Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

Truck market 2024: Class 4-8 anticipated growth in North America

After truck market supply-chain disruptions in 2021 and 2022, North America's medium and heavy commercial vehicle (MHCV) sector is poised for recovery in 2024.

In North America, the United States accounts for approximately 80% of commercial vehicle demand. Following the COVID-19 pandemic, the United States' economy and commercial vehicle market have demonstrated remarkable strength. By extension, Mexico benefits from cross-border trade with the US, bolstered by a strong local currency and an influx of competitively priced imports from China. In Canada, anticipated economic growth and a rise in private consumption and investment also signal a robust commercial truck market.

S&P Global Mobility's research, focusing on Class 4-8 commercial trucks in North America, truck market forecasts continued growth in 2024 and 2025. Analysts from the Mobility team spoke to external audiences about this truck market outlook after the second-quarter forecast update, in May 2024, during a recorded session.

Our most recent truck market forecast release in August 2024 re-confirmed the shape of the outlook for the region, with minor changes. This forecast aligns with economic indicators such as growth in housing construction and personal consumption, the latter of which is expected to moderate. However, interest rates might see a downward adjustment in the latter half of 2024, which could also stimulate a faster-than expected rebound, depending on the scale and timing of the adjustment.

Truck Market Trends for Medium-Duty and Heavy-Duty Trucks

Below the top macro-economic indicators influencing this forecast lies truck tonnage, which refers to the total weight of cargo or freight transported by commercial trucks. This is not just a number. It is a barometer for the trucking industry's efficiency and a reflection of economic vitality.

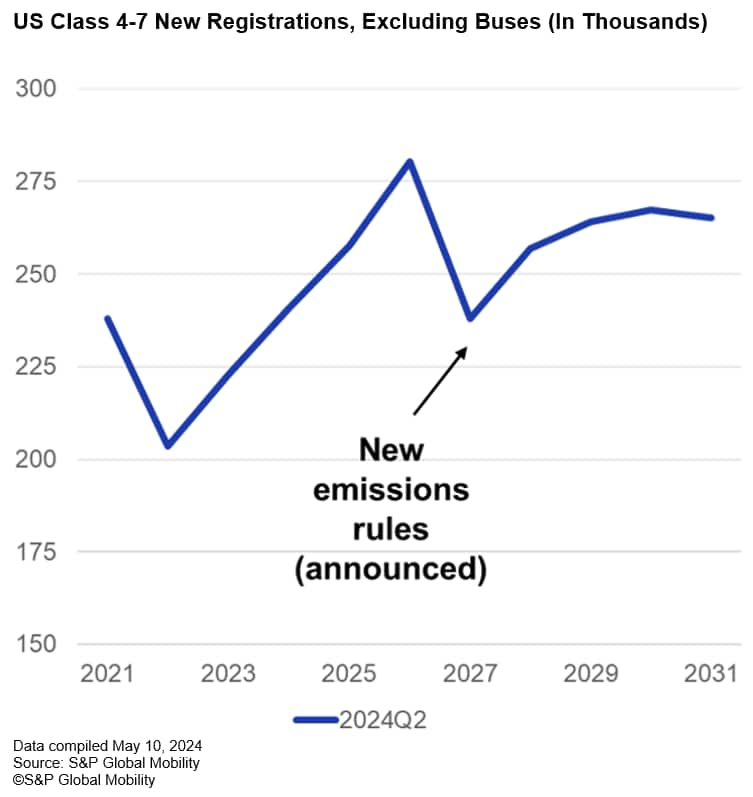

Despite a tepid performance in 2023, truck tonnage is projected to gain momentum in the next two years, as consumer spending continues to expand, suggesting more demand for commercial trucks on the roads to meet consumer and business needs. Notably, the medium-duty truck market, spanning Class 4 to Class 7, is expected to grow consistently through 2025. This sector is susceptible to regulatory shifts, with looming emission standards set for 2027 likely to drive a surge in purchases as fleets and customers look to capitalize on pre-regulation models.

There are divergent trends across different weight classes in the medium-duty truck market. Class 6 trucks that are popular in the lease and rental spaces—such as the Freightliner M2 106, Hino L6, and Ford F-650—are also popular choices for delivery services related to construction and housing like towing and delivery.

In 2023, Class 6 trucks saw a strong year, largely driven by the delivery of previously ordered vehicles linked to the surge in housing and construction activity. However, the fundamentals of the housing market are currently weak, and the sales volume of Class 6 trucks is expected to dip in 2024.

In contrast, Class 5 trucks are projected to thrive. Class 5 trucks are increasingly important for utilities and municipalities, and as the population grows in North America, the demand for these commercial trucks are expected to increase. In addition, the growth in online shopping and e-commerce has led to higher demand for delivery vehicles like Class 5 trucks.

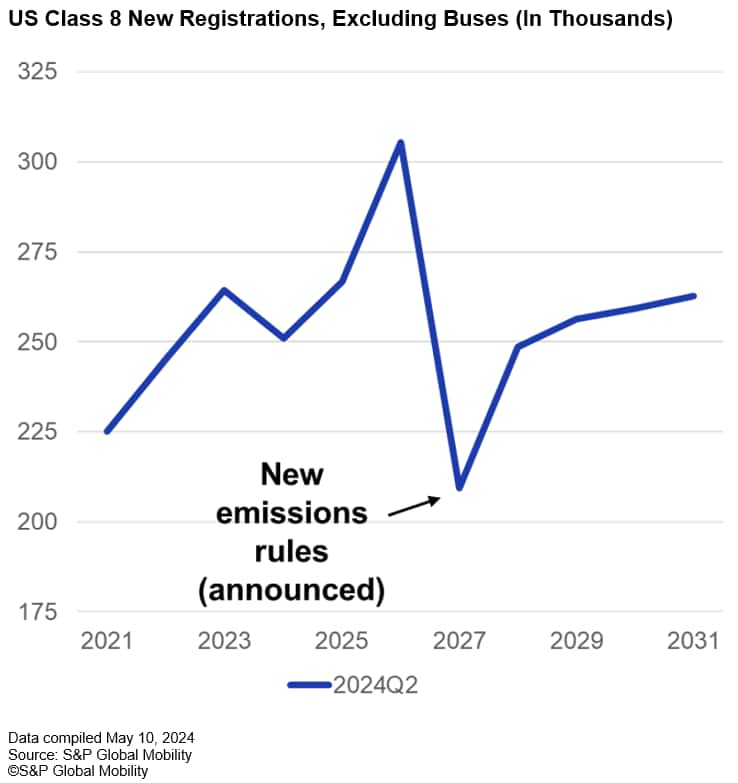

Class 8 trucks are about half the MHCV production volume in North America. These include the Freightliner Cascadia, currently the top MHCV truck in the region by production volume; the International LT; PACCAR's Peterbilt 589; and the Mack Anthem for long-haul transportation. The growth of Class 8 trucks is expected to face challenges in 2024, attributed mainly to ongoing supply chain constraints and adverse conditions in long-distance trucking.

The Future Truck Market Outlook and Shift Toward Sustainable Powertrains

The truck industry is anticipating a strong 2026 after fluctuations in 2024 and 2025, with less volatility than expected. New models, including Volvo's VNL and the latest generation Freightliner Cascadia, will debut during this timeframe. The surge in truck production will fall by 2027 with the newly proposed EPA 27 emission regulations and increased compliance costs.

Mexico's heavy truck market shows signs of vigorous growth, driven by solid replacement demand against an aging fleet and boosted by a robust local currency and competitively priced imports. Major truck OEMs like Daimler Truck, PACCAR, Traton, and Toyota have a significant presence in Mexico. The presence allows them to adjust their production mix between similarly tooled plants in the United States and Mexico to better respond to truck market demands and production needs.

Conversely, Canada's smaller truck market is expected to see a surge in private consumption and investment, potentially propelling strong demand for Class 8 trucks.

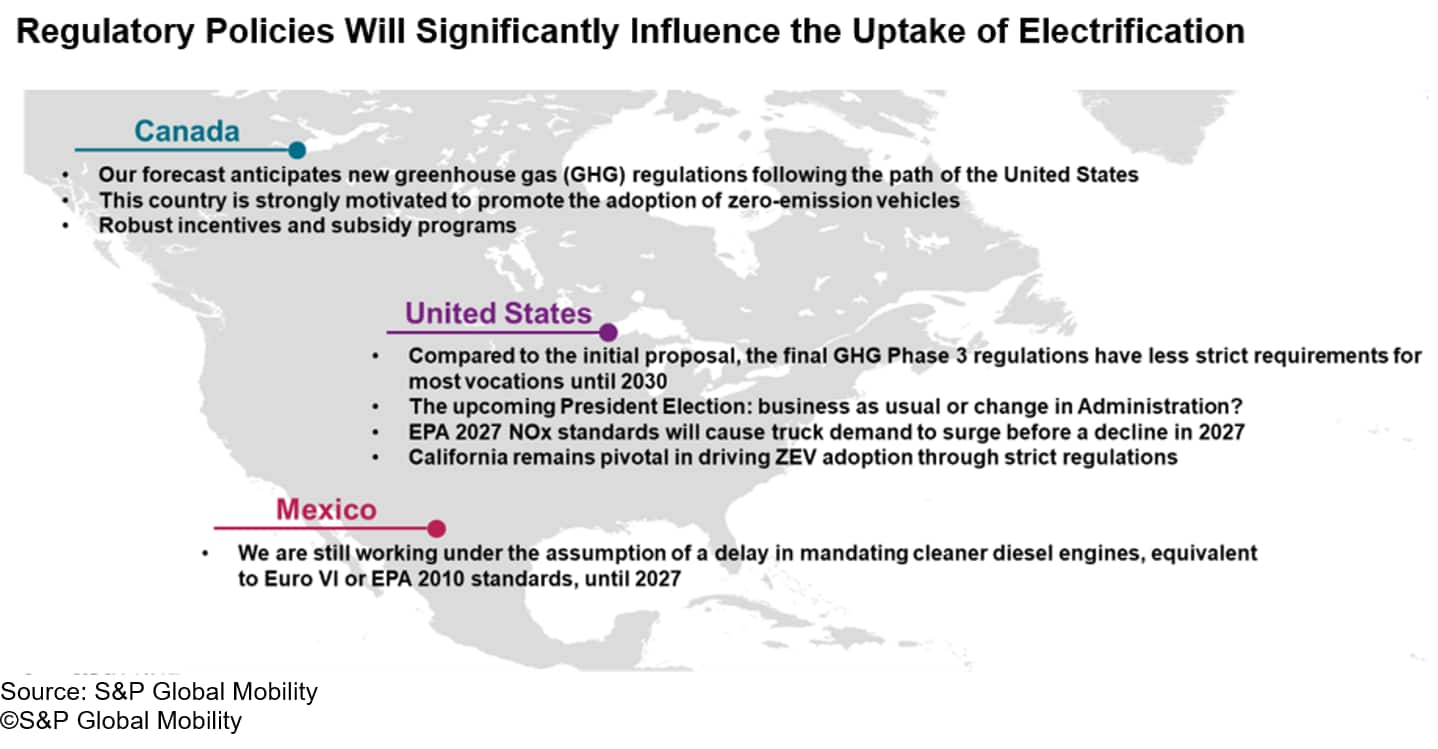

North America's MHCV market narrative is also characterized by the shift toward more sustainable and regulation-compliant powertrain technologies. Canada, the United States and Mexico each have unique regulatory trajectories that will significantly influence fuel type forecasts and vehicle design.

In this regard, zero-emission vehicles (ZEVs), including battery electric vehicles (BEVs), are gaining traction. However, the market's readiness and enthusiasm vary by country and are influenced by regulatory frameworks and market dynamics. The United States will reach an important milestone with new emissions standards in 2027, as described previously.

In neighboring Mexico, a new emissions standard will also be implemented in the middle of the decade. At the time of our truck market forecast release, our assumption was this would be 2027 for Mexico; however, as of this writing, evidence is mounting that the change will come earlier, in 2025, in line with a previously announced timeline.

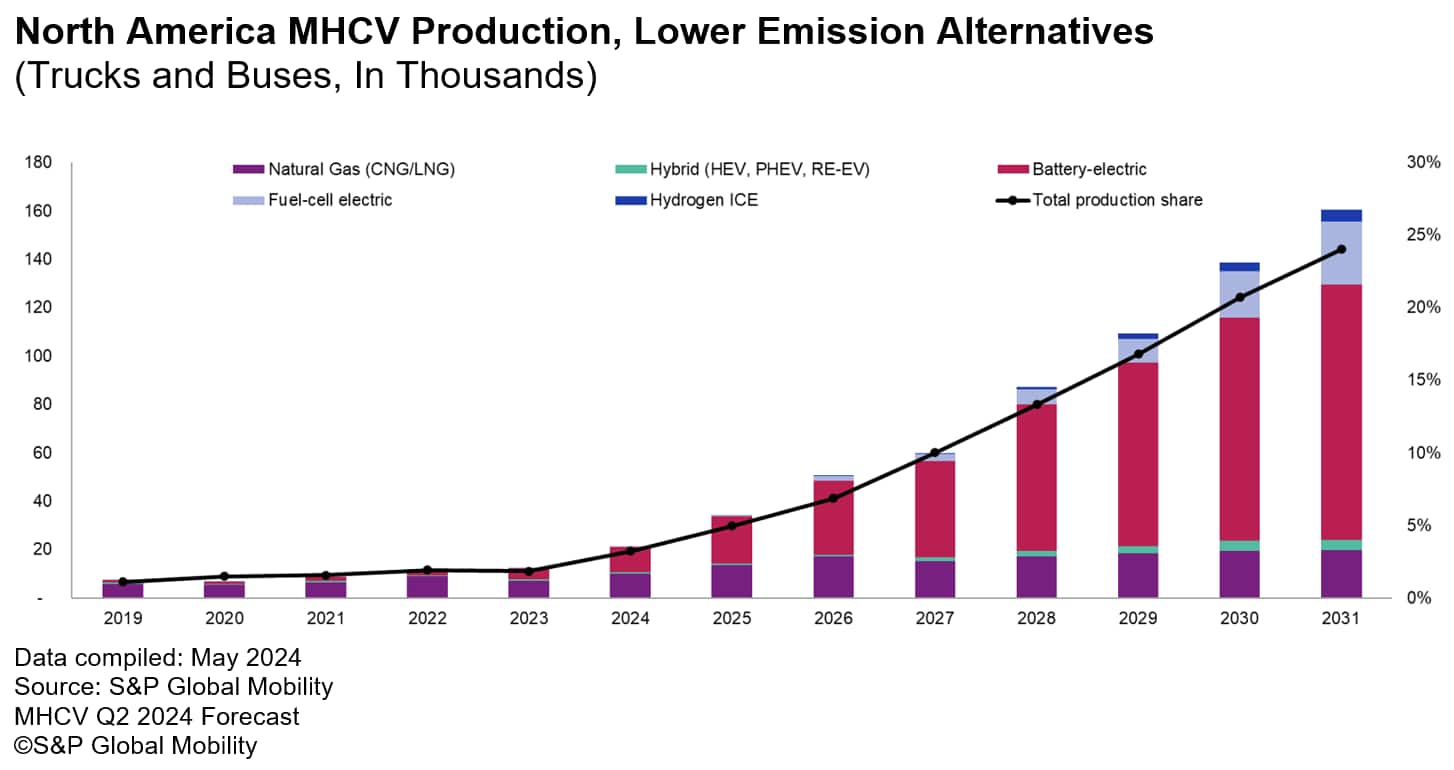

While internal combustion engine (ICE) and diesel will continue to play a critical role throughout this decade, the truck production forecast for North America through 2031 indicates a significant increase in the production share of lower emissions and environmentally friendly alternatives like battery electric trucks. This trend is shaped by a number of factors, including technical advancement as well as California's Advanced Clean Trucks rule, which requires truck OEMs to sell more zero-emission trucks. Likewise, Canada's incentive and subsidy program for zero-emission vehicles will drive significant demand for ZEVs in the midterm.

Moreover, the impending shifts in powertrain technologies underscore a broader truck industry trend toward sustainability. Stringent rules and OEM commitments to zero emissions will shape the transition to battery electric and other alternative fuel vehicles. However, high total ownership costs, infrastructural deficiencies, and unpredictability in battery supplies could slow the adoption rate and lead to different timings across different parts of the region.

Economic, regulatory, and technological forces converge to shape the future of North America's MHCV market in the middle of the decade. With the looming EPA27 emissions standards ahead in the United States and further regulatory milestones beyond that, truck OEMs must balance between immediate opportunities and long-term investments to ensure efficiency and sustainability heading into 2027 and beyond.

This article is part of a series featuring highlights from S&P Global Mobility's 2024 Solutions Webinar Series. The North America Medium and Heavy Commercial Vehicle Outlook webinar occurred on May 16, 2024.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.