Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

Fuel for Thought: Electrification in China — On Track but Challenging

Listen to this Fuel for Thought podcast.

Mainland China's transition to electrification reached a major milestone in July 2024 when sales of new-energy vehicles (NEVs) surpassed internal combustion engine (ICE) vehicles for the first time, according to data released by the China Passenger Car Association (CPCA).

NEVs include battery electric vehicles (BEVs), plug-in hybrid vehicles (PHEVs) and range-extended electric vehicles (REEVs). In 2023, automakers' aggressive sales promotions and a tidal wave of new model launches helped to boost sales of NEVs in mainland China after the 2022 withdrawal of the central-government subsidy programs.

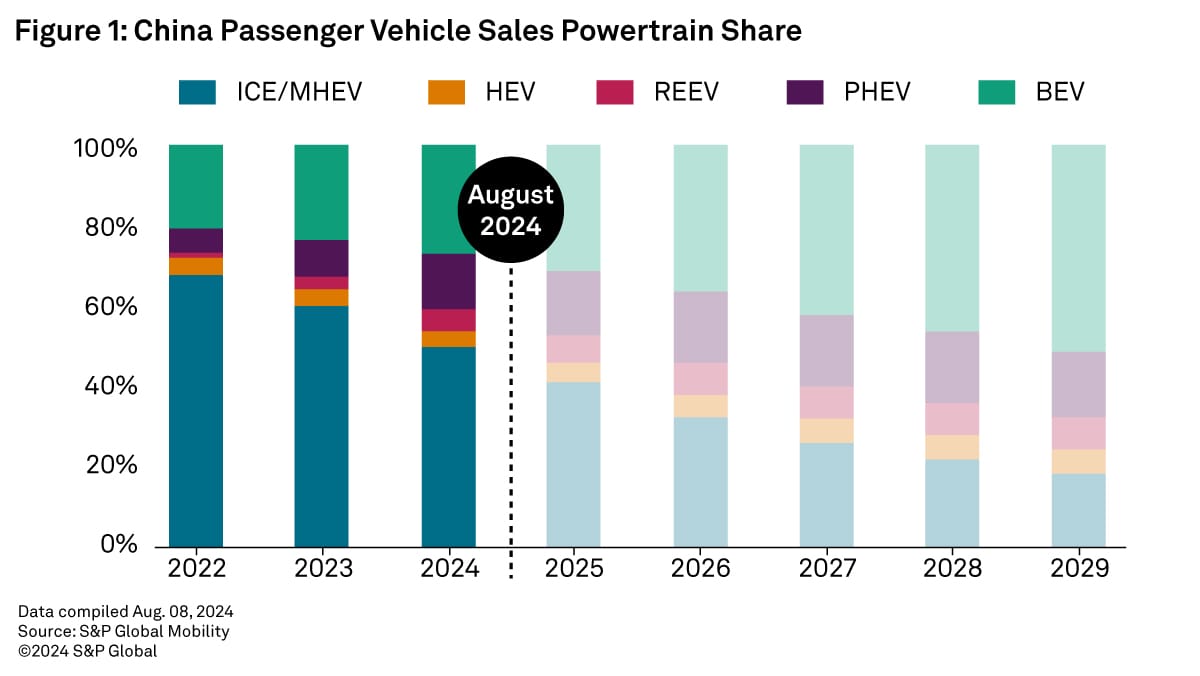

It is beyond doubt that the Chinese auto market will continue to transition to electric vehicles in the next few years with automakers advancing their electrification plans. S&P Global Mobility expects that NEV share of the Chinese passenger vehicle market will reach 46% in 2024, compared to 36% in 2023.

The acceleration in the market's shift to EVs will be helped by declining battery prices, a wider availability of models and the intense level of competition that exists in the market.

With NEVs going mainstream, trends taking shape in the sector have begun to affect the broader passenger car market and influence consumer choices.

EV adoption increasingly driven by plug-in hybrid models with BEV sales slowing down

Although purchases of BEVs, PHEVs and REEVs are all eligible for the central-government's purchase tax reduction incentive programs through 2027, what is really accelerating the market's shift to electrification in 2024 are PHEVs and REEVs, rather than pure electric vehicles.

In the first half of 2024, Chinese sales of BEVs rose by 12% year over year to 3.02 million units, by comparison, sales of PHEVs, including vehicles with extended-range electric powertrain, surged by 85% year over year to 1.92 million units in the first half of this year.

These market dynamics were already taking shape in 2023. S&P Global Mobility research shows that combined sales volumes of PHEVs and REEVs in the passenger vehicle market surged by 83% year over year in 2023 to 2.75 million units, while that of BEVs grew by 20% to 5.2 million units.

S&P Global Mobility expects PHEV and REEV sales in mainland China to continue to grow in the next few years, accounting for 24% of total passenger vehicle sales by 2029. Despite a slowdown in the annual growth rate, BEV sales share is expected to reach 51% in 2029. Together, the total NEV sales share would be 75% that year, according to S&P Global Mobility forecasts.

Growing presence of Chinese automakers poses a challenge for global companies

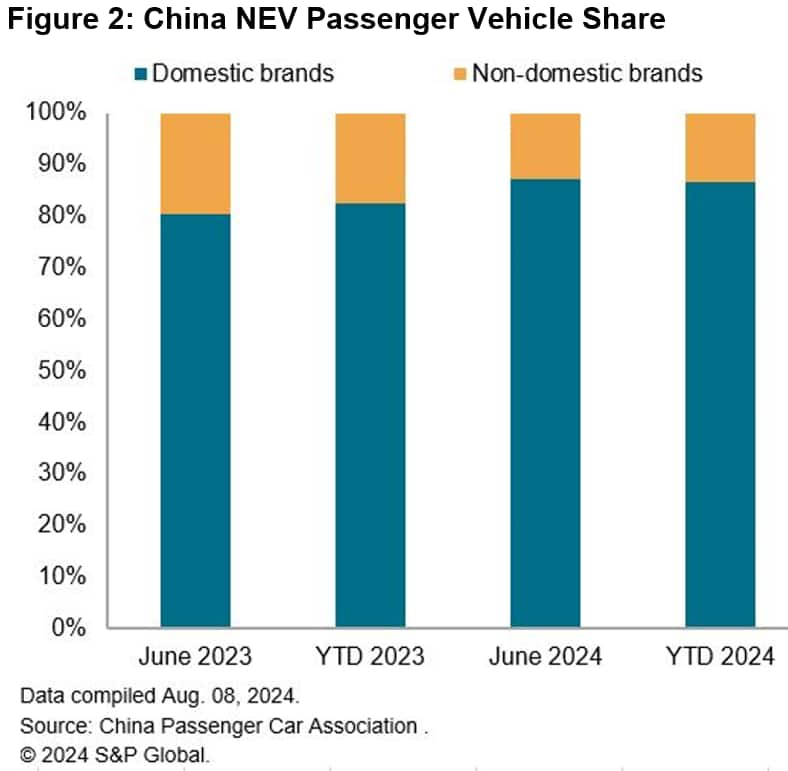

Chinese brands' strong presence in the NEV market has helped them to advance their market share in the overall passenger vehicle market. Domestic brands' market share in the Chinese retail passenger NEV market increased from 83% in the first half of 2023 to 87% in the first half of 2024, while their global counterparts have a combined sales share of less than 15% in the first six months of 2024.

Chinese OEMs' growing presence in the NEV market has led to a shift in consumer preferences over brands and models. Global OEMs, especially the Japanese brands, have struggled to match their Chinese rivals in the speed of adapting to changing consumer demand and market conditions. Toyota has already cut production at its Chinese JVs by 22% year over year in the first half of 2024 to cope with declining demand. Nissan and Honda, the other two major Japanese automakers in mainland China, have all recorded huge declines in Chinese sales during 2024, faced with BYD's aggressive product offensive.

In addition, the premium automakers, including the big 3 German brands, also face the challenge of commanding a price premium for their new-generation BEVs as price competition intensifies. To keep up with the speed of innovation in China and reduce development costs, VW is working with Xpeng and SAIC Motor on separate EV programs that will use the two Chinese companies' vehicle platforms and software technologies. VW's upcoming new launches in mainland China will also include long-range PHEVs and REEVs developed jointly with SAIC.

S&P Global Mobility's latest projection shows Chinese brands' sales share in the country's passenger NEV market is set to reach 87% in 2024, further improving from 83% in 2023. With global automakers rolling out their new-generation BEVs and PHEVs in mainland China in the next few years, we expect global brands' market share to improve from 2026 onwards to reach 25% in 2029 with VW and BMW contributing strongly.

Chinese tech companies tapping into consumer preferences for SDVs

Software is increasingly a point of difference in influencing buying choice in mainland China. Growing consumer interest in software-defined vehicles (SDVs) presents an opportunity for mainland China's tech companies to tap into the electric vehicle market.

Xiaomi Corporation, a leading smart phone manufacturer, aims to deliver 100,000 EVs this year. The company's first electric model, the SU7 sedan, has received unprecedented publicity in mainland China thanks to Xiaomi's strong brand appeal, its huge consumer electronics products userbase and new smart car features it introduced to the SU7.

China's telecom giant Huawei also emerged as a major player in the NEV sector, providing a range of intelligent vehicle technologies to its OEM partners. The success of AITO, a Huawei-backed NEV brand, has encouraged China's state-backed automakers including BAIC and JAC to forge partnerships with Huawei to transition their product line with software-defined cars.

China's export surge met with new trade barriers

Although electrification in mainland China continues to grow, the country's status as an EV production and export hub may face some challenges.

Mainland China's EV exports surged in the past two years amid automakers' efforts to expand sales in global markets. Data from the China Association of Automobile Manufacturers (CAAM) suggests China's NEV exports reached 1.2 million units in 2023, compared with less than 680,000 units in 2022.

Although Tesla contributed largely to mainland China's EV export surge in recent years, growing EV shipment volumes of Chinese automakers including SAIC and BYD has fueled concerns over China's overcapacities and its intention to dominate the global market with low-price vehicles.

The EU's provisional tariffs, which adds up to 36.3% of custom duties to Chinese-built BEVs, are the latest example of rising protectionist actions taken by major economies to protect their market from the influx of BEVs originating in China. Canada and the US have also announced strict tariffs on China-made BEVs. Automakers are looking to cope with these trade barriers by shifting production of certain models to other manufacturing locations or investing in local production capacities to circumvent tariffs. The high tariffs will also prompt automakers to further optimize their cost structure to maintain a reasonable margin level.

However, within the automotive sector, major global automakers including Stellantis and Volkswagen are seeking their own way to keep up with competition from Chinese rivals. Both automakers have invested in Chinese EV startups in the past year to gain access to EV know-hows—especially software architecture—and speed up new launches. The Stellantis and Leapmotor joint venture already began shipment of Leapmotor EVs built in mainland China to Europe in July.

To cope with the EU tariffs, Stellantis also kicked off assembly of the Leapmotor T03 EV at its plant in Poland from semi-knocked-down kits imported from mainland China.

S&P Global Mobility offers detailed sales-based

powertrain forecasts for the United States, Canada, Brazil, United

Kingdom, Italy, Germany, France, Spain, Netherlands, Sweden,

Norway, Rest of EU30, India, mainland China, and Australia.

Learn more about the powertrain forecast.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.