Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

ECONOMICS COMMENTARY

Dec 16, 2024

Japan's private sector growth remains subdued and uneven while inflation intensifies

Japan's private sector expanded at the most pronounced pace in three months, albeit growing only modestly and with a deepening sector divergence. A quicker services expansion contrasted with a further reduction in manufacturing production.

Forward-looking indicators further outlined the likelihood for growth to remain reliant on rising services activity: manufacturing new orders, backlogs of work and business optimism all worsened in December.

Meanwhile price pressures intensified as rising cost pressures, partly driven by yen weakness, resulted in average selling prices increasing at the fastest pace in seven months. The latest data can therefore be viewed as supportive of the Japanese central bank proceeding with a rate hike in the near-term, though the impact on the manufacturing sector will be an area to monitor moving forward.

Japan's flash PMI signals fastest growth in three months

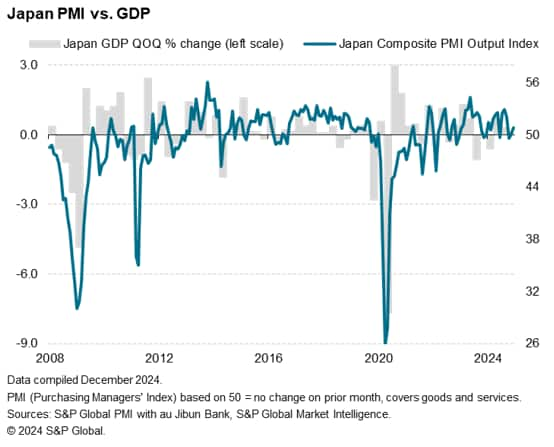

The au Jibun Bank Flash Japan Composite PMI, compiled by S&P Global, rose to a three-month high of 50.8 in December, up from a final reading of 50.1 in November. Posting above the 50.0 neutral mark for a second successive month, the latest reading signalled that Japan's private sector expanded marginally again after contracting fractionally at the start of the quarter. The latest PMI reading is indicative of another near-neutral GDP print in the final quarter of 2024.

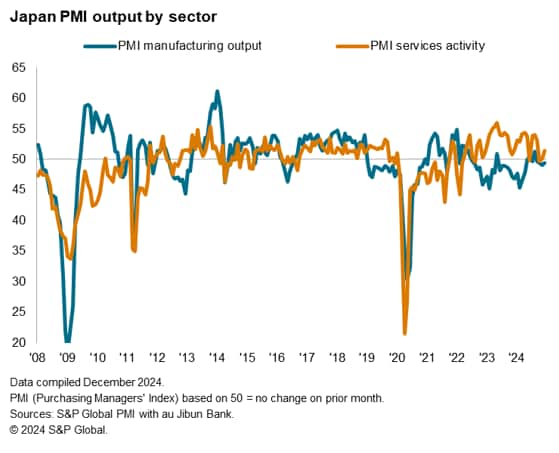

Services activity growth accelerates while manufacturing downturn persists

Growth remained services-driven at the end of 2024, with the rate at which service activity rose being the fastest since September. Higher services new business underpinned the latest expansion in services operations, as Japanese service providers highlighted how increased client demand and a widening of services offerings supported the uptick in new sales. The improvement in demand was limited to the domestic market, however, as export business contracted marginally again in December.

On the other hand, manufacturing production contracted for a fourth successive month. While modest, factories continued to report that client demand further dried up into the end of 2024. Domestic demand for Japanese manufactured goods notably fared worse compared to export demand, the latter rate of contraction easing to the softest in the current 34-month sequence.

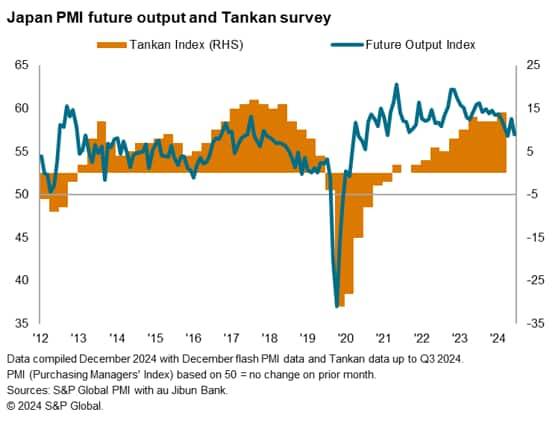

Forward-looking indicators outline likelihood for sustained divergence in sector performance

Forward-looking indicators, including the new orders and backlogs of work indices, meanwhile outline the likelihood for sector divergence to be sustained into the new year. While services new business growth accelerated, manufacturing new orders fell at a slightly quicker pace in December. Anecdotal evidence painted a picture of a general deterioration in market conditions, including in the semiconductor industry, underpinning the latest downturn in goods sales. And while unfinished business expanded for a second successive month for service providers, which is an indication of capacity pressure building, the level of backlogged orders in the goods producing sector fell at a solid pace once again, hinting at weaker production in the coming months.

A common theme across sectors, however, was a drop in confidence about the year ahead. Overall optimism slipped to the second-lowest level recorded in over three years. That said, both manufacturers and service providers maintained a level of optimism that was above their respective long-run averages.

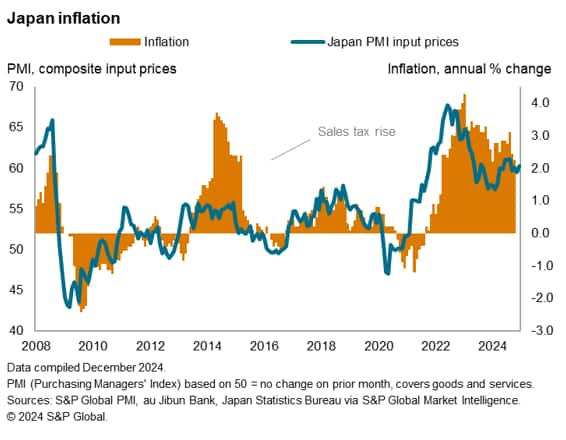

Selling price inflation at seven-month high

Price pressures rose in tandem with business activity growth at the end of 2024. The rate of selling prices inflation accelerated for a fourth consecutive month to the highest since May, running above the 2024 average. According to survey respondents, charges often rose as firms passed on higher input costs to clients. This was most prevalent to the service sector, where output price inflation was at an eight-month high while manufacturing selling price inflation eased on the back of subdued sales.

Higher raw material, transport and wage costs, partially underscored by weakness of the domestic currency, caused input prices to further rise in December. The rate of overall cost inflation inched up to a four-month high and was well above the long-run average.

Policy outlook

Ahead of the final Bank of Japan meeting for the year, where the market is mixed over whether another rate hike will be implemented, the December flash PMI data presented a picture of accelerating growth and still-elevated inflation. This is altogether supportive of the BoJ to raise rates in the near term, with the likelihood being in January, if not December. The impact on the manufacturing sector will need to be monitored, however. On the one hand, higher rates may help to combat the impact of the weak yen, but on the other hand, potential pressure on demand may ensue.

Access the full press release here.

Jingyi Pan, Economics Associate Director, S&P Global Market Intelligence

jingyi.pan@spglobal.com

© 2024, S&P Global. All rights reserved. Reproduction in whole

or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fjapans-private-sector-growth-remains-subdued-and-uneven-while-inflation-intensifies-dec24.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fjapans-private-sector-growth-remains-subdued-and-uneven-while-inflation-intensifies-dec24.html&text=Japan%27s+private+sector+growth+remains+subdued+and+uneven+while+inflation+intensifies+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fjapans-private-sector-growth-remains-subdued-and-uneven-while-inflation-intensifies-dec24.html","enabled":true},{"name":"email","url":"?subject=Japan's private sector growth remains subdued and uneven while inflation intensifies | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fjapans-private-sector-growth-remains-subdued-and-uneven-while-inflation-intensifies-dec24.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Japan%27s+private+sector+growth+remains+subdued+and+uneven+while+inflation+intensifies+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fjapans-private-sector-growth-remains-subdued-and-uneven-while-inflation-intensifies-dec24.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}