Discover more about S&P Global's offerings

Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Jul 05, 2023

Commercial Vehicle forecast: MDHD truck market coasts through ’24, then accelerates as new emissions standards loom

FOR THE COMPLETE MEDIUM- AND HEAVY-COMMERCIAL VEHICLE INDUSTRY FORECAST

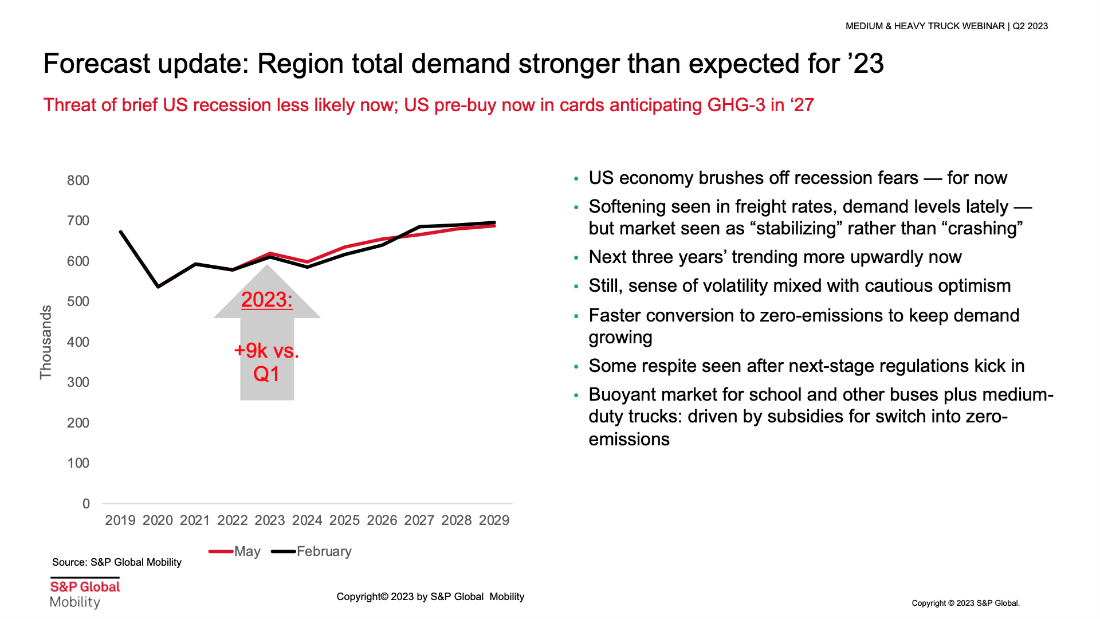

Demand is softening while production sustains in 2023, slowing into '24 - whereupon both rebound in the build-up to the GHG-3 pre-buy wave.

Post-pandemic market corrections will flatten North American demand and growth of Class 5-8 commercial vehicles and buses in the near term. Electrification will drive accelerating growth as next tier of regulations arrives in 2027.

The <span/>US economy appears to have skirted the short recession in 2023, thanks to stoic consumer spending in durable and nominal goods, coupled with the resurgence in services, travel, and restaurants - which have buoyed freight and truck activity though still being constrained by supply chain issues after the Covid-19 pandemic. A slowing-down is expected to be visible by the fourth quarter, turning into a soft-growth 2024.

After a strong first half of 2023, there should be a moderate

reduction in medium- and heavy-duty commercial vehicle and bus

demand through 2024, according to the <span/>S&P Global Mobility's <span/>Q2 2023 forecast

update. However, the updated forecast maintains a more positive

outlook for 2025 to 2026. when the truck market gears up for the

next level of emissions regulations. The third tier of the 2027

greenhouse regulations, combined with the timing of the fleet

replacement cycle, will <span/>likely fuel a strong wave of pre-emptive

buying.

"The added cost of those tougher regulations will drive more purchase activity in the middle of the decade," said Antti Lindstrom, principal analyst for commercial vehicle forecasting at S&P Global Mobility. Furthermore, in the bus space, support measures from the public sector are driving the conversion of school buses and transit buses to zero-emission solutions, adding to this optimistic outlook.

CLICK HERE TO WATCH THIS AND OTHER WEBINARS

As momentum slows, demand is estimated to dip to a low of around

505,000 units in 2024 (including buses and motorhomes), with

projections indicating approximately 543,000 units by 2025. While

not the primary driver, the energy transition in the trucking

sector starting in California - plus about a dozen

other <span/>CARB states

with similar trajectories - is poised to support

volume growth in 2023 and after. In addition to expected

new-product updates, both established players and startup <span/>OEMs are continuing to

introduce "cleaner" versions of their existing truck models such as

the Freightliner eCascadia and Hino's XL8 series, not to mention

PACCAR's Kenworth and Peterbilt <span/>BEV models that comply with zero-emissions

standards.

There are several variations in observable market trends across

different vehicle classes:

- Class 4 trucks, which were popular until the beginning of 2022, have been increasingly taken as lighter-duty applications for last-mile distribution during the pandemic. Ford's Class 4 Econoline Cutaway model accounts for <span/>nearly two-thirds of models in this segment and may see increased competition rising from the start-ups entering the fray.

- Class 5 vehicles, while facing supply chain issues, are expected to see an increase in demand following a post-pandemic pause - for example in public-sector buying.

- Class 6 trucks have gained attention due to their fuel efficiency and suitability for many commercial purposes. However, softening of the housing and construction market triggered a dip in Class 6 truck registrations.

- Class 7 trucks have been on a decline in popularity due to their licensing requirements and higher costs vs. Class 6, in addition to the recent preference of OEMs and customers for trucks that bracket this segment.

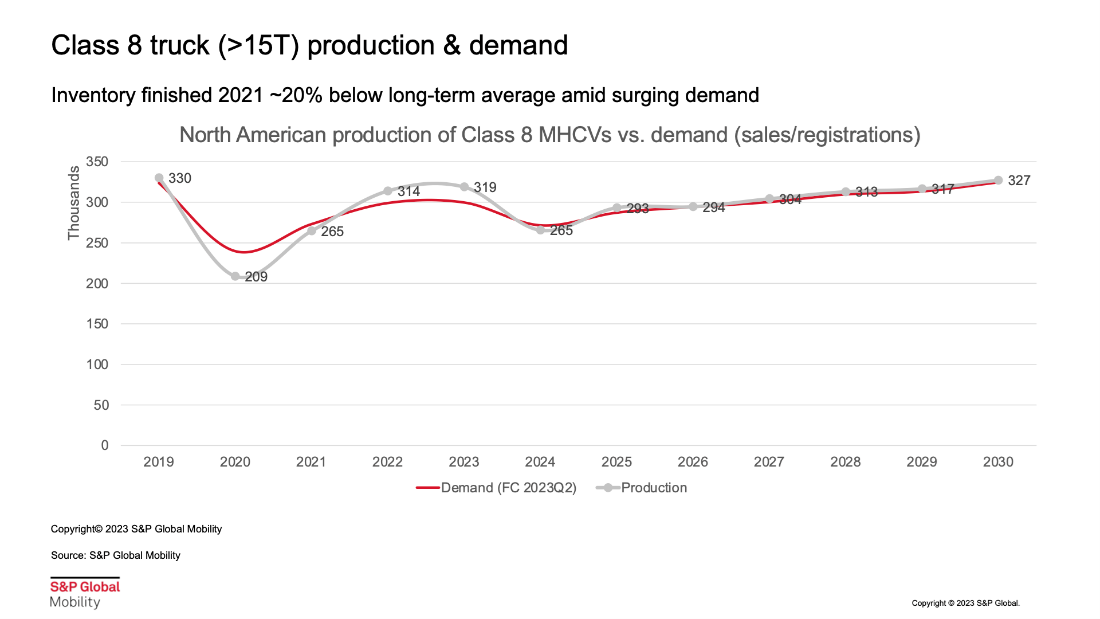

- After a stronger 2022 where OEMs continued to focus on Class 8 trucks amid supply chain bottlenecks, we expect tractor-truck registrations to remain flat this year before a dip in 2024, and a modest upward trajectory picks up again starting in 2025.

- Not yet recovered to pre-pandemic levels, bus and motor home demand is projected to climb significantly in the current year and remaining at a similar level in 2024, supported by a rebound in school bus purchases. Growth is to resume in 2025, with motor homes and other bus types expected to provide the additional lift then.

Regardless of weight class, the more stringent environmental

compliance will be the key driver in demand and production of all

vehicle types. Upcoming regulations, specifically the proposed

greenhouse gas emissions standards by the Environmental Protection

Agency are forcing traditional OEMs to re-evaluate their

manufacturing and investment strategies and prompting a potentially

rapid shift from internal combustion engine (ICE) products to

electrified vehicles.

These laws, in conjunction with the continued push for more aggressive decarbonization efforts by states like California with its Advanced Clean Fleet regulation, are acting as the key catalyst in the transformation of powertrain technologies. However, the transition to the adoption of hydrogen and fuel cell technologies remains limited by cost, infrastructure, and availability issues. This suggests battery-powered electrification as the go-to strategy will be pushed further into the midterm until those issues can be resolved - notwithstanding the recharging network for BEV trucks, which remains to be built.

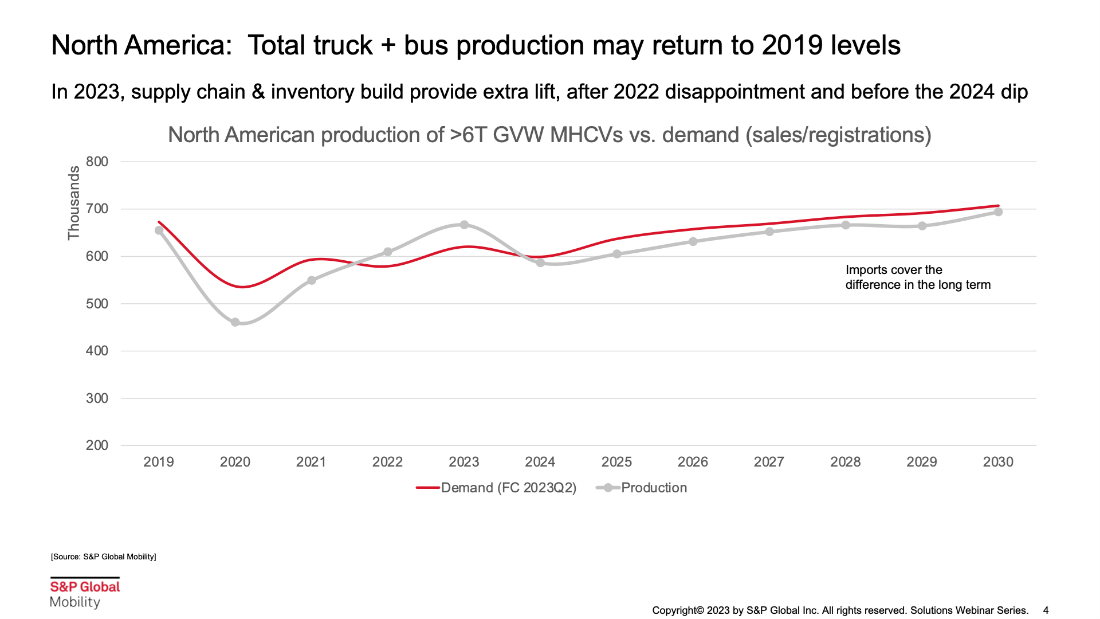

Disruptor brands like Tesla and Nikola will accelerate this transition for their part and help strengthen the US as the region's epicenter of production. As for the legacy brands, despite supply chain and labor issues, their Class 4-8 production rates for the North America region reached and even slightly exceeded the average build rates of 2019 by the end of 2022. While some production targets are still not being achieved, inventories continue being rebuilt - setting the stage for potential growth later.

"Inventory figures of Class 4-7 trucks - which represent about half the market - remain below long-term averages, which is one reason why we think production has some upward potential," said Andrej Divis, executive director of global truck research at S&P Global Mobility.

Overall, present demand is still strong, owing to the muted risk of recession compared to the previous two quarters, combined with surprisingly resilient consumer activity. Production is expected to sustain its surge in the short term, while remaining constrained by supply chain and labor issues, before levelling off and even declining in 2024.

SUPPLY SHORTAGES AND NEW EVS AFFECT '22 CV REGISTRATIONS

FOR THE COMPLETE MEDIUM- AND HEAVY-COMMERCIAL VEHICLE INDUSTRY FORECAST

HYDROGEN: IN IT FOR THE LONG HAUL

TO WATCH THIS AND OTHER WEBINARS

CAN BRAZIL'S COMMERCIAL TRUCK FLEET TURN ELECTRIC?

COMMERCIAL VEHICLE INSIGHTS AND INTELLIGENCE

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2fcommercial-vehicle-forecast-mdhd-truck-market-coasts.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2fcommercial-vehicle-forecast-mdhd-truck-market-coasts.html&text=Commercial+Vehicle+forecast%3a+MDHD+truck+market+coasts+through+%e2%80%9924%2c+then+accelerates+as+new+emissions+standards+loom+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2fcommercial-vehicle-forecast-mdhd-truck-market-coasts.html","enabled":true},{"name":"email","url":"?subject=Commercial Vehicle forecast: MDHD truck market coasts through ’24, then accelerates as new emissions standards loom | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2fcommercial-vehicle-forecast-mdhd-truck-market-coasts.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Commercial+Vehicle+forecast%3a+MDHD+truck+market+coasts+through+%e2%80%9924%2c+then+accelerates+as+new+emissions+standards+loom+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2fcommercial-vehicle-forecast-mdhd-truck-market-coasts.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}