Discover more about S&P Global's offerings

Customer Logins

Obtain the data you need to make the most informed decisions by accessing our extensive portfolio of information, analytics, and expertise. Sign in to the product or service center of your choice.

Customer Logins

BLOG

Feb 23, 2023

February 2023 US auto sales holding the line

February 2023 auto sales are expected to advance mildly from the month-prior level, but not nearly enough movement to identify any change to current demand dynamics.

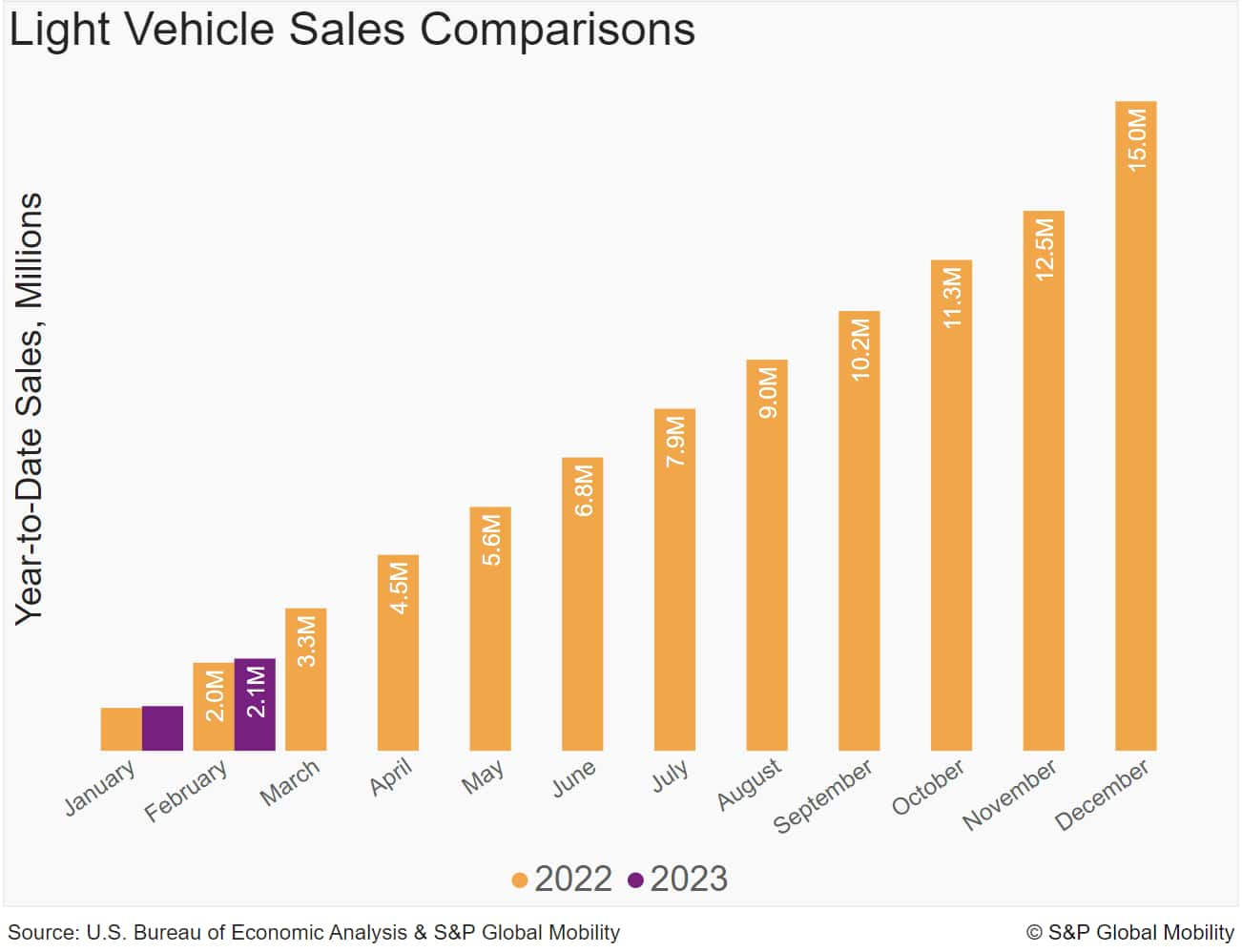

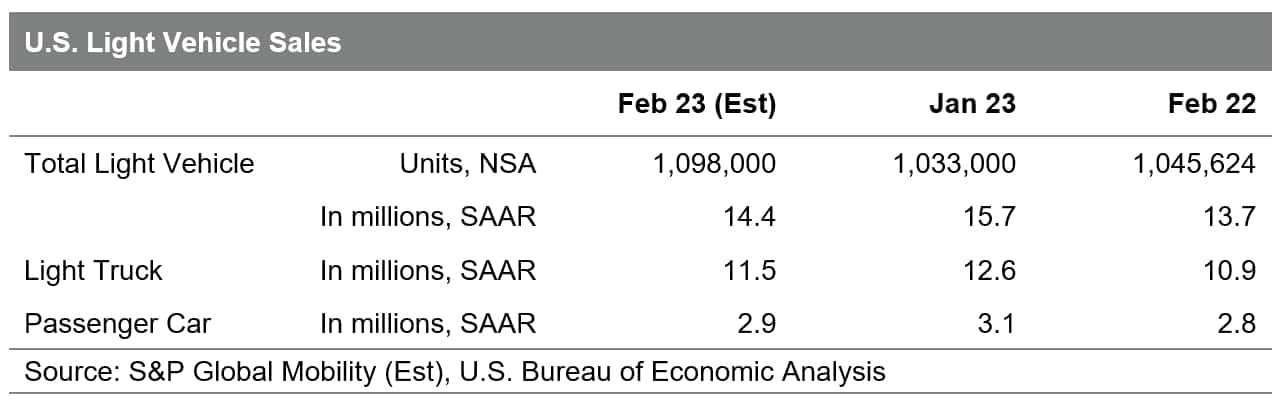

With US light vehicle sales volume for the month projected at 1.1 million units, we expect February 2023 to represent year-over-year (y/y) growth of 5%, the seventh consecutive month of y/y volume improvement. The tally would also be up more than 6% compared to January volumes. February 2023 U.S. auto sales are estimated to translate to an estimated sales pace of 14.4 million units (seasonally adjusted annual rate: SAAR), a marked decline from the month-prior figure, although the underlying sales rate, as represented by the daily selling rate metric, should advance mildly.

"Auto demand levels so far this year have sustained the trends converging in the market at the end of 2022," said Chris Hopson, principal analyst at S&P Global Mobility. "Perhaps notably, fleet sales as a portion of total monthly volume have escalated over the past few months. While this could be an additional signal that auto consumers continue to face an uncertain purchase environment, fleet improvements are not unexpected, as auto production and inventory levels continues to advance."

Regarding the auto production environment, "While demand destruction concerns remain pervasive, production levels are well underway, which should improve vehicle availability by mid-2023," said Joe Langley, associate director of research and analysis for S&P Global Mobility's North American Light Vehicle Forecasting & Analysis team. "Greatly improved vehicle availability may in turn stimulate demand as incentive levels are expected to increase."

The S&P Global Mobility auto outlook for 2023 continues to carry a countercyclical narrative: We expect production levels will continue to improve even as economic conditions are worsening through the early stages of the year. Together with improving production volumes, reports of sustained retail orders, recovering vehicle inventory, and more fleet demand we should see improvements even with worries of an economic recession. S&P Global Mobility forecasts calendar-year 2023 sales volume of 14.8 million units, a 7% increase from the 2022 tally.

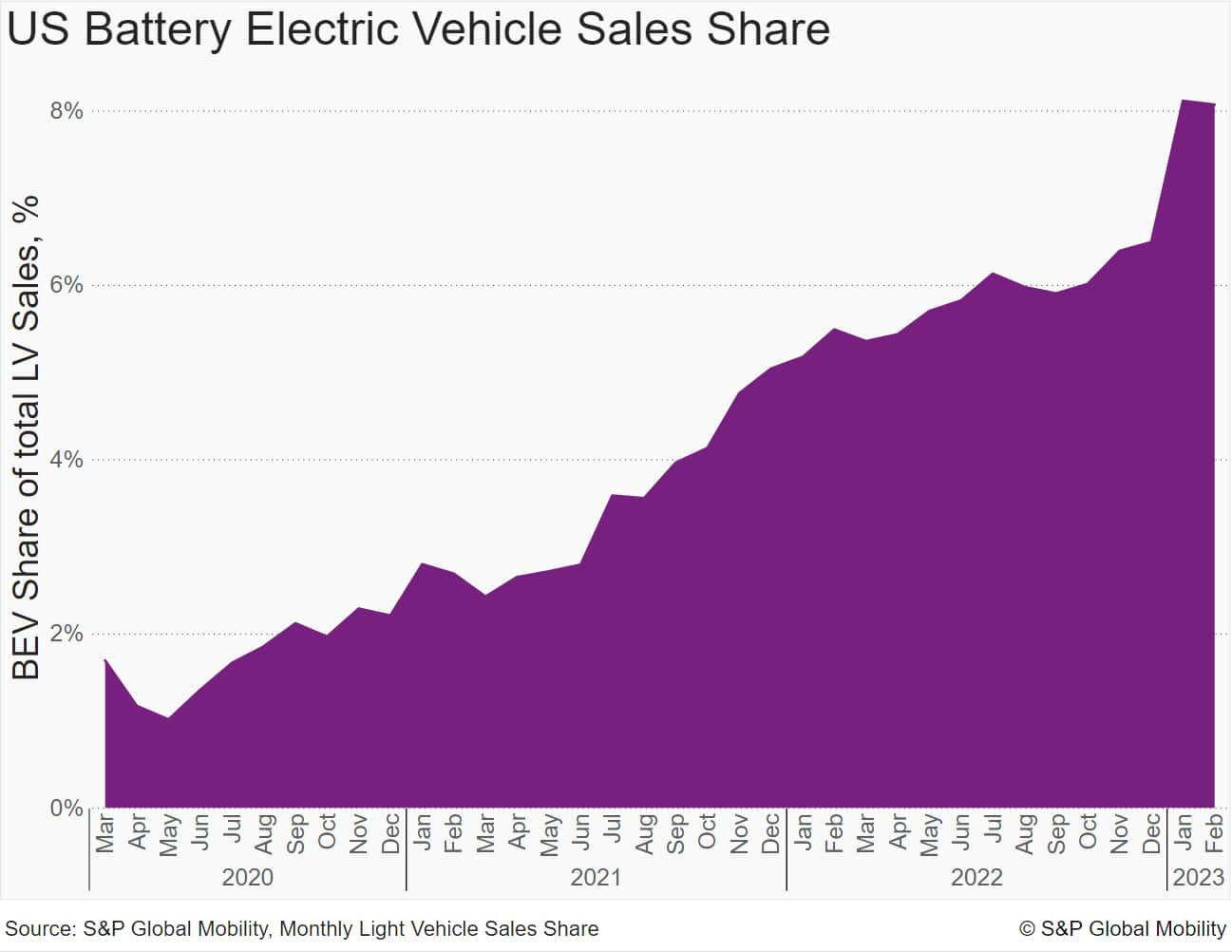

Sustained development of battery-electric vehicle (BEV) sales remains a constant assumption for 2023. The Tesla and Ford price adjustments should continue to boost the monthly BEV share to record levels, as reports reflect that the downward price movement for its products has boosted demand. BEV share in February is estimated to reach 8.0%, continuing the momentum realized in January. Whether these pricing adjustments will be matched by the likes of Hyundai, Kia, and Volkswagen and become a BEV price war, the reaction of other auto companies will determine whether the gains in the BEV mix level will be a blip or a tipping point in the electrification progress of the market.

Keep yourself updated with the latest automotive insights featured on our Mobility News and Assets Community page to stay ahead of your competition.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

{"items" : [

{"name":"share","enabled":true,"desc":"<strong>Share</strong>","mobdesc":"Share","options":[ {"name":"facebook","url":"https://www.facebook.com/sharer.php?u=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2ffebruary-2023-us-auto-sales-holding-the-line.html","enabled":true},{"name":"twitter","url":"https://twitter.com/intent/tweet?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2ffebruary-2023-us-auto-sales-holding-the-line.html&text=February+2023+US+auto+sales+holding+the+line+%7c+S%26P+Global+","enabled":true},{"name":"linkedin","url":"https://www.linkedin.com/sharing/share-offsite/?url=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2ffebruary-2023-us-auto-sales-holding-the-line.html","enabled":true},{"name":"email","url":"?subject=February 2023 US auto sales holding the line | S&P Global &body=http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2ffebruary-2023-us-auto-sales-holding-the-line.html","enabled":true},{"name":"whatsapp","url":"https://api.whatsapp.com/send?text=February+2023+US+auto+sales+holding+the+line+%7c+S%26P+Global+ http%3a%2f%2fstage.www.spglobal.com%2fmobility%2fen%2fresearch-analysis%2ffebruary-2023-us-auto-sales-holding-the-line.html","enabled":true}]}, {"name":"rtt","enabled":true,"mobdesc":"Top"}

]}