Discover more about S&P Global's offerings

Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Jul 31, 2023

Mainland Chinese consumers crossing the chasm to mainstream EV adoption

With Battery Electric Vehicles (BEV) and Plug-In Hybrid Electric Vehicles (PHEV) now entering the market in the mid-$20,000 range, disruptor brands are going all-in on New Energy Vehicles (NEV). S&P Global Mobility forecasts significant market growth of electrified-vehicle sales in mainland China by 2030, with two-thirds of them being pure battery-electric. And NEV exports are sharply on the rise.

Whereas government policy and subsidies have been the driving force in the development of the market for electrified vehicles in mainland China, organic consumer demand is beginning to play a role as well. And while outright purchase subsidies are disappearing, tax incentives and providing free or subsidized license plates to BEV owners in some cities will also continue to support market growth.

Such incentives notwithstanding, battery price has been a barrier to growing consumer demand for electric vehicles due to its impact on the overall vehicle price. The price of raw materials used in EV batteries spiked in mid-2022 and has been volatile. That led automakers to utilize plug-in hybrid technology - which has smaller battery capacities installed than battery-electric vehicles - to keep costs down while also offering relatively good fuel efficiency.

In contrast to Japanese brands that have dominated the full-hybrid (non-plug-in) market with the Honda IMMD and Toyota THS, mainland Chinese domestic brands have now come to the fore, achieving robust growth of the hybrid market share with their advanced dedicated plug-in-hybrid technology.

As there is no NEV incentive for Parallel Full-Hybrids (FHEV), Japanese brands are struggling to compete with PHEVs from Chinese OEMs. Compared with HEVs, PHEVs have a better performance in fuel consumption, a longer electric range, and - for a long-term carbon-free individual mobility strategy - it helps as a bridging technology. To wit, see BYD's success in developing PHEVs, due in part to positive stimulus from the Chinese government with the purchase tax reduction policies extended to CY2027. Chinese OEMs like Great Wall, Geely, Changan, GAC, and Chery also are reinforcing their PHEV products with dedicated hybrid propulsion technology developed to work as an important solution for NEV strategy by 2030.

For the medium term, PHEV technology is expected to be a bridging solution for BEVs, while BEVs remain mostly expensive and charging options are limited to certain consumers, or specific areas.

The long-term trend, however, is in battery-electric vehicles. And while established automakers have taken a more gradual approach to introducing BEVs, new entrants have focused mainly on battery-electric technology.

There are positive developments supporting lower prices in both the BEV and PHEV segments. Consumer demand has grown resulting from a continuous improvement in battery density - which allows either an improved range or a lower entry price for vehicles with a shorter range. Concurrently, charging infrastructure development is expanding, as well.

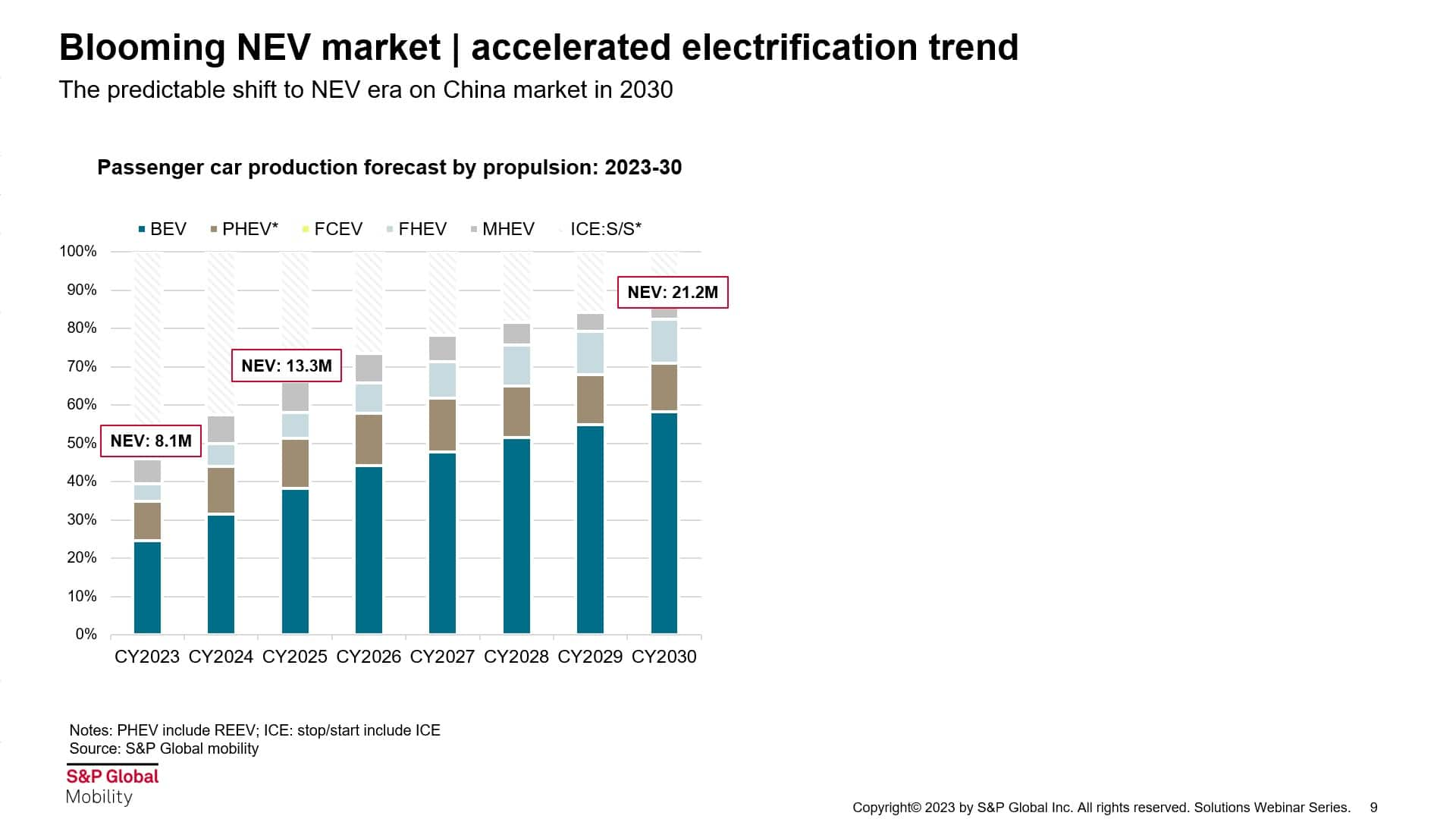

S&P Global Mobility forecasts NEV passenger car production in mainland China in 2023 to be 8.1 million units, nearly tripling to 21.2 million annual units by 2030. Of that number, 58 percent of the overall mainland China passenger vehicle production in 2030 is expected to be BEVs, an increase from around 25 percent in 2023. (Note: S&P Global Mobility defines New Energy Vehicles as battery electric, plug-in hybrid electric, range-extended electric vehicles, and fuel cell vehicles.)

That said, S&P Global Mobility is still recommending the implementation of various electrification technologies that address different scenarios and user demands. Doing so could result in huge incremental gains for the future development of the NEV market.

Examining the market penetration of Tesla and BYD illustrates the advantage of having a diverse product portfolio in mainland China. Tesla's battery-electric vehicles are concentrated in Tier One and Tier Two cities. But BYD - a domestic automaker with a much broader product portfolio of both battery electric and plug-in hybrid electric vehicles in a wider price range - has a more balanced distribution across all tier cities.

Models in the 100,000 to 200,000 yuan price range (around US$14,000 to $28,000) are most popular in the BEV and PHEV markets right now. BYD dominates the PHEV market and has a significant market presence in the BEV segment. Its models are concentrated in the B-, C- and D-segments.

Meanwhile, Tesla, which resorted to price cutting to gain market share, has significant BEV sales primarily in the D-segment. There is, however, fierce competition in the middle of the BEV market. The premium segment, already well populated with both gas and electrified engines, offers more opportunities for the introduction of electric vehicles with intelligent features such as ADAS and intelligent cockpits.

By 2030, we forecast 11% of BEV passenger cars will be equipped with battery capacity equaling or exceeding 100 kWh.

Looking at the technological aspect of the electric vehicle industry, China has a strong advantage in three key areas. It has a complete and competitive supply chain in rare earth materials and positive/negative electrode materials. It also has leading battery manufacturing companies with technological expertise. That will allow for significant increases in battery capacity.

With the manufacturing of electrified vehicles booming, the export of NEVs from mainland China could also be a potential growth industry. In 2022 about 10% of mainland China-produced NEVs were exported to other sales countries.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2fmainland-chinese-consumers-crossing-the-chasm-to-mainstream-ev.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2fmainland-chinese-consumers-crossing-the-chasm-to-mainstream-ev.html&text=Mainland+Chinese+consumers+crossing+the+chasm+to+mainstream+EV+adoption+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2fmainland-chinese-consumers-crossing-the-chasm-to-mainstream-ev.html","enabled":true},{"name":"email","url":"?subject=Mainland Chinese consumers crossing the chasm to mainstream EV adoption | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2fmainland-chinese-consumers-crossing-the-chasm-to-mainstream-ev.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=Mainland+Chinese+consumers+crossing+the+chasm+to+mainstream+EV+adoption+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2fmainland-chinese-consumers-crossing-the-chasm-to-mainstream-ev.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}