Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Feb 10, 2023

The shifting global semiconductor landscape in Asia-Pacific

Rapid and far-reaching changes in the public policy landscape for semiconductors manufacturing in the US and European Union during 2022 will have important direct implications for the semiconductors industry in Asia Pacific economies.

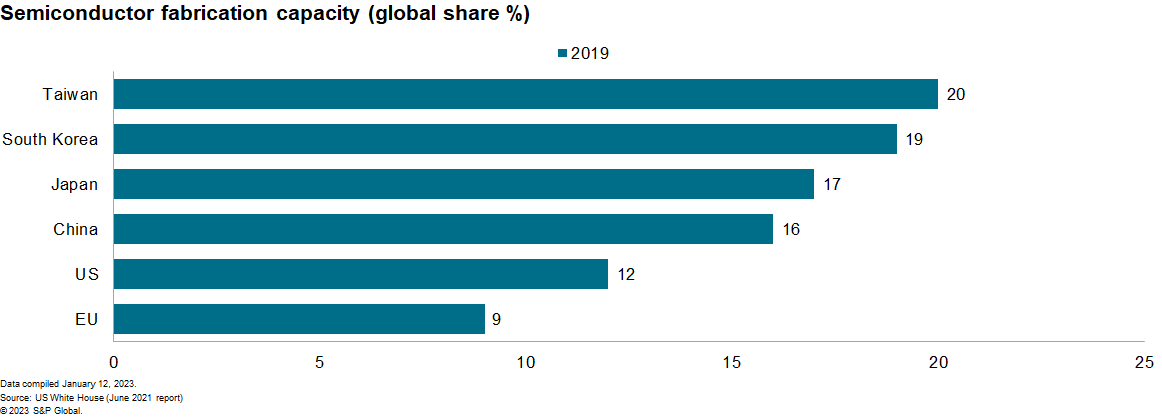

Legislation in the US and EU aims to boost domestic and regional semiconductors manufacturing significantly, threatening to rebalance global semiconductors manufacturing away from Asia Pacific economies. Taiwan, South Korea, Japan, and mainland China accounted for 72% of global semi-conductor production in 2020, with prior production locations such as the US and Japan focused on the more profitable design segment.

The December 2022 announcement by Taiwan Semiconducting Manufacturing Co. (TSMC) that it would triple investment in manufacturing capacity in the US signaled the changing geographic dynamics in the sector. Policies favoring economic nationalism and/or supply chain security in Japan, South Korea, and India by encouraging local manufacturing development will further adjust the landscape, with more locations seeking to develop onshore production and to reduce reliance on supply from Taiwan.

In the three- to five-year outlook, policy factors are likely fundamentally to alter the sector landscape, with increased investment and new business opportunities outside Asia Pacific for semiconductor manufacturing and greater competition within the region.

How we got here

Taiwan's TSMC pioneered the 'contract manufacturing' model in the 1980s, focusing solely on manufacturing chips designed by outside firms on increasingly complex and expensive nodes. Previously dominant industry participants in the US and Japan have converted to outsourcing designs to be manufactured abroad, including in Taiwan.

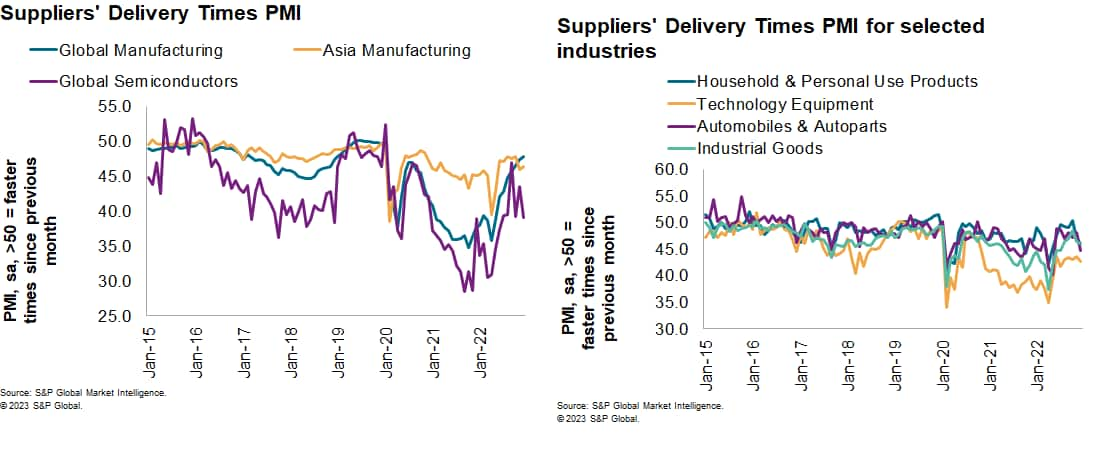

Recent semiconductor shortages have highlighted the sector's reliance on effective functionality within global supply chains, including those in the Asia Pacific region. S&P Global's Purchasing Managers' Indices (PMI) showed that input delivery delays experienced by semiconductor firms were more acute than those elsewhere within the global manufacturing sector and in Asia at an aggregate level.

Global supply chains have not yet fully recovered, with many industries continuing to experience severe delays and acute inflationary pressures, albeit far less severely than in 2021. Recent S&P Global Price and Supply Monitor data showed that reports of supplier shortfalls for semiconductors in October 2022 were among the lowest since December 2020. Even then, they were still above long-run trends, indicating that shortages are likely to persist into 2023.

US response

During the pandemic, when factories were shut and supply chains disrupted, US policymakers decided to extend support to existing efforts to alter the US semiconductor supply chain to avoid future potential supply shocks.

The US has pursued a pro-active policy to re-establish domestic production, encouraging this both via legislation and through the implementation of new restrictions on exports of advanced semiconductors, sector-related machinery, and advanced semiconductor manufacturing technology to mainland China.

Aside from the existing export limitations associated with the CHIPS Act and other executive orders, the Biden Administration is likely to expand trade controls further in 2023, targeting specialty technologies.

EU policy

The EU approach in large part envisages the reshuffling of existing EU funding programs into targeted measures rather than raising new funds to support the development of semiconductor technologies and processor chips. However, it is at an advanced stage of preparation for a new initiative seeking to increase the EU's modest share of the different phases of semi-conductor production.

The bloc is also very likely to focus on expanding co-operation with what it deems "likeminded" partners — namely, the US, Japan, South Korea and Taiwan — to mitigate semiconductor supply chain risks, including raw materials supplies.

The EU will probably also use competition, trade, and investment defense instruments to address what it sees as unfair trade practices and distortions such as state subsidies from outside the EU, with markets such as mainland China likely to be exposed to regulatory action.

Taiwan's approach

Taiwan is the global leader in high value contract-based semiconductor manufacturing. In 2020 TSMC alone accounted for over 50% of global semiconductor manufacturing revenue.

Since 2016, the Taiwanese government has pursued a policy of reshoring manufacturing, including efforts to improve the supply of domestic semiconductor manufacturing equipment to account for 60% of local needs by 2030.

The Taiwanese government has also taken a greater role to regulate the industry, including protectionist measures to prevent technology transfers or the poaching of Taiwanese engineering talent.

Other Asia-Pacific policies

South Korea's "K-semiconductor Strategy" - a USD450 billion plan to develop a comprehensive semiconductor manufacturing supply chain by 2030 - has been largely driven by concerns over the country's dependence on mainland China and Taiwan for high-value semiconductor imports, particularly non-memory chips, in addition to a large Korean manufacturing presence in mainland China.

The Japanese government has expressed renewed interest in achieving "strategic autonomy" and "strategic indispensability" within the semiconductor manufacturing industry and within industry-related global supply chains. This would probably involve increased co-ordination with the US in restricting advanced technology exports to mainland China.

India so far has no domestic capacity for commercial semiconductor production. The changing regional policy agenda to favor greater self-sufficiency in semiconductors has encouraged policies by Prime Minister Narendra Modi's government to initiate India's presence in the sector. The Indian government is keen to position itself as a trusted partner country where critical semiconductors can be developed.

Mainland China's policy

The Chinese government regards semiconductor manufacturing as a strategically important industry. While mainland China manufactured nearly 35% of the world's semiconductors in 2021 - consisting primarily of less sophisticated, low value chips - it remains a net importer of chips, consuming roughly 40% of global supply.

Notably, mainland China remains one of the largest importers of Taiwanese semiconductors. Mainland China is also a leading supplier and refiner of metals and rare earth materials needed for manufacturing semiconductors.

US sanctions on certain exports of advanced semiconductors technology to mainland China represent at least a near-term constraint for its ambitions to develop a domestic semiconductors manufacturing industry. These policy measures will also have implications for the location of downstream electronics manufacturing processes requiring the use of advanced semiconductors technology.

To counteract these restrictions, mainland China will continue to invest heavily in the development of end-to-end "sanction proof" supply chains. It is also likely that the Chinese government will leverage its position as the largest trading partner of key semiconductor producers in the Asia Pacific region, including Japan, South Korea, and Taiwan, and threaten economic retaliation against countries that participate in US efforts to restrict mainland China's technological development.

Outlook

Both the US and the EU have introduced policies to encourage the development of local semiconductors production capacity and reduce mainland China's access to complex technologies for manufacturing advanced semiconductors.

Policies favoring economic nationalism and/or supply chain security in Japan, South Korea and India by encouraging local manufacturing development will further adjust the sector landscape. More locations will seek to develop onshore production, creating greater competition within the Asia-Pacific region. Mainland China also has the clear objective of building its own technological sector and to reduce dependencies on Western inputs.

-With contributions from Jeffery McElroy.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fthe-shifting-global-semiconductor-landscape-in-asiapacific.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fthe-shifting-global-semiconductor-landscape-in-asiapacific.html&text=The+shifting+global+semiconductor+landscape+in+Asia-Pacific+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fthe-shifting-global-semiconductor-landscape-in-asiapacific.html","enabled":true},{"name":"email","url":"?subject=The shifting global semiconductor landscape in Asia-Pacific | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fthe-shifting-global-semiconductor-landscape-in-asiapacific.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=The+shifting+global+semiconductor+landscape+in+Asia-Pacific+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmarketintelligence%2fen%2fmi%2fresearch-analysis%2fthe-shifting-global-semiconductor-landscape-in-asiapacific.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}