Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

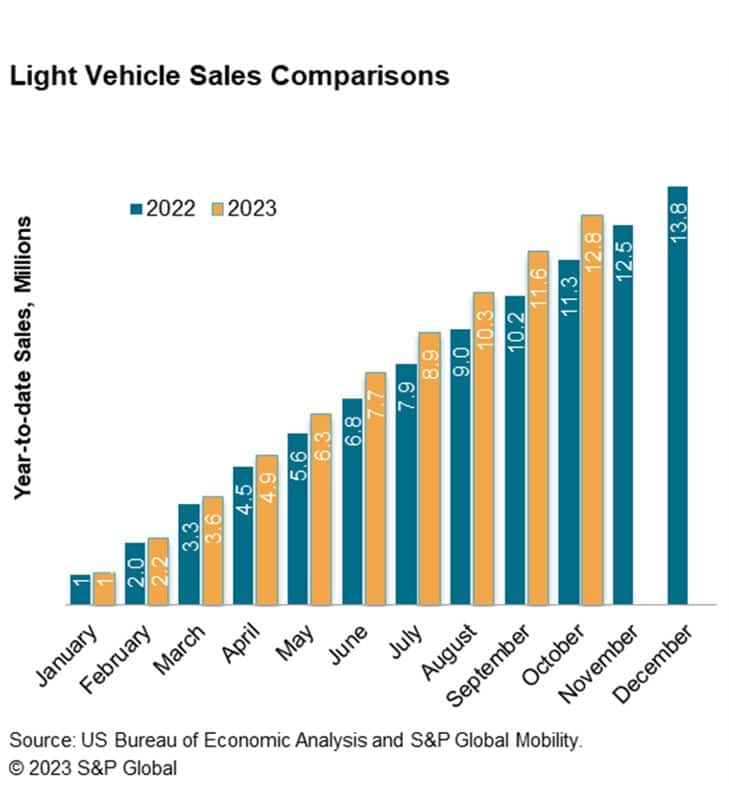

October US auto sales reflect uneasiness and volatility; projection of 1.2 million units

Despite some assembly plants shut down by the UAW strike for more than a month and continued auto consumers pressure points of rising interest rates and still-high new vehicle pricing levels, October US light vehicle sales are expected to be relatively optimistic. S&P Global Mobility projects sales volume of 1.22 million units for the month, which would translate to a seasonally adjusted selling rate (SAAR) of 15.7 million units for the month, in line with the month-prior level.

The sales outlook for the remainder of the 2023 remains uncertain given the UAW strike against GM, Ford and Stellantis. While sales impacts for September were limited, the production disruptions and consequent sales effects caused by the strike are expected to emerge in October sales levels for these specific automakers - and are very likely to be sustained in November. Further impact will be determined by the length and expansion of shutdowns beyond the current plants.

"On the surface, with a projected SAAR result of 15.7 million units, October auto sales will be stronger than they appear," reports Chris Hopson, principal analyst at S&P Global Mobility. "Underlying pressure by way of still-notable vehicle affordability concerns, potential economic slowdown and specific instances of severely limited inventory levels are likely to be a drag on auto sales for the remainder of the year."

According to the S&P Global Mobility analysis, as of the week ending October 22, 2023, approximately 150,000 units of production have been lost due to the respective plant strikes. Inventory levels, which will continue to be a closely followed metric as long as the UAW strike persists, will be pressured moving through November and into December.

This production loss is reflected in retail vehicle inventory listings which have decreased by 12% for the models affected by the strikes. However, this decrease has been more than offset by increases in other models, leading to potential market share volatility in the upcoming months.

The overall industry advertised inventory has sharply accelerated in the past month: from 2 million units as of Sept 11, to nearly 2.5 million units for the week ending Oct. 15 - more than a 10% increase in a one-month span, and 64% higher than this period last year.

"Model year 2024 advertised inventory is now reaching the level of remaining 2023 model year units," said Matt Trommer, associate director of Market Reporting at S&P Global Mobility. "And while we see the 2023 model year inventories decreasing, the 2024 MY inventory is growing at a faster rate than the 2023 model year sell-down."

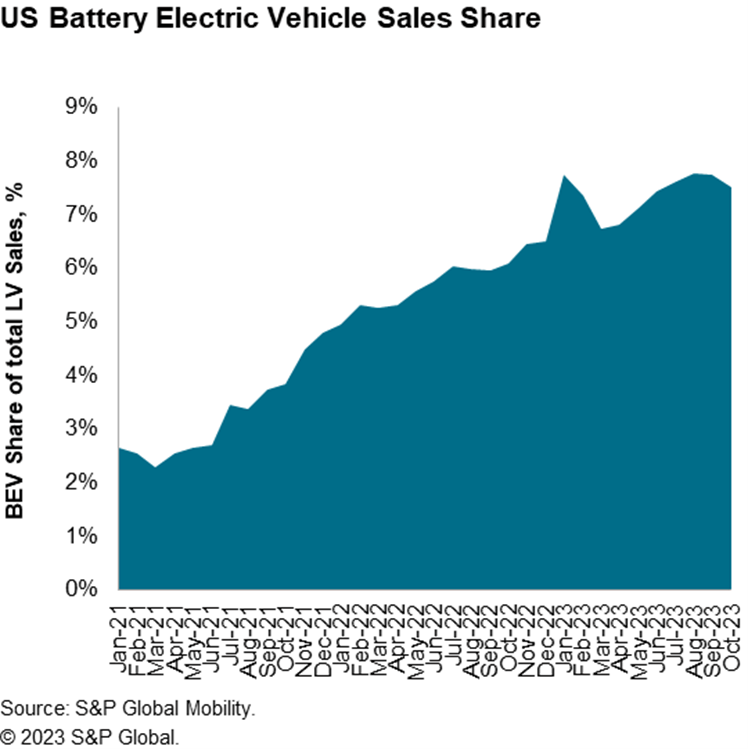

Continued development of battery-electric vehicle (BEV) sales remains a constant assumption for 2023 although some month-to-month volatility is expected. October 2023 BEV share is expected to reach 7.5% and bringing year-to-date BEV sales growth to an estimated 47%. Looking at the remainder of the year, beyond potential future pricing developments by Tesla, the launch of several new BEVs is expected to produce incremental sales gains as the year comes to a close.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.