Discover more about S&P Global's offerings

Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Jan 17, 2024

2024 Automotive Materials Forecast: EV batteries...and more

Entering 2024, automotive sector health shows mixed messaging, fractured markets, and significant implosive forces affecting major megatrends. For all four CASE systems (Connected, Automated, Shared, and Electrified), 2023 showed cracks in the expansion rates and long-term outlooks of these development focus areas. But where does battery raw materials acquisition by OEMs and suppliers fit into the picture?

As market level indicators such as interest rates, loan to value, loan delinquency, and return to market all show headwinds - OEM messaging has changed from confident expansion toward one of value proposition. Suppliers with excessive debt coming to term will need to rebalance their near-term strategy toward making payments on increased interest rates instead of long-term investments.

Underpinning all OEMs and Tier 1 suppliers are material supply chains that directly determine which efforts will succeed by changing the economic feasibility, market reach, and technical prowess of their investments.

EV Battery Raw Materials

For example, Rare Earth Elements underpin the magnets in many electrical motors, improve the material characteristics of legacy materials, and enable ubiquitous technology such as touch sensitive displays. This one category of minerals development feeds many of the advanced technology packages seen as luxurious or even simply competitive by consumers.

But also under scrutiny is a relatively mundane mineral: copper. The mining of copper is currently underinvested and pivotal within energy transition efforts, but we're already seeing tier 1 suppliers and OEMs looking to replace this material in electrified vehicles. Battery bus bars and charging cables are moving toward aluminum in a cycle long known to the infrastructure-based use cases. In those applications, a 4:1 price ratio will drive material changes to infrastructure builds, and vehicle-based applications may see a similar tipping point. Teardown services are identifying improvements in assembly and cost which come from this material change.

The materials supply chain currently stands as the second major blockade to mainstream battery electric vehicle adoption rates. The mining sector faces a struggle to convince a widening ethical investor base of its ESG credentials.

Investments and crossing the chasm

Due to some investors holding back commitment to the mining sector it has not yet garnered the investment required in mineral exploration and extraction to support a mainstream transition to electric vehicles. For every voice proclaiming the future of automotive to be electric, there remains a chasm in investment which bolsters the validity of Main Street hesitancy toward EV adoption. While industry experts, business leaders and marketers all point toward battery electric vehicles, mainstream consumers have yet to find the problem that electric vehicles solve in their daily lives.

The timidity of institutional investors may come from the realities of EV adoption rates in the market - especially in North America. Or it may point to the difficulties in getting raw material markets to move forward - a task that takes decades of approvals and remains highly sensitive to market demand.

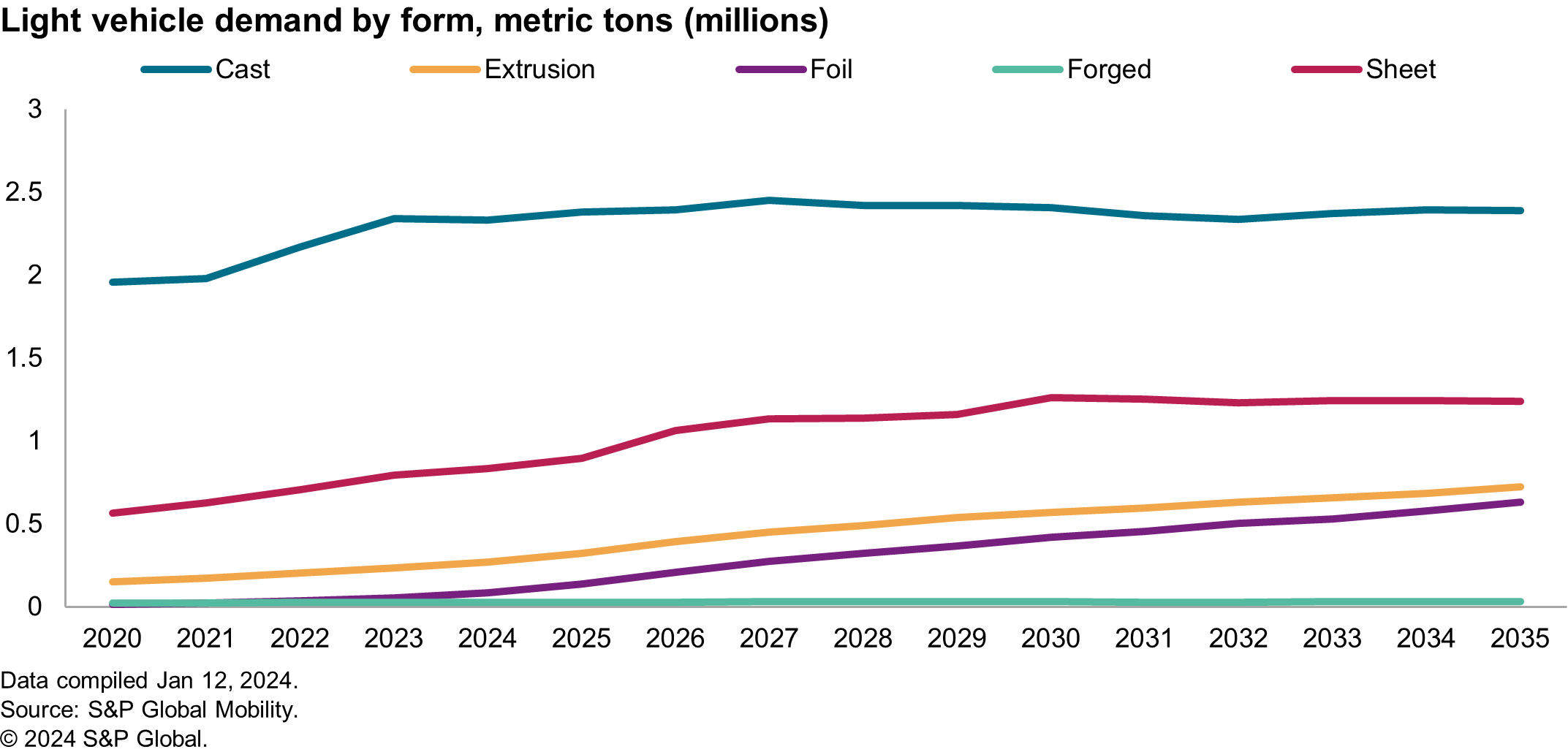

For instance, the chart below shows North American demand for aluminum - a standard ingredient for the battery to live on, but also a supply pinch point. Propulsion demand across multiple components shifts from the lower value castings of traditional systems towards extrusions, high-quality castings, and even foil sheets. All these forms require aluminum with fewer impurities, which influences scrap costs and may require dilution with additional primary aluminum.

In 2023, the Platt's Aluminum Symposium noted that high-quality sources of aluminum recycling such as beverage cans would not be able to bridge the demand gaps for North America, and the latest trade deficit numbers reflect the accuracy of this prediction.

In primary markets there are still significant hurdles to overcome in popularizing the re-processing of bauxite residue, also known as red mud, and other mining waste to provide additional market value with improved environmental impact. Low profit margins, long duration payback, high planning risk, and high sensitivity to operational excellence may be why investors have not supported the minerals extraction market as much as may be required. But it could also be baking in consumer-adoption headwinds. Research conducted by S&P Global Mobility in in 2023 found expressed interest in refining tailings to extract high value minerals while improving environmental <span/>stewardship, but voiced the difficulty in finding investors.

Country Risk Assessment

In the last few years, several supply chain disruptions to major material sources have fundamentally changed the way OEMs evaluate the risk of accepting a new material within vehicles. And sometimes the causes of supply chain snarls are unusual. As an example, preparations for the winter Olympics in Beijing, mainland China resulted in shortages in Magnesium (due to power plants being forced to close around the event to comply with tougher clean air rules which caused a reduction in smelting capacity). This illustrated how the reliance on a single city for 80% of the global supply of a commodity could result in shortfalls - causing suppliers to frantically hunt for recycled materials.

Regional sourcing of materials such as Nickel, Manganese and Cobalt have become more sensitized within OEMs. Some companies have signed <span/>ESG declarations regarding the origin of their material sourcing, to avoid the brand-damaging effects of societal risks associated with certain regions of production. Best-in-class materials may be replaced by "best in risk aversion."

Despite the sometimes cumbersome decision-making processes at OEMs, alignment of cost and risk reduction can move quickly. With the recent graphite shortfall of the battery industry, supply chain localization efforts are looking further into the raw material sourcing strategies to ensure risk is minimized.

ESG and Sustainability

For most people in business, "sustainability" usually concerns the longevity of financials, product performance, and the reduction of waste within systems. Messaging around sustainability has, in some circles, become equivalent to carbon accounting.

Performance of materials in real-world conditions will be contrasted with marketing messages and idealistic scenarios. For engineers being asked to improve recycled material content in components, reduce carbon footprint, or integrate biomaterials into their components, the task is typically associated with cost neutrality. But with the current macroeconomic conditions, automotive product portfolios, and changing optics of high-level initiatives, sustainability may evolve toward its initial definition of overall environmental responsibility.

OEMs in Europe are currently working to meet recycled material content regulatory requirements prior to formal approval. However, there are major problems with the incumbent regulations from the perspective of OEMs and material suppliers.

The EU mandate of recycled content is not a fine-based system, but rather a compliance-based metric which will determine whether a vehicle can be sold in the region. In cases of fine-based systems, OEMs can tolerate a blended changeover plan whereby they may inch toward compliance within a regulatory framework while accepting the increased cost of doing business in the short term. However, in this case, any vehicle with less than 25% recycled plastic will not be permitted for sale in the EU market.

Component engineers are looking to their suppliers for recycled content which can be quickly integrated into existing vehicles - and this is a main friction point in the materials industry. Chemical companies have existing recycled content compounds available for commercial use, but they have not made it through validation processes.

It's possible the OEMs have not allocated enough budget for these extensive and costly recertification processes, based on S&P Global Mobility research within the supply base. One component redesign researched was in the budget range of $50-80 Million, and these activities have slowed due to budgets being reallocated to battery system development, according to the supplier. Additionally, S&P Global Mobility has learned that these material suppliers are highly reluctant to invest in new processing systems that allow for integration of post-consumer waste into the feedstock. Although it is a state-of-the-art process, many of these publicly-traded suppliers are risking profitability in the process.

Fully loaded or decontented?

While materials can be a geopolitical and regulatory risk, there are unsung benefits of proper material selection when evaluated from a bottom-up perspective.

Some groups view material selection as infrastructure: If it works, a company will only invest the amount needed to keep the wheels rolling. For others, material selection is the tip of the innovation spear affecting customers directly. Use cases of vehicles are the ultimate group of demographics, intersectionality, and practicality.

Automakers make big investments in tactile surfaces, but decontenting a vehicle with the removal of items such as carpet, or using cloth or exposed non-woven surfaces, may produce a vehicle that gives the impression of rugged luxury. For another consumer, seeing a vehicle with an eco-conscious pledge of zero landfill waste, biopolymer use, or metrics reflecting the amount of recycled content, may align with their core values and emotional sentiment of why they purchase the vehicle.

Materials priorities in the supply chain

So, are materials considered as infrastructure or innovation? Both definitions are correct. Raw materials support the systems groups formally labeled as infrastructure, possibly putting minerals as the grandparents to these systems.

OEMs have attempted to secure the expansion portfolios in lithium, foreseeing an undersupply of this mineral in comparison with their product plans. However, this is not the only at-risk material for OEMs, as geopolitical, compliance, and market sentiment are dictating different terms. OEMs need to bring raw material supply chains back toward assembly plants, improve the material's internal visibility, and keep inflationary pricing in check.

The automotive industry is no stranger to complex systems, logistical sensitivities, or even vertical integration. Many of the stated goals for OEMs are currently competing for budget, talent, and marketing attention.

2024 may show the priorities of OEMs in a competitive goals environment, whereby single-metric grading scales are no longer appropriate methods of gauging their market performance. Some stretch goals of corporate performance may focus on core value propositions, consumer needs, and profitability. Strong business cases that embrace grit, efficiency gains, and waste reduction are expected to be winning topics.

FOR MORE ON MATERIALS AND LIGHTWEIGHTING

FEATURES AND TECHNOLOGY BENCHMARKING

THE LOOMING EV SUPPLIER SHAKEOUT

AUTOMOTIVE PLANNING AND FORECASTING

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2f2024-automotive-materials-forecast-ev-batteriesand-more.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2f2024-automotive-materials-forecast-ev-batteriesand-more.html&text=2024+Automotive+Materials+Forecast%3a+EV+batteries...and+more+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2f2024-automotive-materials-forecast-ev-batteriesand-more.html","enabled":true},{"name":"email","url":"?subject=2024 Automotive Materials Forecast: EV batteries...and more | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2f2024-automotive-materials-forecast-ev-batteriesand-more.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=2024+Automotive+Materials+Forecast%3a+EV+batteries...and+more+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2f2024-automotive-materials-forecast-ev-batteriesand-more.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}