Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Aug 16, 2024

Global economic outlook: August 2024

Learn more about our data and insights

Early August's extreme market turbulence has abated, yet more volatile conditions are likely to persist. The exceptional volatility at the start of the month ought to be viewed in the context of "thin" markets, frothy equity valuations and an overreaction to the noise in some weaker-than-expected US economic data. The path forward will likely remain bumpy given numerous US-related uncertainties, including the risk of a hard landing, the timing and magnitude of policy rate cuts, the outcome of elections in November and their policy implications. The material change in Japan's monetary policy prospects and the related unwind of so-called carry trades will likely remain a source of market volatility.

An initial US rate cut in September is increasingly likely. US inflation figures have remained on an improving trajectory, while the US Federal Reserve is paying more attention to the second aspect of its dual mandate, labor market conditions, which have continued to soften. We await Fed Chair Powell's keynote speech at Jackson Hole later this month before making any major adjustments to our monetary policy forecasts. Still, given the prospect of an earlier start to US easing, we are likely to bring forward the projected timing of rate cuts in many other countries in our subsequent forecast update.

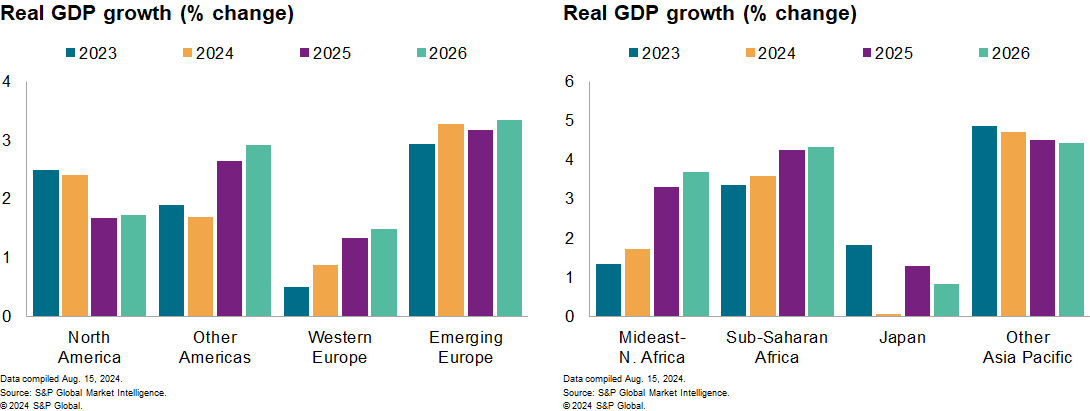

Recent US economic data do not signal an imminent lurch into recession. Although a hard landing cannot be ruled out with monetary policy still restrictive, our take remains that the economy is transitioning to a period of below-potential growth. July's US Purchasing Managers Indexes (PMIs) compiled by S&P Global remained indicative of continued growth, with signs of softening in manufacturing activity (beyond the US also; see below). July's rise in the US unemployment rate reflected a spike in the labor force — not typically a harbinger of recession. Other releases have also generally been consistent with slowing growth. Given stronger-than-expected real GDP data in the second quarter and updates to our tracking estimate for the third quarter, we have actually revised up the 2024 annual growth forecast, from 2.4% to 2.6%.

July's global PMI figures showed a mixed picture across the major sectors. On the soft side, the global manufacturing PMI slipped slightly below the expansion-contraction level of 50 for the first time this year. Weakness in new orders suggests the loss of momentum is likely to continue in the near term, with the signals for investment particularly soft. In contrast, the services PMIs generally remained resilient across most economies. While the global composite output index lost some ground in July, it remained at a level consistent with solid if unspectacular global growth momentum. Eurozone figures disappointed and we have trimmed our growth forecasts accordingly, from already relatively low levels.

The stability of global growth forecasts for 2024 and 2025 is somewhat misleading. Annual global real GDP growth is projected at 2.7% both this year and next, unchanged from our July forecast. However, a softer patch for quarter-over-quarter global growth rates looks increasingly likely in the second half of 2024, with investment and global trade hindered by heightened uncertainty. We expect a subsequent pick-up during 2025-26 as more accommodative financial conditions gradually filter through.

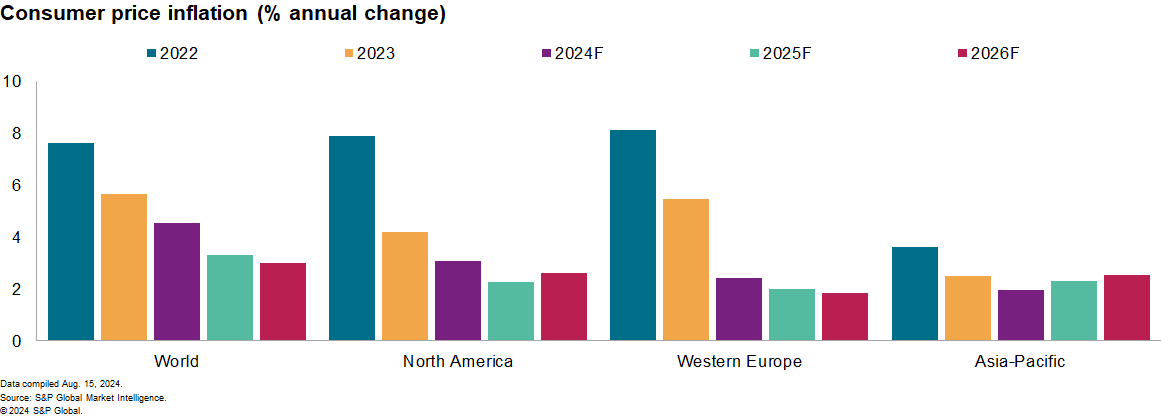

Disinflation continues, although we see near-term upside risks. Crude oil prices have rebounded from early August's lows. Business surveys show some further, albeit limited, lengthening of suppliers' delivery times. Container freight costs remain elevated. Disinflation in core goods is also bottoming out. The year-over-year consumer price inflation rate for core goods that we calculate for five key economies (the "G5 group") was negative for the third straight month in June, although on an annualized basis, it has been edging up since early in the year. The good news is that services inflation has finally started to come down more quickly. June's 0.4 percentage point fall in the "G5 group" of economies matched the largest decline since the rate peaked in early 2023.

Got 10 minutes? Hear Ken discuss key macroeconomic themes

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-economic-outlook-august-2024.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-economic-outlook-august-2024.html&text=Global+economic+outlook%3a+August+2024+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-economic-outlook-august-2024.html","enabled":true},{"name":"email","url":"?subject=Global economic outlook: August 2024 | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-economic-outlook-august-2024.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Global+economic+outlook%3a+August+2024+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fglobal-economic-outlook-august-2024.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}