Discover more about S&P Global's offerings

Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Dec 20, 2023

2024 EV forecast: the supply chain, charging network, and battery materials market

For the electric vehicle sector, 2023 saw waning consumer preferences for EVs, several promising startups fall by the wayside, a decline in battery materials costs, and ambitious OEMs and suppliers from mainland China turning their focus to exports of vehicles as well as components. S&P Global Mobility's forecast for 2024 is one of cautious optimism - with an increase in affordable EVs, reliable vehicle-charging ecosystems, and profitable returns.

Despite the slowdown in consumer sentiment toward EVs, there is nonetheless an ongoing necessity for emissions reductions - with EV regulations and milestones largely intact and looming a year closer. However, slowing consumer desire for existing EVs could boost profitable internal combustion engine (ICE) markets and legacy automaker portfolios, driving consolidation and attracting private equity interest.

Crucial strategic decisions regarding capital expenditures in the electrification space need to be made in the near term. Several OEMs are beyond the point of no return in their shift to EVs, while some suppliers might be questioning the wisdom of going "all in" on EVs quite so soon.

Much of the decision will be based on being able to deliver at scale affordable mass-market EVs with enhanced real-world range. These vehicles need to be integrated into charging ecosystems that are both abundant and reliable. While ensuring profitability and maintaining margins, these efforts are aimed at delivering returns for investors who are eagerly awaiting returns on their capital investments in the light passenger vehicle sector's contribution to the energy transition.

Here is our forecast breakout by various sectors within the electrification space:

Global EV sales

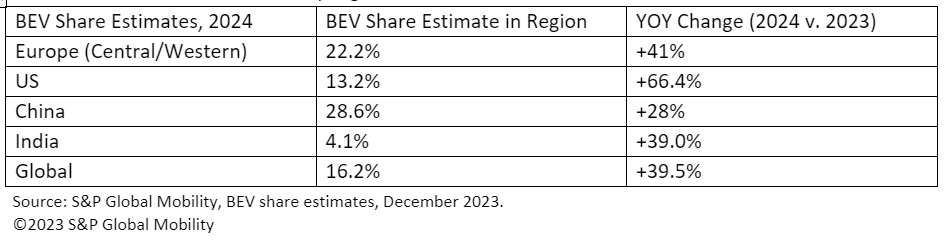

Despite slowing consumer demand for electric vehicles, reports of the demise of EVs have been greatly exaggerated. S&P Global Mobility's 2024 global sales forecast projects battery electric passenger vehicles to be on track to post 13.3 million units worldwide for 2024 - accounting for an estimated 16.2% of global passenger vehicle sales. For reference, 2023 posted an estimated 9.6 million BEVs, for 12% market share.

Major markets are forecast for most of this volume, though smaller markets will also see modest increases. Forecasted BEV share by region is as follows:

The EV supply chain

OEMs are shifting toward in-house development of electrified propulsion components, and the landscape of outsourced programs for components such as integrated e-Axles is exceptionally competitive.

Mainland China's control over the electric motor market and its required resources has led to growing technical and political efforts to diversify away from permanent magnet (PM) usage. Primary platforms, specifically secondary e-Axle applications in all-wheel drive, are transitioning away from PM.

Increased OEM-supplier partnerships signal attempts to control the electric motor market against mainland China's dominance. E-fuels' "free pass" in Europe offers an opportunity amid declining EV sentiment, prompting a shift of focus to research and development (R&D) and supply chain scaling.

Additionally, the increase in production volumes is expected to encourage more partnerships, alliances and joint ventures. This collaboration allows OEMs to have greater control over a critical propulsion value chain, which can present technical challenges and potential supply chain constraints.

Tesla Cybertruck and thermal efficiency

Tesla and mainland Chinese OEMs lead in integrating thermal components to create more efficient BEVs, and this trend should continue globally. Thermal management, with its increasing content per vehicle, could become a renewed focus for suppliers amid OEMs' in-house shift.

Several OEMs have already started exploring the consolidation of cooling circuits and integration of key system subcomponents such as pumps and valves. If the Cybertruck's innovative integrated thermal management (ITM) technologies are effectively implemented, it is likely that fast followers will emulate these advancements. Potential implications could be a shift from low-voltage components to 48V systems - affecting elements such as water pumps, cooling fans, reservoir chillers, and the HVAC blower.

Such developments capitalize on BEV platform clean sheet development freedoms to deliver more compact and efficient systems. We expect this trend to persist among European and North American OEMs, with many tier 1 suppliers continuing to develop and deliver their take on the integrated thermal module.

However, while the launch of the Tesla Cybertruck may influence near-term thermal management technologies, it may also prompt questions about the efficacy of the combined Octovalve and Super Manifold system in meeting performance needs in diverse operating conditions.

With a larger battery and more demanding operating conditions, there may be doubts about whether a complex and relatively small system like the Super Manifold can adequately perform cooling and heating duties. This could lead Tesla to reconsider their one-size-fits-all system strategy. One potential implication could be the necessity to incorporate electric heaters to manage the challenges posed by colder operating conditions.

Mainland China EV startups

What will be the outcome for mainland Chinese EV startups and tier 1 cell manufacturers in mainland China if domestic EV demand does not grow as anticipated? If new import tariffs in Europe are implemented, OEMs that assemble their export vehicles in mainland China might find margins diluted.

Furthermore, mainland Chinese companies are pursuing agreements with Korean and Moroccan counterparts, anticipating compliance with subsidy rules. Stringent IRA criteria, excluding batteries with minor contributions from mainland China, may restrict the eligibility of those EVs for the $7,500 credit. Additionally, potential loopholes, such as assembling in Free Trade Agreement-compliant countries, will likely be addressed and eliminated.

EV raw materials prices and battery cost dynamics

Stagnant metal prices in 2024 are likely to bolster vehicle margins, but the unexpected decline threatens mining projects' viability.

Lithium prices for batteries dropped more than 60%, and nickel, graphite, and cobalt each fell about 30% in 2023. Stagnant metal prices throughout 2024 will help reduce battery costs, thereby improving vehicle margins (or affordability if savings are passed on to consumers). However, the unexpected decline in lithium, cobalt, and other EV battery metal prices is impacting mining firms, prompting the suspension or delay of new projects.

EV charging incentivization and regulations

The number of AC and DC chargers installed globally surged from 3 million in 2019 to more than 10 million in 2022. The count will increase to more than 15 million globally in 2023, and we forecast 70 million in 2030. As charging availability remains a key issue for the widespread deployment of EVs, governments are one of the main actors to further the cause of easing the access to it.

For the US, the National Electric Vehicle Infrastructure Standards, or NEVI Formula Program, specifies where federally funded infrastructure must be placed. In Europe, the Regulation for the Deployment of Alternative Fuels Infrastructure sets minimum requirements to which EU member states must adhere, specifically regarding the number and specifications of publicly available EV infrastructure.

Observance of these and other such regulations globally will ensure sufficient deployment of infrastructure. However, open questions remain around interoperability across networks, ease of payment, transparency of expected charge times and plentiful access to fast charging.

EV charging and range technology

Wide bandgap (WBG) materials such as silicon carbide (SiC) and gallium nitride (GaN) are transforming power electronics, promising BEV drivers faster charging, extended range, and lower costs. They are seen as superior semiconductor technologies for high-voltage power devices and, consequently, an ability to sustain higher power for extended periods. WBG technology facilitates faster switching, leading to decreased power losses and more compact systems.

Europe's PFA ban

The EU's delayed decision on the per- and polyfluoroalkyl substances (PFAs) ban will hinder the automotive industry's development planning, despite ongoing alternative testing. The European Union's slow decision-making process and deadline setting for the ban on PFA usage and production remain on the 2024 agenda, but progress has been delayed. The lack of clarity on impending regulation is unhelpful to the automotive industry, particularly in terms of future development and certification planning. Although companies are already testing alternatives, a definitive trend has yet to emerge.

The long tail of ICE

All these potential stumbling blocks bring us full circle to existing internal combustion technology.

The "free pass" given to so-called e-fuels in European legislation regarding the ICE phase-out poses an opportunity should EV sentiment continue to decline. R&D efforts, as well as the expansion of the supply chain, will continue to explore the potential of this opportunity. These efforts are particularly relevant for those who deem EVs an imperfect solution for specific use cases.

If EV sales growth continues to decelerate, several major suppliers are strategically positioned to deliver key internal combustion components in a market sector that, despite its decline, potentially remains highly profitable and consolidated. In 2024, further consolidation is possible, with suitable candidates drawing the attention of keen private equity investors who have ample capital to invest.

FOR MORE ELECTRIC VEHICLE TRENDS

DEMO OUR VEHICLE TECHNICAL INTELLIGENCE PLATFORM

AUTOMOTIVE PLANNING AND FORECASTING

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2f2024-ev-forecast-the-supply-chain-charging-network-and-battery.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2f2024-ev-forecast-the-supply-chain-charging-network-and-battery.html&text=2024+EV+forecast%3a+the+supply+chain%2c+charging+network%2c+and+battery+materials+market+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2f2024-ev-forecast-the-supply-chain-charging-network-and-battery.html","enabled":true},{"name":"email","url":"?subject=2024 EV forecast: the supply chain, charging network, and battery materials market | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2f2024-ev-forecast-the-supply-chain-charging-network-and-battery.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=2024+EV+forecast%3a+the+supply+chain%2c+charging+network%2c+and+battery+materials+market+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2f2024-ev-forecast-the-supply-chain-charging-network-and-battery.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}