signed-up users. In addition to Shanghai, AutoX has received permits to test its AVs from Shenzen and Guangzhou in China and California in the United States. The company has set up an 80,000-square-foot facility for AV operations in Shanghai. The company has partnered with electric vehicle manufacturer NEVS to conduct a large-scale trial of robotaxis in Europe by the end of 2020. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Advance estimates show that Hong Kong SAR's economy bottomed

out in the third quarter of 2020, with quarter-on-quarter (q/q)

growth turning positive for the first time since early 2019, along

with narrower year-on-year (y/y) contraction. The stabilization in

local COVID-19 situations and the rebound in exports have provided

main support to the economy, although the fallout in the pandemic

locally and globally, coupled with travel restrictions and mainland

China-US tensions, will remain the downside risks to the near-term

outlook. (IHS Markit Economist Ling-Wei Chung)

- Preliminary data show that real GDP contracted 3.4% y/y in the third quarter of 2020, narrowing substantially from the above-9.0% y/y plunge in the first and second quarters, which came in the largest on record. Despite the deceleration, it still marked the fifth straight quarter of y/y contraction.

- In seasonally adjusted q/q terms, the economy showed signs of recovery as real GDP jumped 3% from the previous quarter, reversing a 0.1% fall in the second quarter. It also represented the first q/q expansion since the first quarter of 2019.

- The third-quarter 2020 improvement was mainly driven by a rebound in merchandise exports because of the recovery in mainland China's economy and signs of revivals in other regional economies. That said, domestic demand continued to lag behind as local sentiment and spending were restrained by the local resurgence of the pandemic and tighter social distancing measures in July and August.

- Exports of goods expanded 3.8% y/y in the third quarter, marking a reversal of a 2.2% y/y fall in the second quarter. It also represented the first increase since the third quarter of 2018. In September 2020, merchandise exports jumped 9.1% y/y, boosted by a 17.0% y/y surge in shipments to mainland China as the recovery there gained traction.

- Coupled with the continued expansions in exports to Taiwan and resumed growth in shipments to South Korea and Vietnam, they helped offset the double-digit declines in shipments to India, Japan, Singapore, and Thailand. Concurrently, exports to the US returned to a modest gain in September 2020, marking the first increase since November 2018, while shipments to Europe recorded a narrower decline during the month.

- On the other hand, exports of services continued to plunge in the third quarter of 2020, marking the fourth consecutive quarter of slumping by more than 20% y/y. With the tourism sector remaining at a standstill, the contraction in exports of travel services worsened further amid severe disruptions on inbound tourism.

- Tourist arrivals plunged 99.7% y/y in September, driven by the same rate of contraction in visitors from mainland China. Due to the outbreak and tightening social distancing measures and travel restrictions, tourist arrivals started to plunge by more than 96.0% y/y since February and over 99.6% y/y since April. Along with the interruptions on transport and business services, exports of services slumped 34.8% y/y, although narrowing from a record plunge of 45.6% y/y in the second quarter.

- Private consumption continued to shrink in the third quarter but at a slower pace as consumer sentiment was restrained by the resurgence of infections in July and August before improving in September when the pandemic situation began to stabilize and business activities gradually reopened. Private consumption dropped 7.7% y/y in the third quarter, decelerating from a 14.2% y/y slump in the second quarter, which marked the largest decline in history.

- This reflected a 12.9% y/y drop in retail sales in September, which came in similar to a 13.1% y/y decline in August but narrowed substantially from a 23.1% y/y slump in July.

- Tourist-related spending remained the hardest hit in September, led by a 25.7% y/y slump in sales of jewelry and other luxury items, although the rate of contraction decelerated from about 55% in June-July and around 75% in February-May. Other tourist-related spending, such as sales of medicines and cosmetics, followed a similar trend, down 45.5% y/y in September, after plunging 50-60% y/y during February-July.

- Concurrently, the slump in fixed investment, although remaining at double digits, narrowed to 11.2% y/y in the third quarter from 21.4% y/y in the second quarter.

- The economy has finally shown signs of bottoming out in the third quarter of 2020, after suffering the longest recession since the 1998 Asian financial crisis. As the economy has not yet recovered from last year's misfortunes caused by heightened political turmoil and mainland China-US trade tensions, the pandemic has added another severe blow to the already-battered economy.

- Mitsubishi Motors Corporation (MMC) has unveiled plans to raise the proportion of electric vehicles (EVs), including plug-in hybrid EVs (PHEVs) and hybrid EVs, in its total sales to 50% by 2030 as part of its revised Environmental Plan. According to a company release, the automaker also aims for a 40% reduction in the carbon-dioxide (CO2) emissions from its new cars as compared to 2010 and a 40% reduction in CO2 emissions from business activities as compared to 2014. "MMC will be fulfilling its responsibility as a manufacturer and seller of automobiles to make ongoing contributions toward a future dynamic, sustainable society," the automaker stated. The latest move by Mitsubishi is in line with changing environmental regulations in Europe, the United States, and other countries. In July, the automaker released its mid-term plan and revealed an intention to strengthen its line-up of eco-friendly models, such as PHEVs and EVs, by launching new models by fiscal year (FY) 2022. The plan also included introducing models including sport utility vehicles (SUVs), pick-up trucks, and multi-purpose vehicles (MPVs) in the Association of Southeast Asian Nations (ASEAN) region from FY 2022. (IHS Markit AutoIntelligence's Isha Sharma)

- South Korea's Ministry of Trade, Industry and Energy will launch a new division under its wing, which will be in charge of spearheading the development of future vehicles, in line with the country's blueprint on the automobile segment, reports Yonhap News Agency. According to the ministry, the new division, which will be launched on 11 November, will also center around developing technologies related to electric vehicles (EVs) and fuel-cell electric vehicles (FCEVs). The latest development is in line with the South Korean government's commitment to improve air quality in the country by bringing down particulate levels, fostering alternative-powertrain vehicles as the country's new growth engine and reducing its heavy reliance on imported oil. Hydrogen fuel has a strong potential to revive sluggish manufacturing businesses, including small and medium-sized enterprises, which in turn will create new jobs (see South Korea: 21 January 2019: South Korean government reveals FCEVs roadmap). Last week, the government unveiled its plan to boost the adoption of EVs and FCEVs in the country by expanding the number of charging stations and making such vehicles more affordable. Under the plan, the government aims to increase the number of EVs and FCEVs on the country's roads to 1.13 million units and 200,000 units, respectively, by 2025. (IHS Markit AutoIntelligence's Jamal Amir)

- Recent data show an essentially stagnant Malaysian economy,

largely in line with expectations. (IHS Markit Economist Dan Ryan)

- When the COVID-19 virus pandemic first struck, the ringgit weakened because of panic selling, as happened in many Asian countries. However, the currency has since recovered, and now appears to have found stability near 4.16 per USD.

- Bank Negara Malaysia has kept interest rates low and constant. This is likely to continue, even if the heightened Movement Control Order causes short-term economic damage.

- Consumer prices have lately been flat, a situation that should continue well into 2021. Wholesale prices have been more volatile and could fall further before stabilising along with the economy in mid-2021.

- Exports staged a strong rebound in June, as part of the post-lockdown recovery, but have been essentially flat (although volatile) since then. Imports have also been flat, leaving the trade balance in the USD3-6-billion range.

- The leading indicator has been bullish for months versus a year

earlier, but appears to be overly optimistic. The industrial

production index, however, has been essentially flat compared with

a year earlier.

Wholesale sales grew quickly in recent months, but remain depressed compared with last year. This probably reflects the consumer-facing part of the wholesale sector. - The unemployment rate has reflected the overall economy, with many people becoming jobless in early second quarter and then being rehired as growth resumed. From this point, the unemployment rate should remain relatively stable until improvement resumes in mid-2021.

- Consumer spending on normal retail goods remains down from the levels of a year earlier. Auto registrations are up, however, suggesting that households are still willing to spend on big-ticket items.

- Data for spending and output, as of August, had been relatively steady since the recovery from the low point in mid-second quarter. Similarly, price data for September are not showing strong trend changes, although wholesale prices will need to be watched closely.

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-november-3-2020.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-november-3-2020.html&text=Daily+Global+Market+Summary+-+November+3%2c+2020+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-november-3-2020.html","enabled":true},{"name":"email","url":"?subject=Daily Global Market Summary - November 3, 2020 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-november-3-2020.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Daily+Global+Market+Summary+-+November+3%2c+2020+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fdaily-global-market-summary-november-3-2020.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}