Discover more about S&P Global's offerings

Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Aug 28, 2023

August US auto sales trends remain familiar

New light vehicle sales in August are expected to be up double digits from year-ago, while maintaining pace with July results

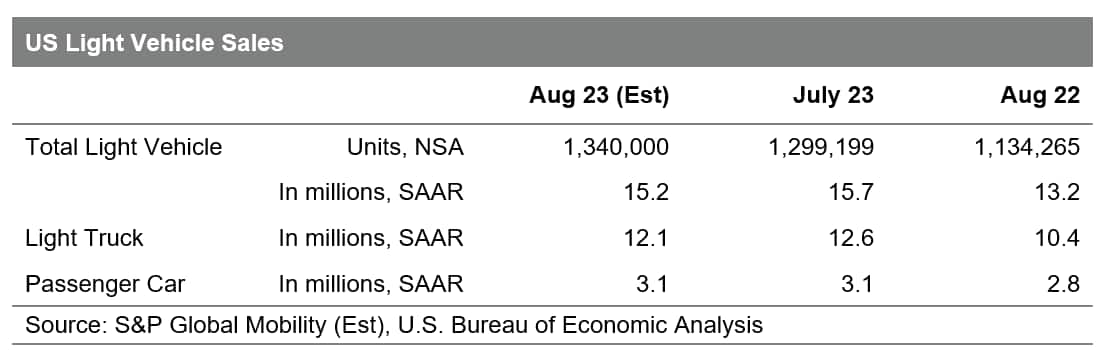

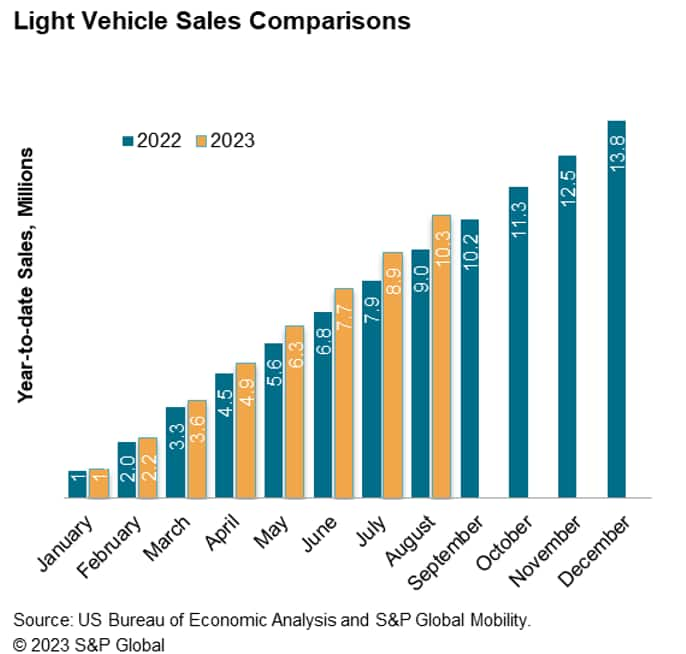

S&P Global Mobility expects US light vehicle sales in August to remain steadfast in a challenging environment, with a volume estimate of 1.34 million units. The projected August result would be up 18% year over year, however compared to the month-prior result, growth would be a milder 3% even with two more selling days. This translates to a seasonally adjusted annual rate (SAAR) of 15.2 million units, down from a July 2023 reading of 15.7 million units.

While the year-over-year growth in the market will be sustained in August, there are some faint indicators of market softening. The daily selling rate metric, since peaking at 54,500 sales per day in April, has realized a mild downward trend since. With 27 selling days in August, and an estimated volume of 1.34 million units, the daily selling rate metric would fall below 50,000 units for the first time since February 2023. S&P Global Mobility analysts project calendar year 2023 total light vehicle sales of 15.4 million units. Although the daily selling rate has diminished over the past three months, we do not expect this metric to further decline over the remainder of the year.

"New vehicle affordability concerns will not be quick to rectify," reports Chris Hopson, principal analyst at S&P Global Mobility. "Rising interest rates, credit tightening and new vehicle pricing levels slowly decelerating remain pressure points for consumers."

In terms of total dealer-advertised inventories, volumes have stayed relatively static since the beginning of July - at around 2.3 million units, with upward and downward variations of ~100,000 units over the course of a sales month, according to Matt Trommer, associate director of Market Reporting at S&P Global Mobility.

On a year-over-year basis, compared to mid-August 2022, inventories have risen by 57% from just shy of 1.5 million vehicles, Trommer said. (Note that total advertised inventory figures include a fractional percentage of vehicles that dealers may have sold but are still advertising, as well as vehicles allocated to dealers but are still in transit.)

Various risk factors beyond the US consumer also remain prevalent in the outlook for the remainder of 2023, including the potential for North American vehicle supply disruptions as union negotiations emerge.

"The greatest threat to the forecast in the near-term surrounds the union negotiations between the United Auto Workers (UAW) in the US and Unifor in Canada with their respective contracts set to expire in mid-September 2023," said Joe Langley, associate director at S&P Global Mobility.

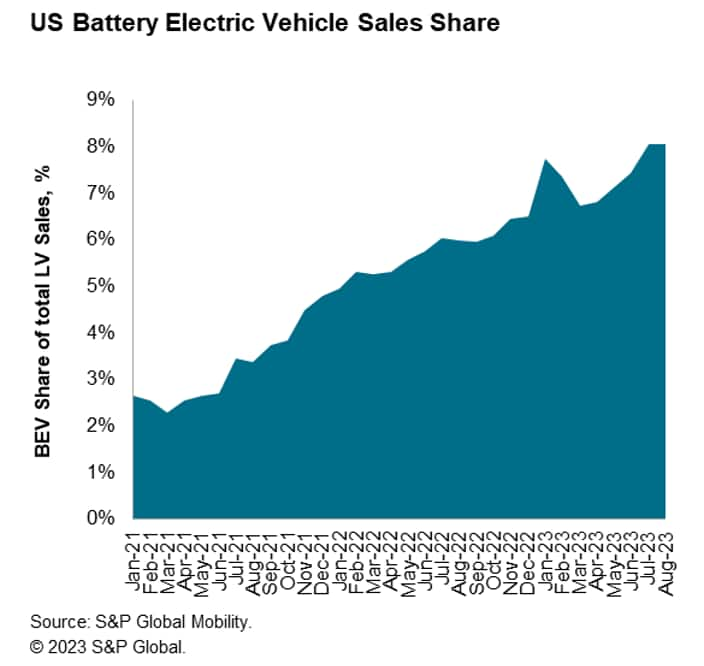

Continued development of battery-electric vehicle (BEV) sales

remains a constant assumption for 2023 although some month-to-month

volatility is expected. BEV share is expected to 8.0% of August

sales, remaining on trend with the preceeding month. Looking at the

remainder of the year, beyond potential future pricing developments

by Tesla, a sustained churn of new and refreshed BEVs and

aggressive BEV production expectations will continue to promote BEV

sales as the year progresses.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2faugust-us-auto-sales-trends-remain-familiar.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2faugust-us-auto-sales-trends-remain-familiar.html&text=August+US+auto+sales+trends+remain+familiar+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2faugust-us-auto-sales-trends-remain-familiar.html","enabled":true},{"name":"email","url":"?subject=August US auto sales trends remain familiar | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2faugust-us-auto-sales-trends-remain-familiar.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=August+US+auto+sales+trends+remain+familiar+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2faugust-us-auto-sales-trends-remain-familiar.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}