Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

US Automotive Market Share Wars Will Resume in 2023

Recovering inventories are increasing dealer stock, while interest rate hikes and economic headwinds will dampen demand - forcing OEMs and dealers to make deals once again. The question is: Who will blink first?

By Mark Rechtin, Executive Editor, S&P Global Mobility

After nearly two years of inflated new- and used-car prices - with car dealers asking consumers to pay thousands of dollars over MSRP - the US industry is primed for a reset to previous competitive norms.

A combination of industry factors and macroeconomic conditions could trigger a potentially bloody battle for market share this year, according to an analysis by S&P Global Mobility. Automakers and dealers that have grown accustomed to huge profits on vehicles sold as soon as they leave the factory will see a return to traditional conditions of accumulating showroom inventories and the need for incentives to move the metal.

This could mean a big win for consumers still in the market for a new or used vehicle, and who are not intimidated by sharply increased lending rates or other economic headwinds. Already there are signs of increased new-car inventories and declining used-car prices - though not yet to pre-COVID levels.

"Things will heat up this year when the first tranche of COVID-sold vehicles starts returning to market," predicts Dave Mondragon, vice president of product development for S&P Global Mobility. "These vehicles are all underwater. They were sold at record-high prices with no discounts, and there will be little to no equity to roll into a new vehicle."

It's not so much the volume of vehicles coming back - new-vehicle sales cratered in 2020 when production lines slowed due to supply chain snarls. But the practice by many dealerships of using vehicle shortages to sell at inflated prices means nearly every vehicle coming back has massive negative equity - with the customer owing thousands of dollars more than the vehicle is worth at trade-in. "That's when discounting starts up again," Mondragon says.

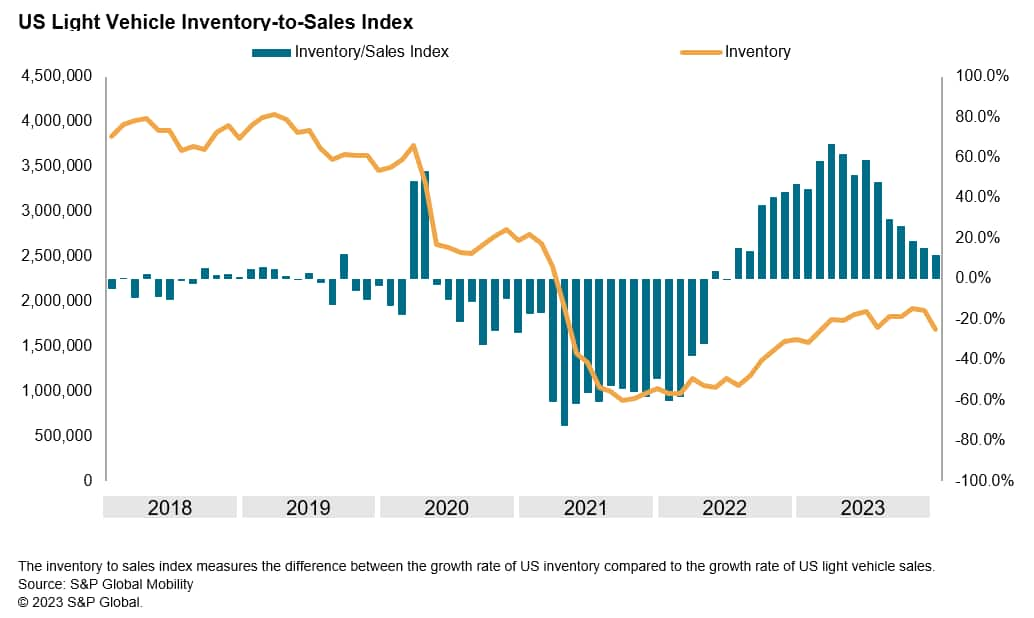

Inventory Rebounding

With supply chain snarls easing, an S&P Global Mobility analysis of inventory data shows a 91% increase in advertised new-vehicle dealer stock at the end of December 2022 compared to February, a sharp 43% uptick compared to August 2022, and a 21% jump compared to October.

"Though we're not back to historical norms, inventory pressures are starting to ease," said Matt Trommer, S&P Global Mobility associate director of innovation product management for in-market reporting.

"The only real difference was domestic and European brands seeing improved inventories earlier in 2022, and Asian brands ramping up to a greater extent in the second half of '22 after actually going down in the February-to-August period," Trommer said. "In a few cases, we're seeing inventories coming up quite a bit. Jeep, GMC and Mazda are now showing a broad availability of vehicles. Other brands such as Honda, Kia and Subaru, however, are showing more limited availability."

"We're in the formative stages of inventory rebuilding following six months of year-over-year increases that ended 35 months of year-over-declines in July 2022," said Joe Langley, associate director of research and analysis for S&P Global Mobility's North American Light Vehicle Forecasting & Analysis team. "Stellantis is the closest to having normalized inventory. They are going to have to ask themselves, 'What do we do next?'"

In December, Ford, Chevrolet, Ram, and Jeep had about 300,000 units of leftover 2022 models advertised as available for sale. Those four brands accounted for 71% of 2022 advertised inventory listed by mainstream brand dealers - and 66% of all dealer-advertised inventory when including luxury marques. Among luxury brands, Mercedes-Benz and Lincoln still showed the most remaining 2022 vehicles in dealer advertised inventory, according to the S&P Global Mobility analysis.

That said, not every brand will be in the same circumstances. After the initial semiconductor crunch, GM, Ford, and Stellantis better managed their supply chains and are closer to being back to traditional production levels; the Japanese brands are still struggling with supply-chain issues. While less impacted, Hyundai and Kia are also dealing with structural issues of not having enough factory capacity to meet growing demand.

"We're seeing the US3 being the closest to normalized inventory and they will have to start asking themselves hard questions relating to production planning, product mix and pricing along with incentives activity," Langley said. "The surprise of 2023 will be vehicle availability. It will still be well below industry norms, but inventory for the spring selling season will be up 50-70% from 2022 levels."

Another element that could factor into increased consumer power in the new-car arena: A softening in inflated used-car values.

When COVID shut down new-car manufacturing, demand (and prices) for used cars soared starting in early 2021. Data from CARFAX, part of S&P Global Mobility, shows that - pre-COVID - average weekly dealer listing prices for used cars had held steady, slightly above $19,000. The first quarter of 2021 saw a rapid price shock that resulted in peak pricing of $29,025 in Q1 2022. But last fall, used-car prices started retreating. By mid-December, CARFAX data showed a retreat to $27,239. And while prices are nowhere near pre-COVID levels, there is no evidence that inflated prices will hold.

One potential easing of a price crash: A momentary drop-off in off-lease cars coming back during the three-year anniversary of the COVID shutdown, when sales cratered for several months in 2020. A shortfall in the certified-pre-owned segment might resume demand pressure on the new-car side and temporarily hold prices steady.

External Forces

There are usually multiple causes of swings in market behavior, and it appears US light vehicle sales have a perfect storm of culminating events that will come to a head starting in spring 2023: In addition to rebounding vehicle inventories, a sharp rise in U.S. lending rates, inflation leading to lower disposable income among households, and nervy macroeconomic headwinds are worrying US consumers.

Already there are storm clouds on the horizon in terms of demand destruction. The daily new-car selling rate metric remained remarkably steady in the second half of 2022, even while some pockets of inventory accumulated. While stubbornly sticky low levels of inventory dampened year-end clearance incentives, any backward movement in the daily selling metric to begin 2023 could be signal of a retrenching auto consumer.

Households are eyeing the uncertain economy as a reason to hold back on new purchases. If workers do not receive 2023 pay raises commensurate with 2022's sudden inflationary spike, and large-scale layoffs continue, that will prompt conservatism in household capital expenditures.

"Ongoing supply chain challenges and recessionary fears will result in a cautious build-back for the market," said Chris Hopson, manager of North American light vehicle sales forecasting for S&P Global Mobility. "US consumers are hunkering down, and recovery towards pre-pandemic vehicle demand levels feels like a hard sell. Inventory and incentive activity will be key barometers to gauge potential demand destruction."

From a forecasting perspective, S&P Global Mobility recently downgraded the US demand settings for 2023 due to darkening economic clouds. The immediate release of pent-up demand of the past two years that many OEMs anticipated would absorb increasing production is now wavering, and may be eliminated altogether if consumers retrench their spending habits. This will prompt downward pressure on vehicle pricing.

Who Blinks First?

Where will the discounts first appear? Likely in full-size trucks. GM, Ford and Stellantis need full-size truck volumes and profits to support investment in their electrified futures. GM is the only one of the three that has incremental capacity to produce more full-size pickups - whether they're ICE or BEV. Ford is capacity-constrained until Blue Oval City comes online in the second half of 2025, and Stellantis has their own limitations in the short-term.

"This essentially puts GM in the driver's seat if they want to increase incentives to drive additional volume. If they do this, Ford and Stellantis will be forced to follow," Langley said. "There is still room for these manufacturers to increase incentives on their pickups and still be ahead on the revenue side if they experience comparable sales improvements from those higher incentives."

After all, pre-COVID incentives on big pickups were running $6,000 per unit in January 2020, and the Detroit automakers were still profitable. But recently, demand for pickups has waned as more buyers move to SUVs.

Despite full-size pickups' important contributions to each brand's business case and factory output, the share of half-ton retail sales has been declining for more than two years, according to S&P Global Mobility data. The segment's retail share in Q3 2022 was 7.8% - lower than in any other quarter dating back to Q3 2012.

Another area of potential incentive skirmish? Likely in a high-volume segment with plenty of players, such as mainstream compact SUVs. In addition, a competitive luxury market with additional pressure from Tesla could see a higher-end brand with resurgent inventories use the opportunity to grab share. Meanwhile, Tesla's recent price cuts across its lineup could prompt a price war in the BEV space.

At least one luxury automaker has stated it is openly looking at conquesting its rivals, and is already injecting money into the market to capture share. They see it as a once-in-a-lifetime opportunity, and are thinking that investing earlier in incentives - either cash on the hood, or subsidized lending rates - will result in the best chance to grab share. Meanwhile, another luxury brand with already strong days' supply is cranking up subsidized lease deals.

The next automaker's sales chief willing to cede market share without a fight will be the first one. Performance bonuses, career trajectories, and factory output requirements hinge on it. Furthermore, failing to spend to retain market share has downstream costs: The cost of losing loyal customers, multiplied by the cost of thousands of conquests needed to replace them, must also be considered. Also, automakers' and suppliers' factories need to run at high percentages of capacity to be profitable. Lofty talk of inventory control sounds great, until just-built vehicles start stacking up in factory-overflow lots.

Remember: Average transaction prices in December were $49,500, so for every 20,000 vehicles built, OEMs can generate nearly $1 billion in revenue - a tempting carrot for OEMs when revenue goals are under pressure.

As a result, spring and summer of 2023 could force automakers into aggressively pursuing customers with incentives while attempting to maintain the healthy profit margins they have seen for the past two years.

The upshot will be a chaotic accordion effect in monthly sales results, as fluctuating inventories run head-on into unsettled consumer confidence and numerous industry and macroeconomic conditions. Automakers and dealers will be hard pressed to find a consistently successful sales strategy that allows them to maintain or increase share during such uncertain times.

Feature your exclusive automotive industry insights on our Mobility News and Assets Community page, a platform that is designated for automotive and mobility industry thought leaders and the community.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.